Don't Sleep on the Industrials: Sector Trends and Trade Ideas – 11/10/2023

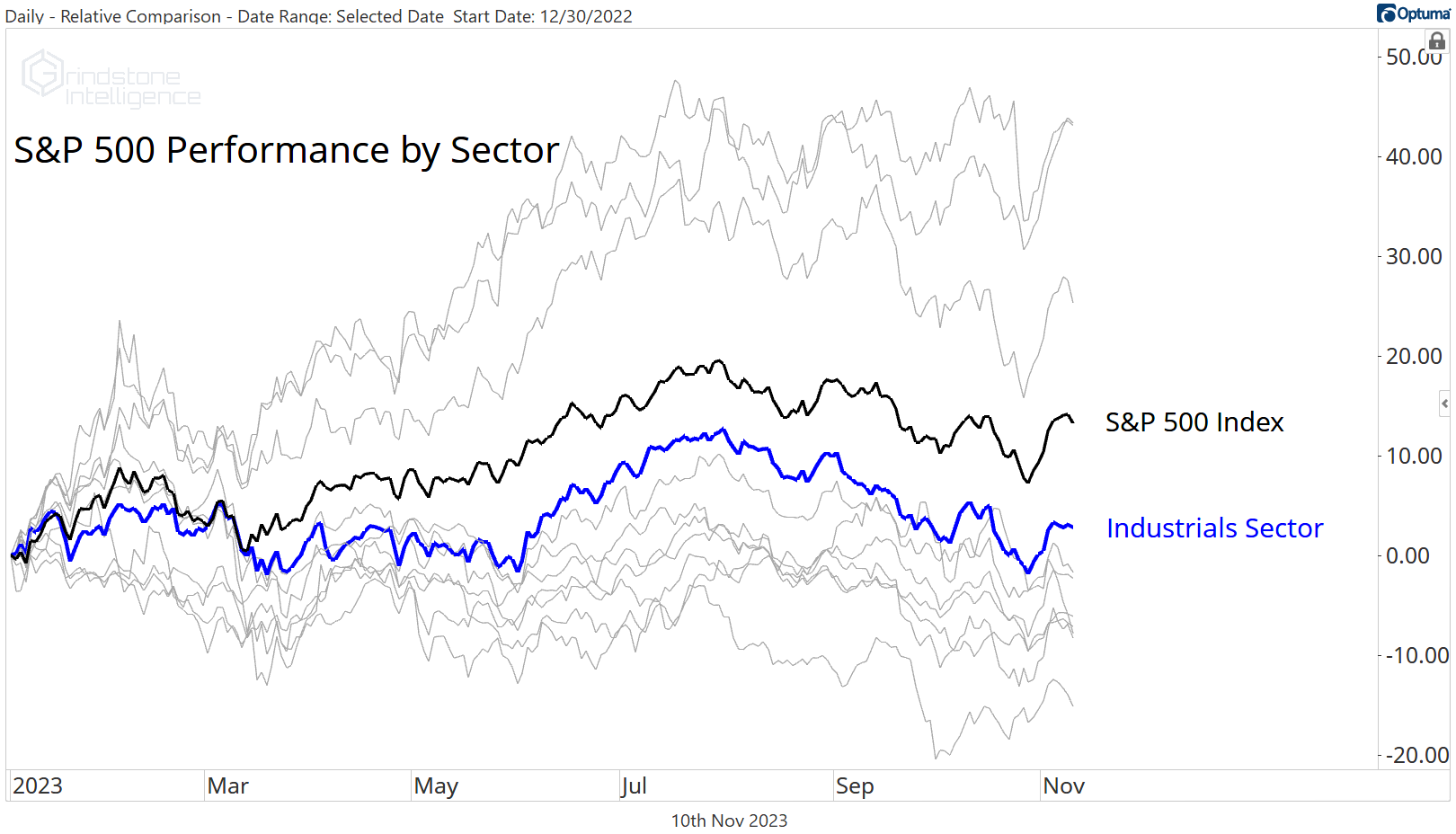

Best of the Worst. That’s perhaps the most apt way to describe the Industrials sector in 2023. The S&P 500’s year-to-date return has been dominated by large cap growth. That’s no secret. The Information Technology, Communication Services, and Consumer Discretionary sectors, home to juggernauts like Apple, Microsoft, Alphabet, Meta, Amazon, Tesla, and NVIDIA, are each up more than 25%. Their huge gains have pulled the S&P 500 Index 13.4% higher for the year. The average stock, meanwhile, has fallen.

The Industrials are a bit of an outlier. They’re the only other sector still sporting a positive return for the year.

Their outlier status goes a bit further, though, because beneath the surface, the Industrials are more than just winners of the consolation bracket. They’ve outperformed the benchmark index on an equally weighted basis, and their 6.4% gain is bested only by Tech and Communications.

That’s not all. Ask almost anyone that’s followed the market this year, and they’ll tell you how bad the small caps have been. And they’d be right: the small caps have pretty much gone straight down when compared to the large caps.

Unless you look at the Industrials. The small cap variety of the sector is up 10% for the year, better than the large cap group and better than every other small cap sector, too.

In short, don’t sleep on the Industrials.

