(Premium) February FICC Outlook

Fixed Income

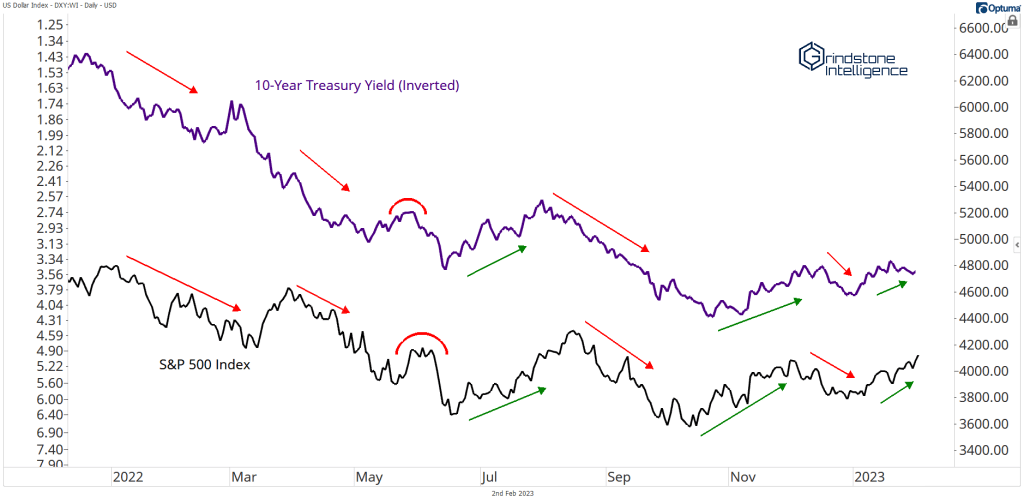

Interest rates dropped in January, providing fuel for the equity market rally and setting the stage for growth stocks to outperform their value counterparts. The correlation between stocks and bonds is nothing new – it drove market all throughout 2022. Check out how closely the two moved together last year:

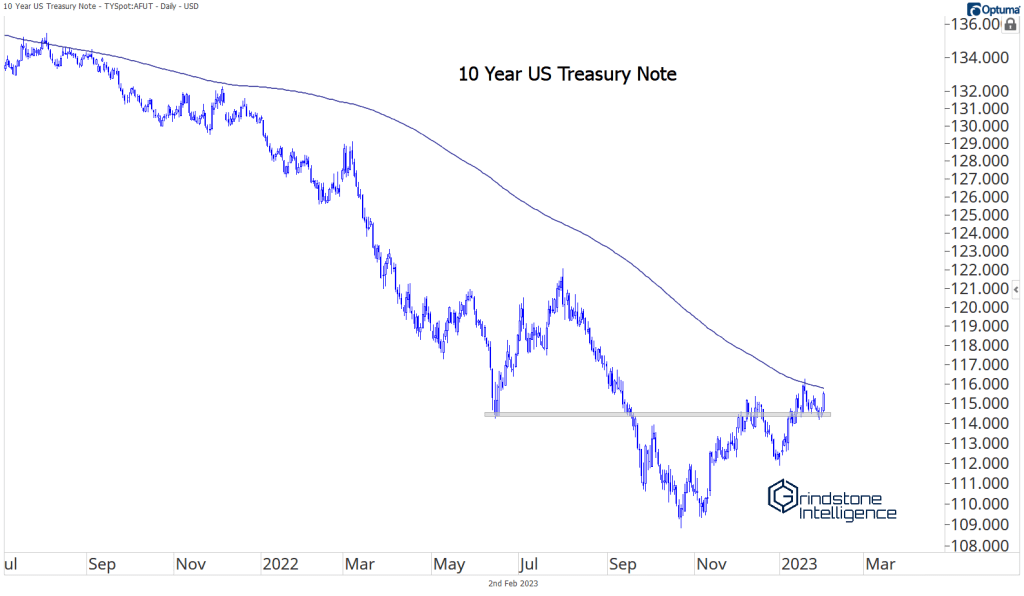

10-Year Treasury bonds staged an impressive rally to climb above their swing-lows from June. That area offers support near-term, though bonds are still below a falling 200-day average.

