A Logical Place to Bounce

I was out of town for a few days around the Juneteenth weekend. The Missouri heat can be oppressive in the summer, so my wife and I escaped to the relative coolness of Colorado with the kids. When I returned, stocks began to rally. You’re welcome.

While I’d like to take full credit (and you certainly have my permission to call this the Harrison bottom if it turns out to be THE bottom), I’m not entirely responsible for last week’s price action. The bounce in stocks is being led by the weakest sectors of the year, and it’s starting from very logical levels.

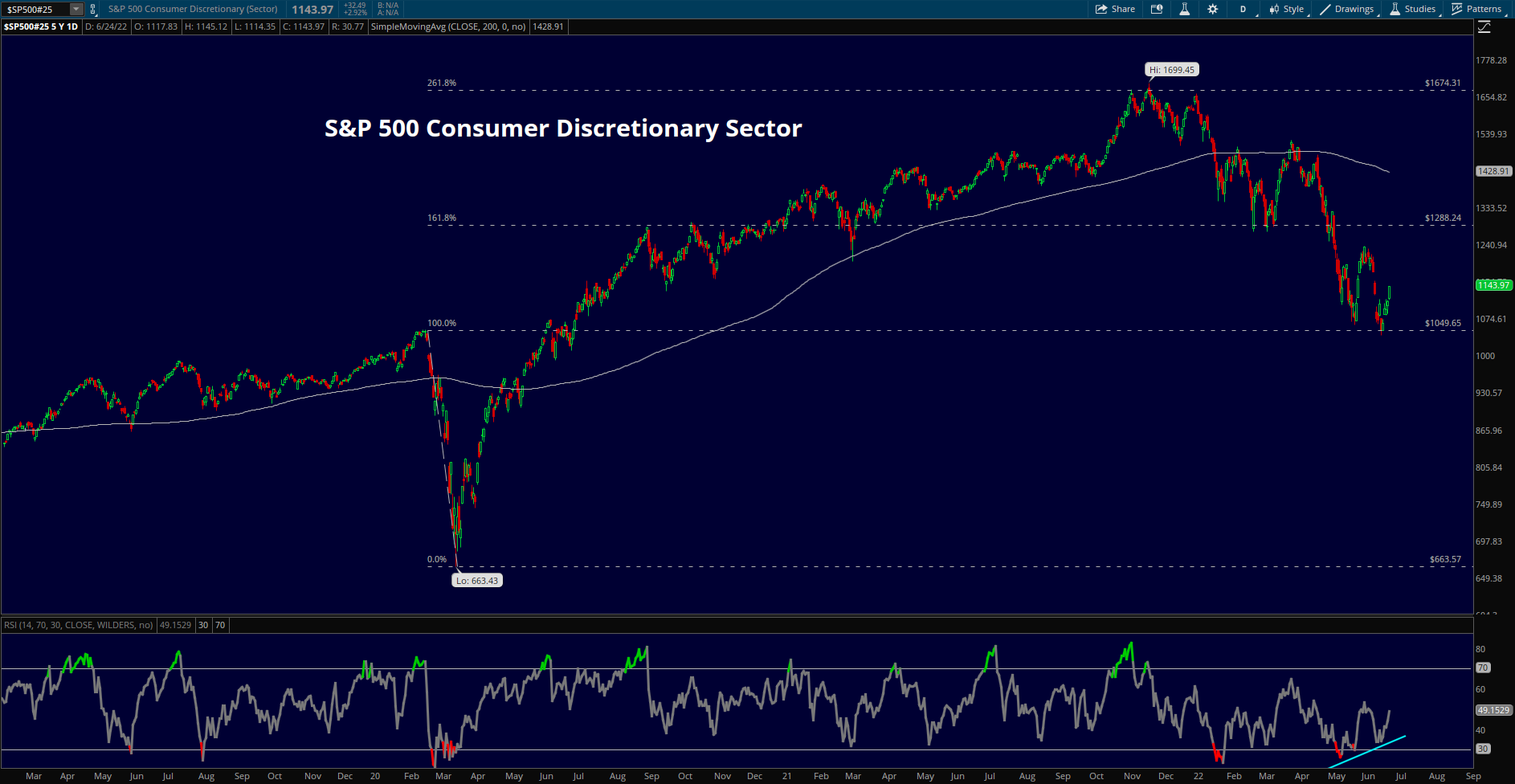

The Consumer Discretionary sector peaked in November of last year, a month before the S&P 500. From there, it fell 37% to the June 16 low, making it the worst-performing sector of 2022. On that day, Discretionary officially wiped out all its gains since the onset of COVID more than 2 years ago. Those February 2020 highs were a major turning point before, and it stands to reason that they could trigger a meaningful bounce for the sector again today.

Additionally, momentum failed to get oversold on the most recent selloff, setting up a bullish momentum divergence at those former highs. Since the mid-month trough, Discretionary has rallied more than 8%, leading all sectors in the index over that time.

The Communication Services sector was the first to peak last year and it’s been the second worst so far in 2022. A bullish momentum divergence sparked a rally in early spring, but prices quickly succumbed to the underlying downtrend. Now, the group is trying again. Momentum stayed out of oversold territory during the June selloff that broke below support at the pre-COVID highs, creating a potential bullish divergence. We’ll need to see more price confirmation first, but if the bears fail to keep the sector below this key level, it could spark the most meaningful rally we’ve seen since the downtrend began.

Information Technology rounds out the group of growth-oriented sectors that have led stocks lower this year. They peaked in the final week of 2021, just days before the S&P 500 as a whole, and fell more than 30% in the aftermath. Unlike its Consumer Discretionary and Communication Services counterparts, Tech has yet to approach its pre-pandemic highs. That could mean the group has some catching down to do. Or it could simply be a reflection and continuation of the relative strength Tech has exhibited over the last decade.

Either way, this is still a logical place for buyers to step in and support the sector. Prices have found the 161.8% extension from the COVID collapse, a level that also marked a peak in September 2020 and a trough the following March. Momentum has stayed out of oversold territory since January.

On the opposite end of the Growth/Value spectrum, the Financials and Industrials sectors have familiar signatures. Each group ran into trouble at the 161.8% extension from its COVID collapse, and each is trying to find support at its pre-pandemic peak. It would make a lot of sense for these sectors to find a bottom here.

Does all this mean we’ve seen the lows for stocks?

Maybe.

All major reversals have to start somewhere, and having two-thirds of the S&P 500’s market cap at a major support level seems a pretty good place to start. But trends are called trends for a reason, and the trend is still down. Until they’ve proven otherwise, rallies during a bear market are just that – bear market rallies.

Here’s a few snapshots from my long weekend in the Rockies.

Nothing in this post or on this site is intended as a recommendation or an offer to buy or sell securities. Posts on Means to a Trend are meant for informational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in posts. Please see my Disclosure page for more information.

The post A Logical Place to Bounce first appeared on Grindstone Intelligence.