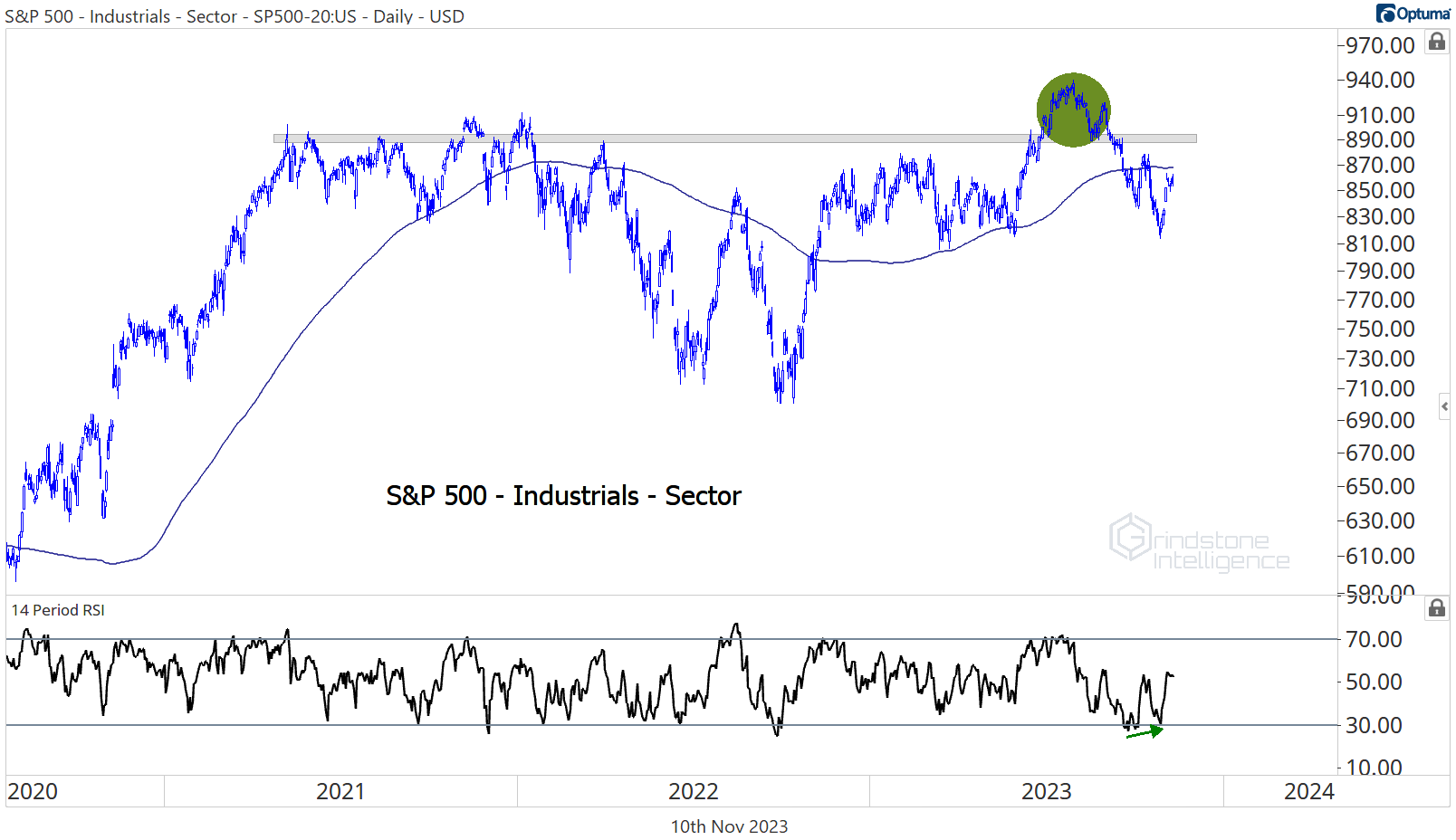

Zooming out, this massive failed breakout in the large cap space is still a problem. It’s most likely going to take more time to repair, and until then, we expect both the sector and the overall market to be choppy and rangebound.

But we don’t have to care that much about what one market cap-weighted, sector-level index is telling us. It’s clear that beneath the surface, things are a lot better than they look. The EW Industrials have been trending higher vs. the EW SPX for 18 months, and this latest consolidation should resolve in the direction of the underlying trend.

The upside resolution could come soon. November, December, and February are historically the three best months for the Industrials relative to the rest of the market.

So which Industrial stocks do we want to be buying? Let’s take a look.

Digging Deeper

Returns across the Industrials landscape vary greatly. Passenger airlines continue to suffer - they’ve more than reversed the 35% YTD gain they had in mid-July, and the group is now down 11% for the year.

