February Energy Outlook

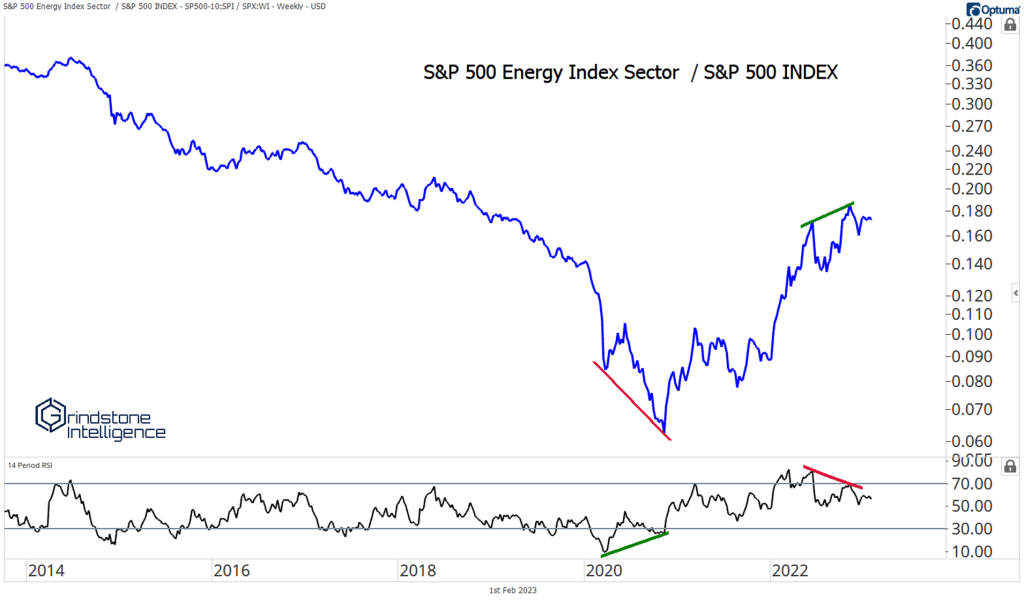

We downgraded the Energy sector shortly after publishing our December outlook. Bearish weekly momentum divergences on both the relative and absolute charts had us cautious about the future of the sector.

Nothing has changed. Except perhaps that we’re even more concerned about the future of the sector.

Remember, momentum divergences don’t always lead to trend reversals, so we’re ready to reinstate Energy’s overweight rating should prices resolve higher. For now, though, we see weakness as a more likely outcome.

