Consumer Staples: Sector Outlook

More relative lows

In bull markets, it’s the offensive areas of the market that lead. When prices are trending higher and the economy is booming, people don’t spend a bunch of time thinking about the risks. Who cares about the consistency and stability of selling toothpaste and diapers when there are new, fast-growing opportunities like artificial intelligence?

Alternatively, investors tend to pivot out of those growth-sensitive areas during times of uncertainty, and focus instead on companies with predictable earnings power. Being able to see those pivots give us insights into investors’ appetites for risk. And that’s important, because risk appetite is what drives market prices.

For the last year, strong risk appetite has dominated the market landscape. The S&P 500 has gained more than 30%, led by the Communication Services and Information Technology sectors. Meanwhile, the sector filled with those companies selling toothpaste, diapers, tobacco, and frozen peas has dropped to new lows vs. the rest of the market.

Sure, momentum for the Consumer Staples/S&P 500 ratio has managed to stay out of oversold territory since October, setting the stage for a potential failed breakdown and a mean reversion higher. But bullish momentum divergences don’t mean anything without price confirmation. We just aren’t seeing that yet.

Another way to gauge risk appetite is to look at the Staples and compare them with the Consumer Discretionary sector. Consumer Discretionary companies are more similar to the Staples than say, a regional bank earning money on net interest margins, so we get a relationship that’s more apples to apples. The only difference is the products sold by companies in the Discretionary sector are tied to economic strength. You’re probably not getting a new car or doing a big home remodel during a recession, but you’re still going to the grocery store and buying toilet paper.

So when the Consumer Discretionary/Consumer Staples ratio troughed at the end of 2022, then rose steadily for the next 10 months, that was evidence of buyers showing preference for the riskier, growthier stocks in the market.

However, the Discretionary/Staples ratio peaked in December after running into a key rotational level from the 2021 lows:

Is that a sign of investors fleeing for safety and a harbinger of bad things to come?

We don’t think so.

The relative weakness in Consumer Discretionary over the last few months is largely attributable to just one stock. Tesla alone represents about 13% of the entire sector, even though it’s lost 40% of its value since last summer. And if we strip away the outsized influence of market cap weightings, the Discretionary/Staples ratio hasn’t peaked. It set a higher high just last week.

Risk appetite remains healthy, and that’s a bad thing if you’re owning Consumer Staples.

To be clear, the Staples underperforming doesn’t mean they’re falling. In fact, the sector just hit a new 52-week high last week, the first time it had achieved that feat in nearly 2 years.

Unfortunately, we don’t have the capacity to own everything that’s rising. In bull markets, we have to focus on the things rising the most.

Digging Deeper

Half of the Consumer Staples sub-industries have fallen over the past year. Only one sub-industry, the Brewers, managed to outperform the overall S&P 500 index over that time, and the Brewers peaked last July.

Merchandise Retail hasn’t been too far behind, though.

In a world where the Consumer Staples sector is getting crushed by the rest of the market, Costco is an outlier. Late last year, it broke out to new relative highs against the S&P 500.

However, COST found resistance just shy of our $800 target, and it could take some time to digest its gains over the last few months.