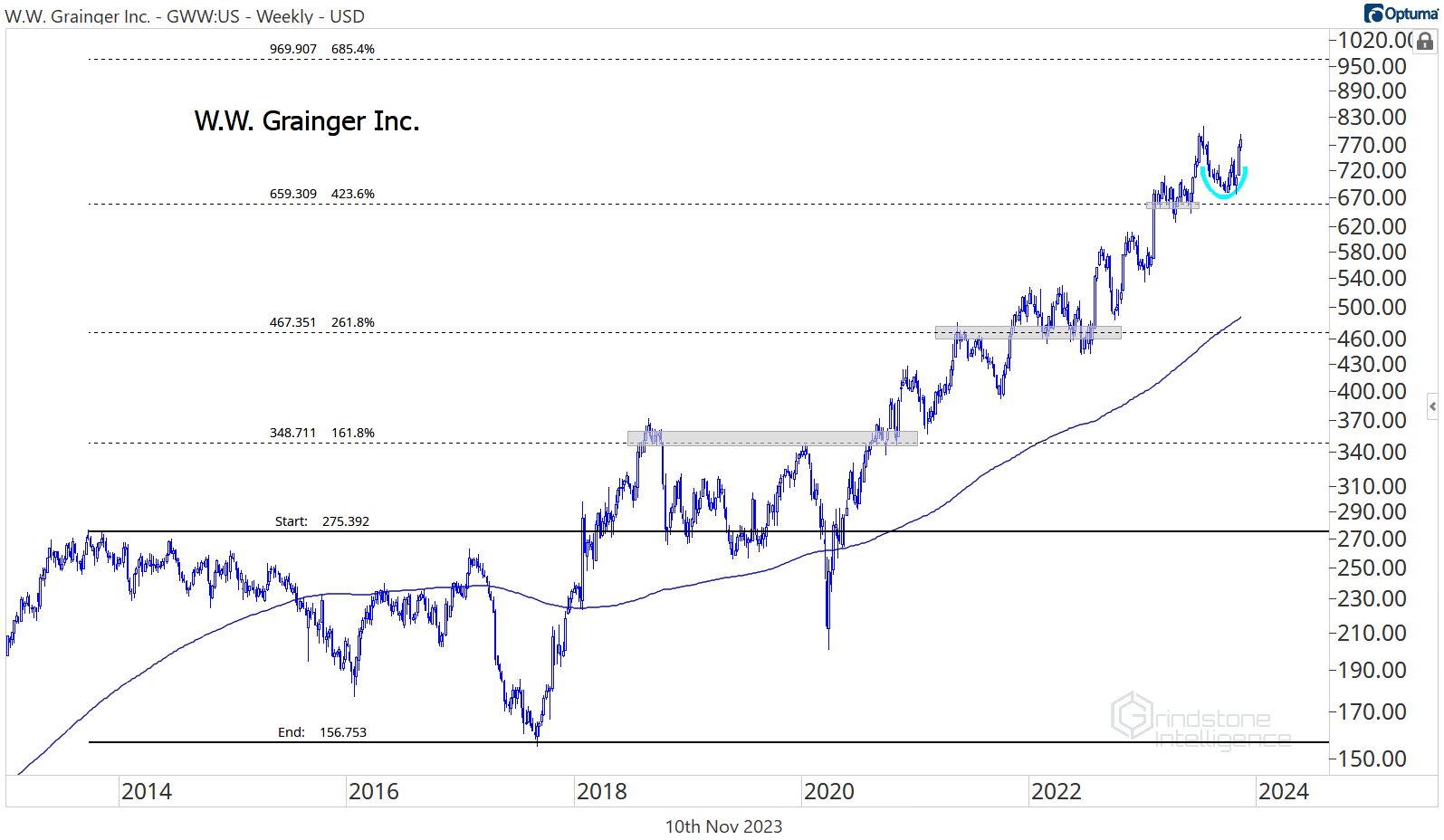

The trading companies, though, are near their highest levels of the year. Grainger has long been one of our favorites in the space (and not just because this author’s brother is a sales manager at the distributor).

We love that GWW just broke out of a 10 year base relative to the S&P 500. It failed at those 2012 highs last October, then pushed above them in January, and successfully backtested them in April, May, and again in September. Now that it’s digested the breakout, Grainger is setting new relative highs again.

It won’t get there overnight, but with the stock in a long-term uptrend on both an absolute and a relative basis, we think GWW eventually heads to $970, which is the 685.4% retracement from the 2013-2017 decline.

The Commercial Services industry is another that’s approaching its highs, and Cintas is the reason. CTAS spent 4 months digesting gains after it ran up and touched the 161.8% retracement from last year’s decline. Now it’s breaking out again. We want to be buying this breakout above $520 with a target of $625.

It’s not just that Cintas is setting new highs. We want to be focusing our attention on the companies that are showing relative strength by outperforming the alternative assets that we could own. That’s exactly what CTAS is doing. It just set new highs vs. the rest of the market.