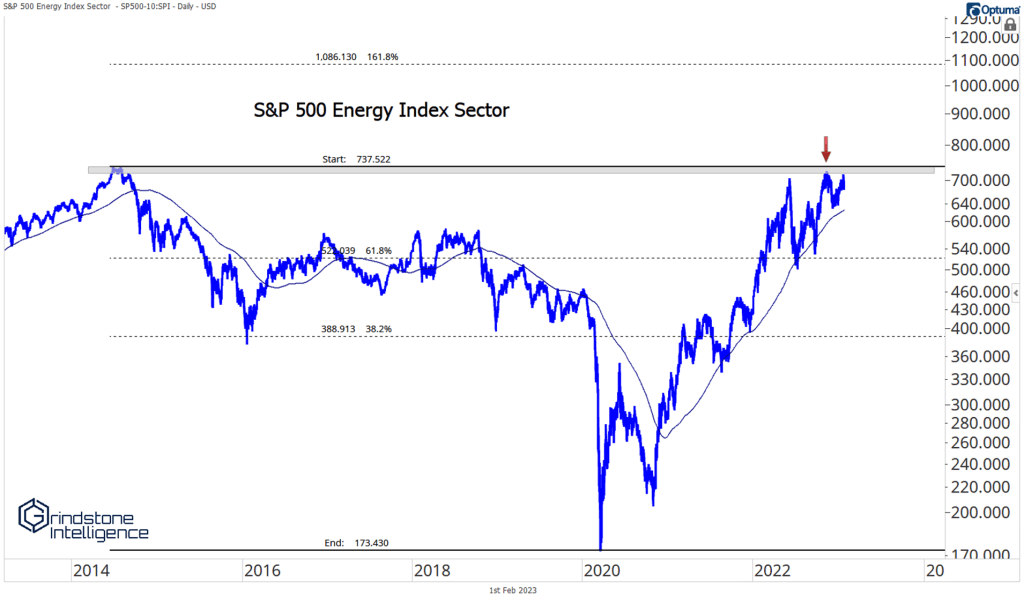

The sector is dealing with resistance from the 2014 highs. For those of you that have been around that long, 2014 was the year that oil prices began a huge, multi-year decline. That former peak has some memory.

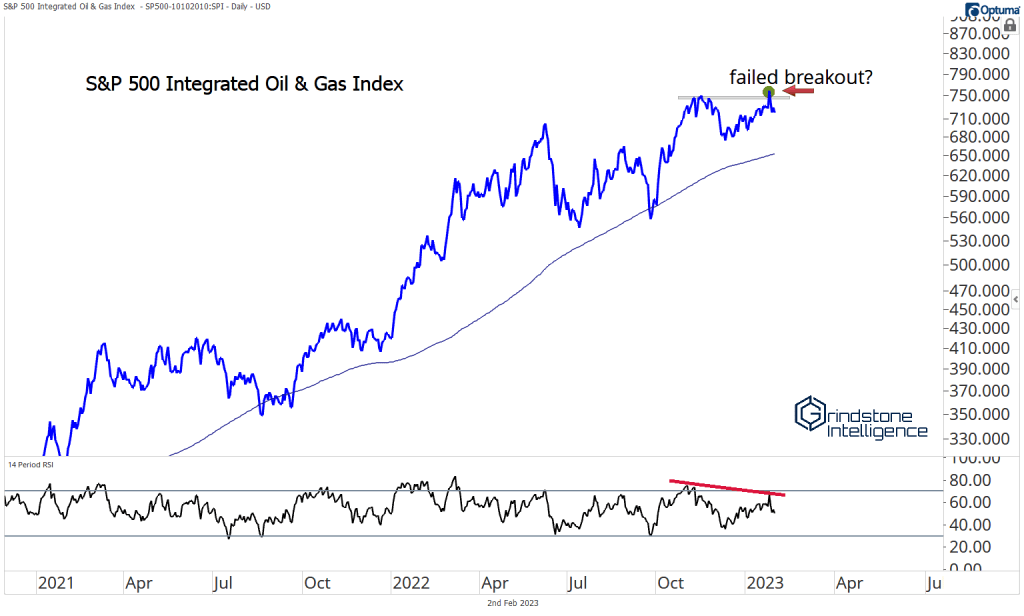

Here’s a chart that screams trouble. The Integrated Oil & Gas industry just put in a failed breakout above its November highs. What’s more, momentum failed to even get overbought on that rally. You’re probably tired of reading the same words over and over again, but we’ll say it again. From failed moves come fast moves in the opposite direction.