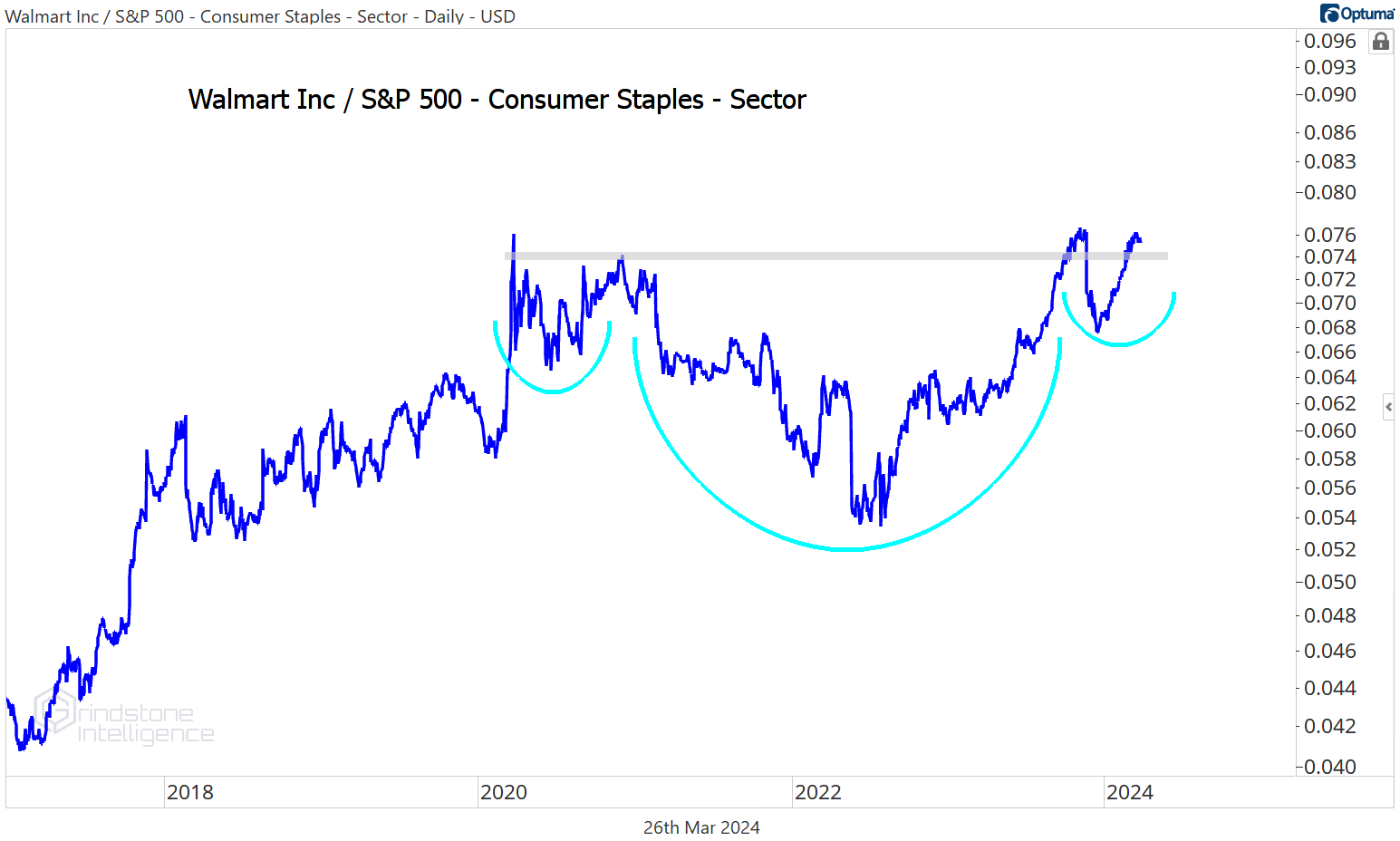

Costco peer Walmart is similarly strong. It’s not showing quite as much strength relative to the overall market, but check out this inverse head and shoulders pattern shaping up vs. the rest of the Staples sector. A breakout here would set WMT up for a big run of outperformance.

We still think WMT will go to $200, which is the 423.6% retracement from the 2018 selloff. Don’t ignore how momentum has stayed out of oversold territory for the last 18 months and is getting overbought on rallies - that’s a big feather in the cap for the bulls.

Leaders

Kroger hails from a different sub-industry than Walmart and Costco, but it’s showing relative strength of its own. Over the last 4 weeks, no Consumer Staples stock has been better. The risk/reward today in KR is much cleaner than it is in those other two, too, as the stock tries to break out of a 2-year consolidation. We can be buying Kroger above $57 with a target up at $79, which is the 261.8% retracement from the 2015-2017 decline.

Tyson is another stock that’s led in recent weeks. Last month, we lamented the failed breakout for TSN above $57, but held out hope that the failure was a false start, and not a catalyst for the stock to hit new lows. Now prices are back above that key level, and we like it long with a target of $70.

It’s not just the breakout that has our attention. It’s the potential for a massive reversal in the relative strength profile. Here’s Tyson trying to bottom against the rest of the market at the same level it did back in 2012:

And we’d be even more confident if it can break out of this base compared to the rest of the sector, too. Downtrends are hard to reverse, and we always need to be wary of betting against the continuation of a trend. But that doesn’t mean trends never reverse. The stage is set here for Tyson.