Leaders

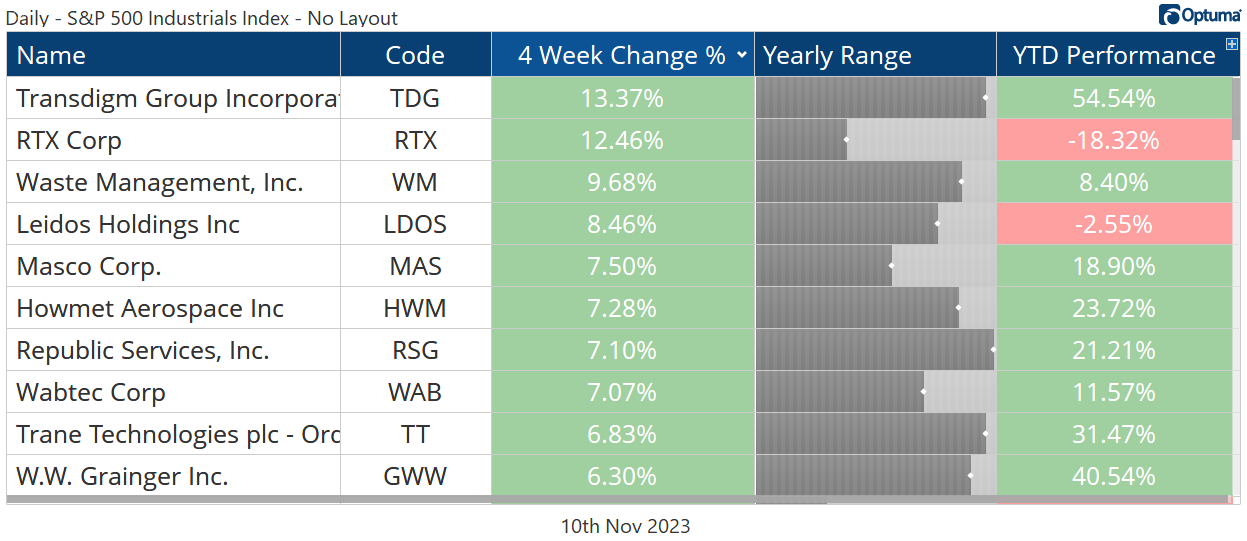

Transdigm was the best-performing stock in the sector over the last 4 weeks, rising 13% and bringing its YTD rally to 54%. This was one of our favorite names early in the year after it broke out of a big, 3-year base, but we’ve been on the sidelines ever since it hit our first target of $930 in August.

We wanted to see how the stock responded to that area of potential absolute resistance and the relative resistance for TDG when compared to the S&P 500. We’ve now gotten resolutions on both.

Our new target on TDG is $1300.

There’s strength elsewhere in the Aerospace industry, too. Howmet Aerospace (HWM) continues to rise after breaking out of a massive, decade-long base. We like it with a target of $70

And the slimmed-down GE looks great, too. We only want to own GE if it’s above $116, which is the 161.8% retracement from the 2021-2022 decline and the peak from June. On a breakout, we think it extends its sector-leading YTD gains and climbs all the way to $145, which is the swing low from 2014-2015.

Has GE already gone too far, too fast? We don’t think so. It’s gone absolutely nowhere vs. the rest of the market for 5 years.