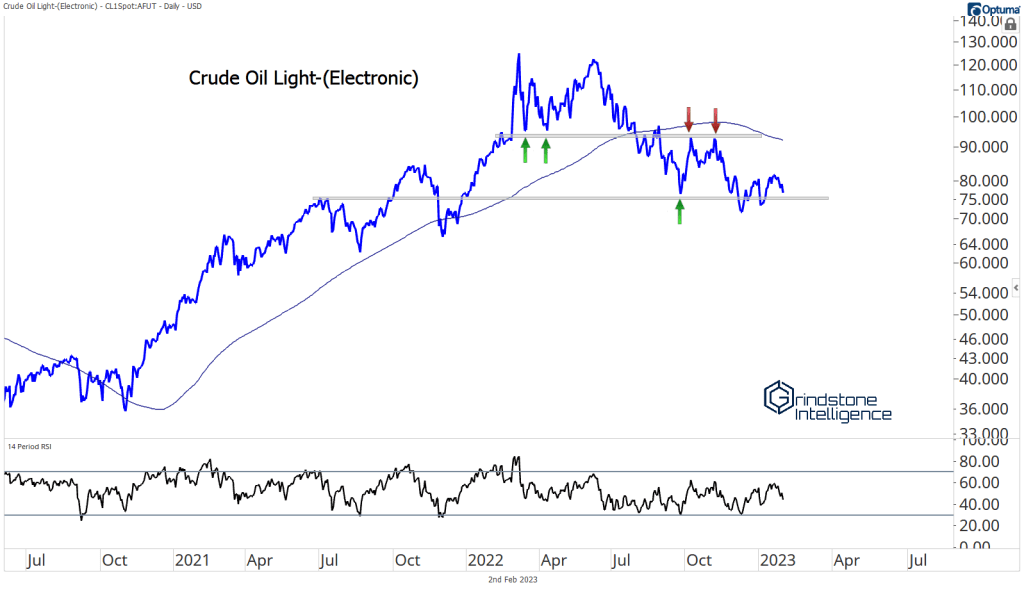

Crude oil breaking below 70 could be the trigger that sends the Energy sector into a tailspin.

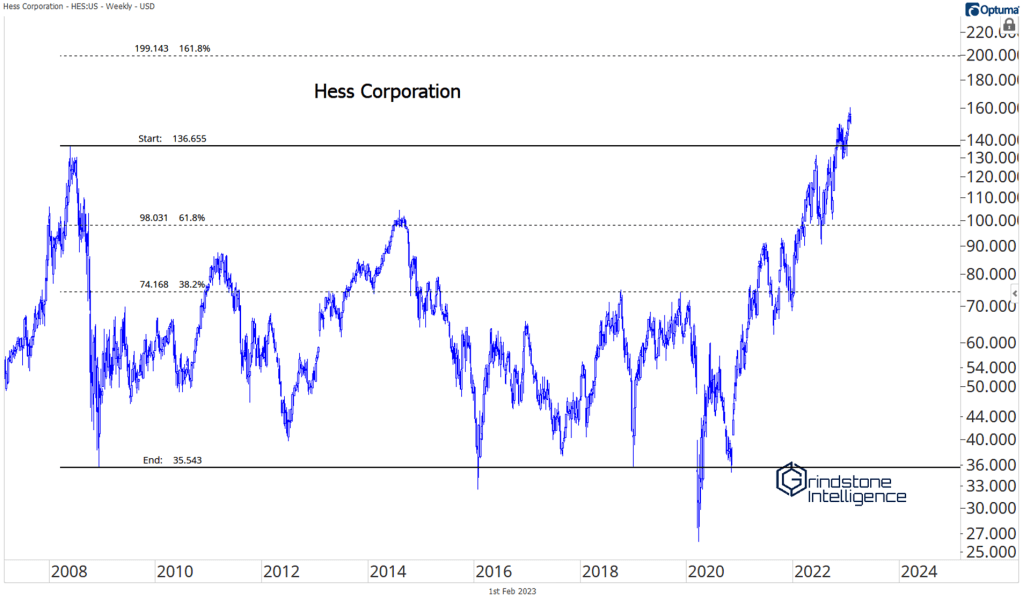

One bright spot has been Hess, which recently broke out above its 2008 highs. We can still target 200 if the stock is above 140, but if it’s below those ’08 highs, we want to take note for potential weakness in the rest of the sector.

Click on each section below to see the rest of our February outlook:

Fixed Income, Currencies, and Commodities Communication Services Sector Consumer Discretionary Sector Consumer Staples Sector Energy Sector – UNLOCKED Financials Sector Health Care Sector Industrials Sector Information Technology Sector Materials Sector Real Estate Sector Utilities Sector

The post February Energy Outlook first appeared on Grindstone Intelligence.