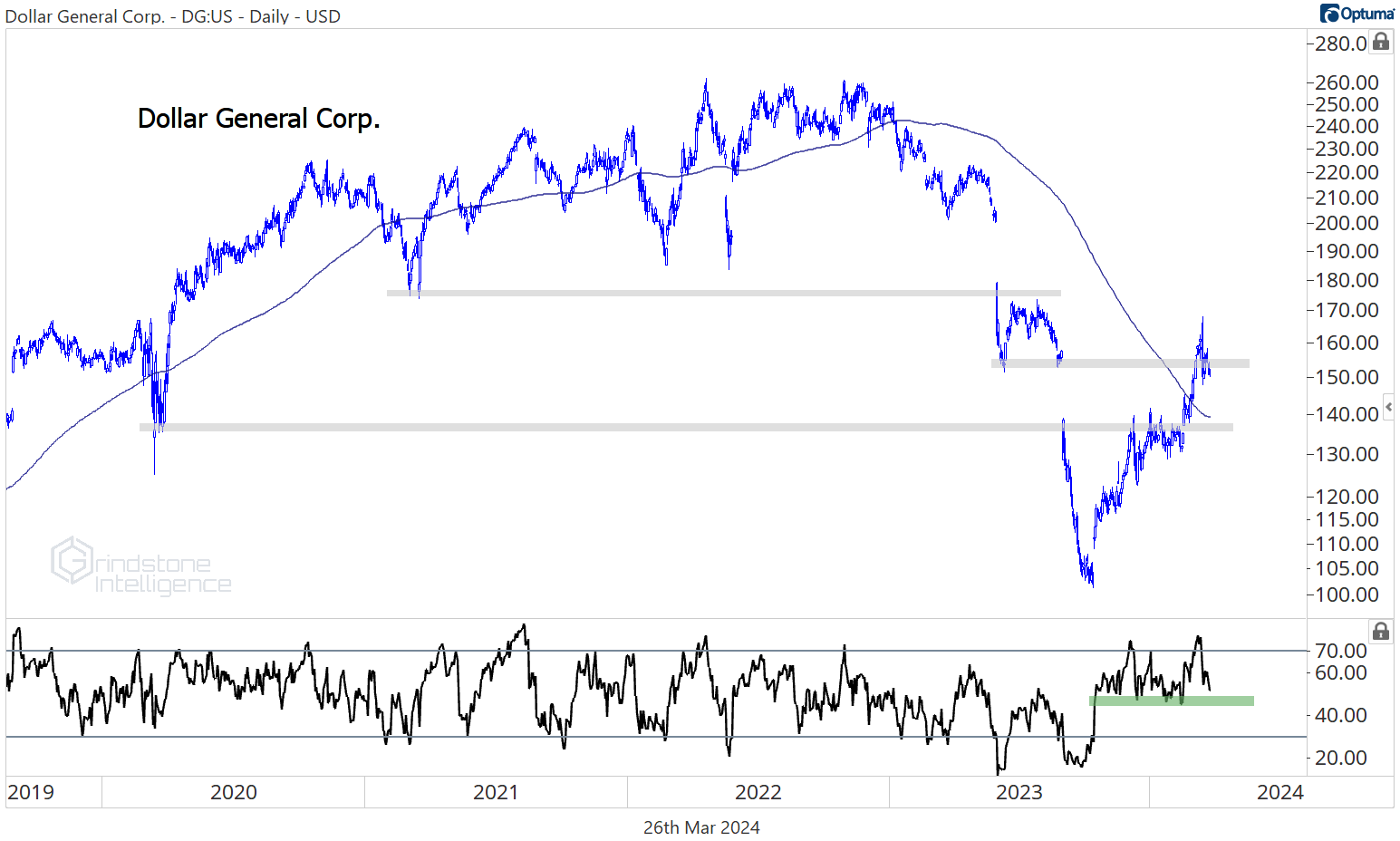

Speaking of reversals, check out Dollar General here. DG just climbed back above its 2017 relative lows.

There’s still a lot of work to do here, but this looks a lot better than it did a few weeks ago. DG is above its 200-day moving average, momentum is in a bullish range, and it’s closed the gap from the August earnings report. With a tight leash, we can own DG above $155 and bet on this downtrend reversal with a target of $200.