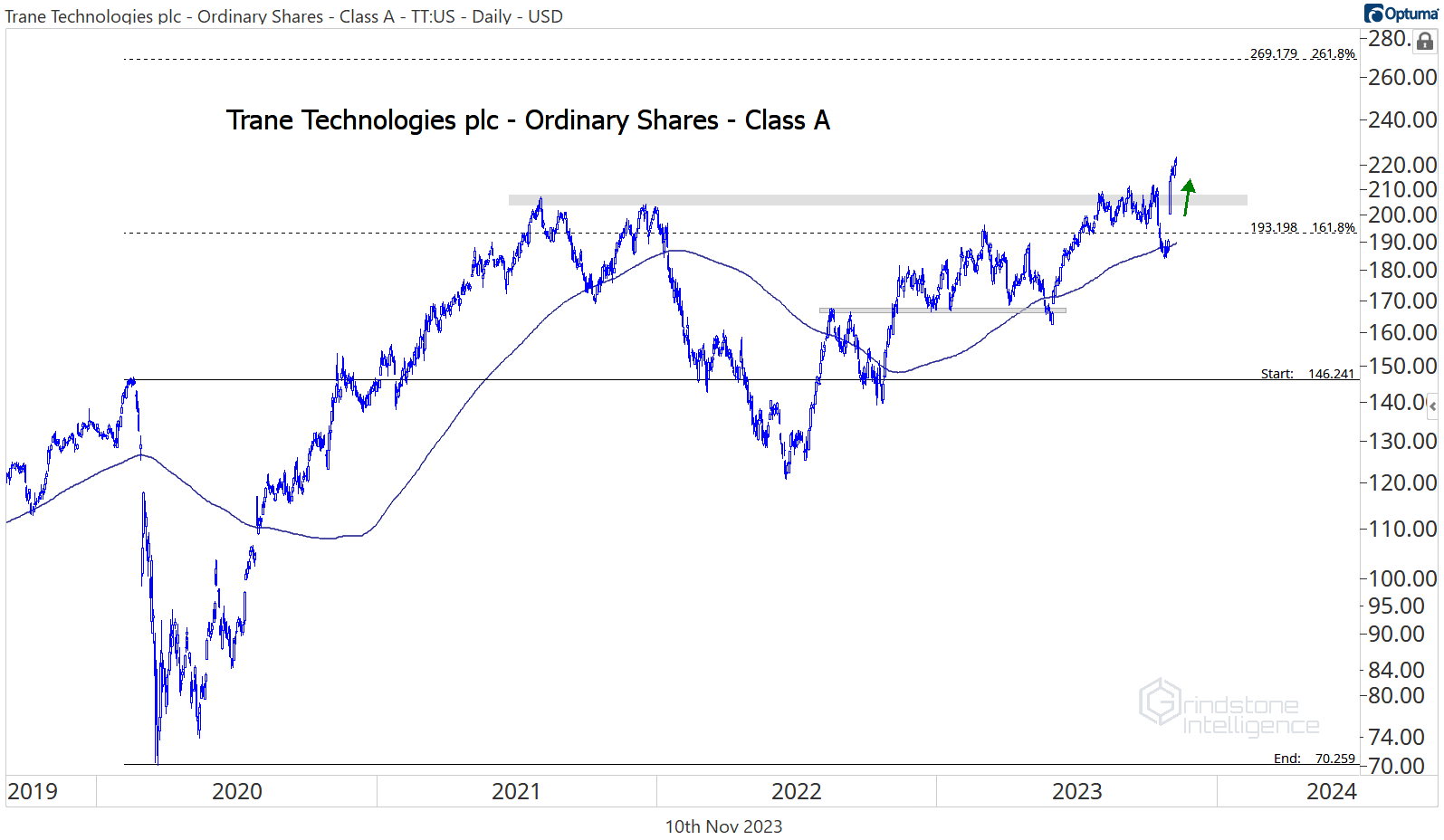

And we’d be remiss if we failed to call out Trane Technologies, which just broke out to new all-time highs. We want to buy pullbacks toward $200 with a target of $270.

Losers

Paycom is a reminder of why risk-management using technical analysis is so important. In late October, the stock broke to new multi-year lows. There was absolutely no reason to continue owning the stock after the breakdown. It was the perfect time to cut losses and look elsewhere. A few days after the breakdown, PAYC reported earnings and dropped another 38%.

The pullback in Old Dominion is one we think is worth buying. ODFL is one of the best-performing stocks in the Industrials sector this year, even after a 15% drawdown from the highs. The long-term uptrend for ODFL is intact as long as prices are above $360, so we want to be buying any pullbacks towards that level with a target back to the highs of $440. We think it eventually goes to $570 - but we only want to own it above the brim of the 2021-2023 cup and handle pattern.

Growth Outlook

Industrial sector earnings growth is near the top of the scorecard in 2023. Only the Consumer Discretionary and Communication Services sectors are expected to outpace the Industrials’ 7% projected growth. That’s well in excess of the S&P 500’s estimated 3% EPS decline for the calendar year.

Growth over the next two years is equally impressive, led by an estimated gain of 11% in each 2024 and 2025. Those estimates are above the long-term S&P 500 earnings growth rate of about 7%.