Losers

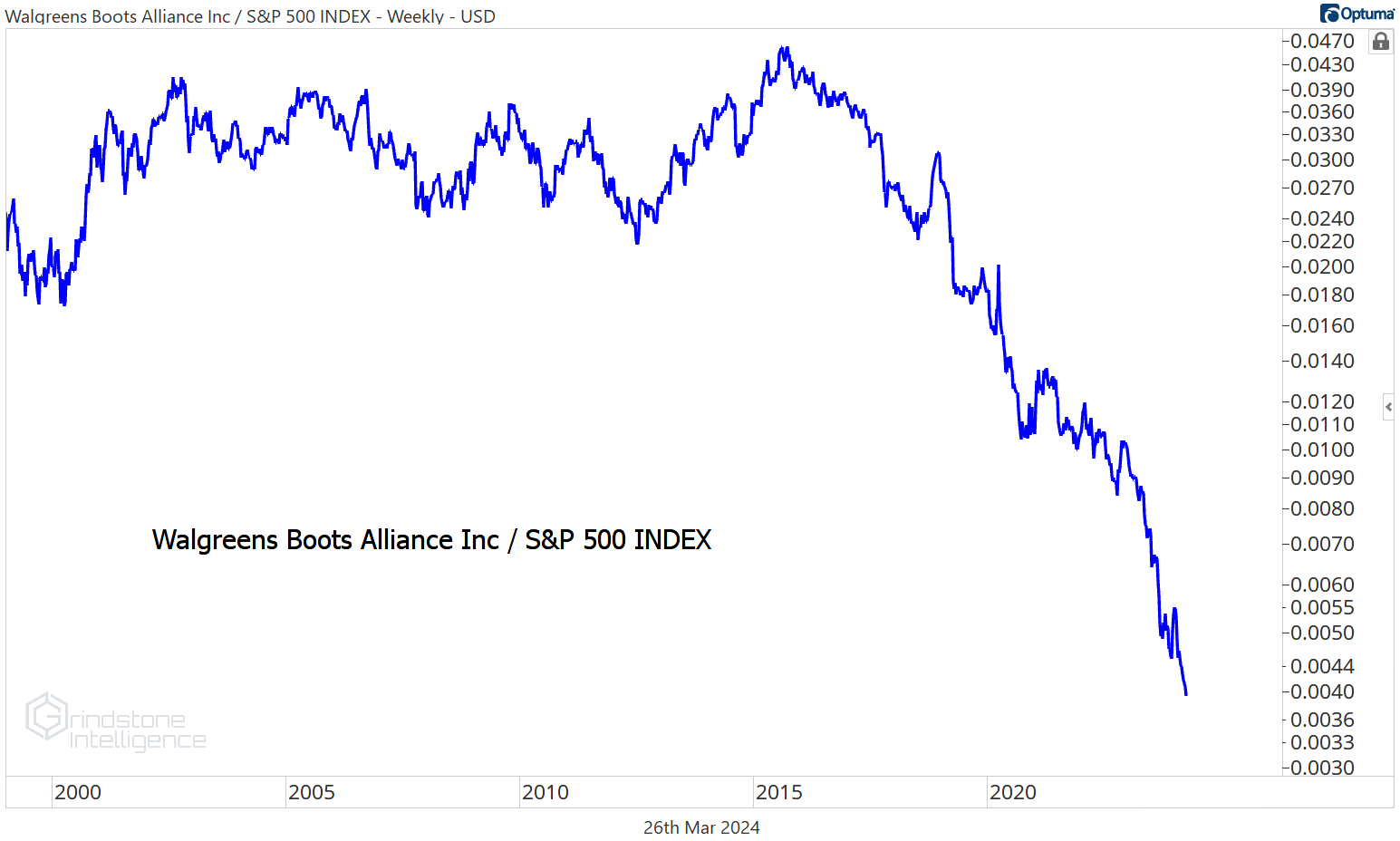

Walgreens is a perfect example of the risks involved when betting on trend reversals. WBA had a lot going for it - 15 year support and a massive bullish momentum divergence to go along with a failed breakdown.

After a textbook mean reversion rally to the 200-day, though, WBA ran out of steam. No, the stock hasn’t broken below the trough set last fall, but the S&P 500 has been off to the races this year, and Walgreens hasn’t participated in any way. There’s tremendous opportunity cost in holding out hope for downtrend reversals during bull markets.

One more chart to watch

Monster Beverage is trading above the 161.8% retracement from the 2021-2022 decline, which has been our key level to watch.

This was one of the best stocks in the world over the past 25 years, and even though it hasn’t gone anywhere for the past year, its uptrend relative to the rest of the Consumer Staples sector hasn’t been damaged at all.

We want to be long MNST with a target of $470, which is the 261.8% retracement from the 2021-2022 trading range, and we’ll have more confidence if it can resolve higher out of this relative base, too.

Until next time.