The one chart that gives us pause is that of the 30-Year Treasury Bond. It’s still stuck below its June lows. Is it just that 30s haven’t joined the party yet? Or are they trying to tell us something about the durability of this rally in fixed income?

We certainly don’t know the answer and don’t have a strong opinion on the direction of interest rates over the coming weeks and months. What we do believe is that stocks don’t need rates to continue falling. They just need them not to rise in a material way.

Currencies

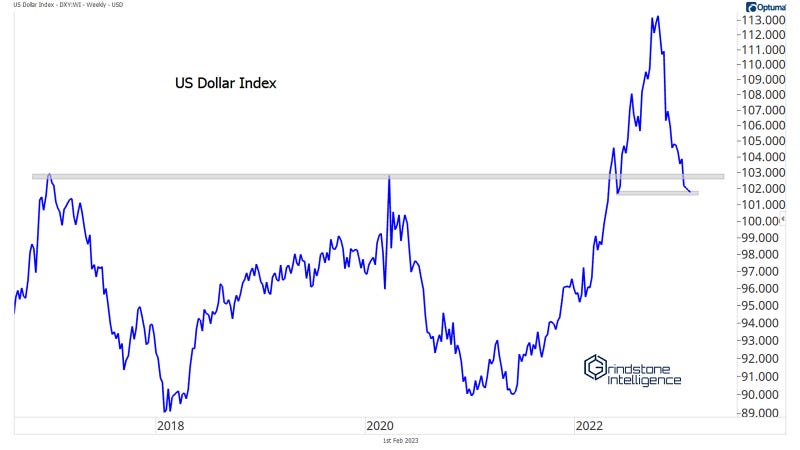

Everything seemed to work in favor of higher asset prices in January, including continued softness in the US Dollar. The correlation between the US Dollar and the S&P 500 in 2022 was every bit as strong as that between bonds and stocks. In December, though, the two began to diverge:

In our January outlook, we asked ourselves:

Does that divergence mark the end of the correlation? Or is a catch-up move coming?

A catch-up move was what we got.

We were surprised by which of the two the catch-up came from. The US Dollar Index was at a logical area of support, and we expected a bounce. Instead, it continued to fall. The last line of support for Dollar bulls is the swing lows from last May.

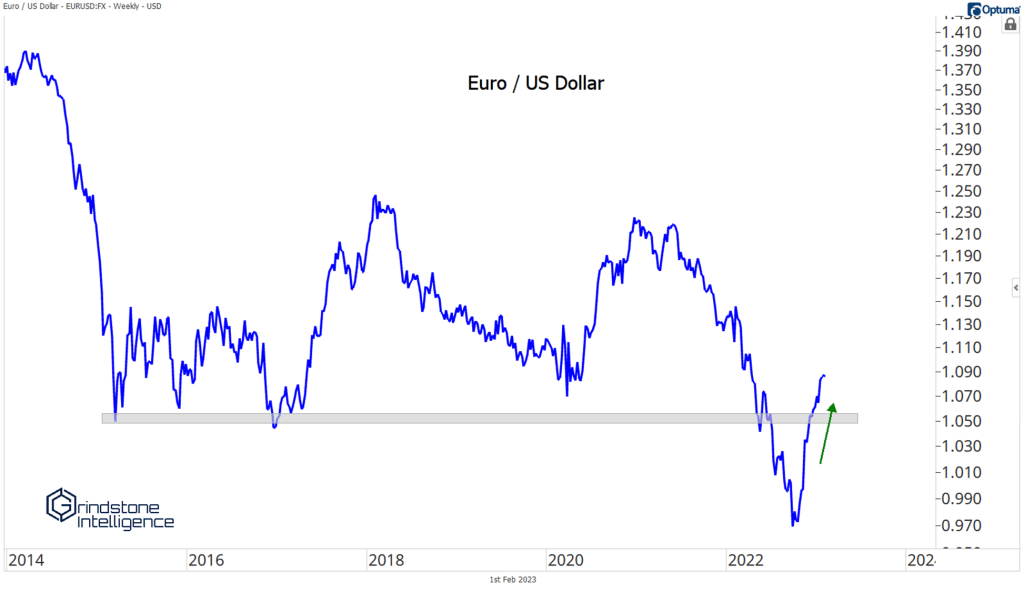

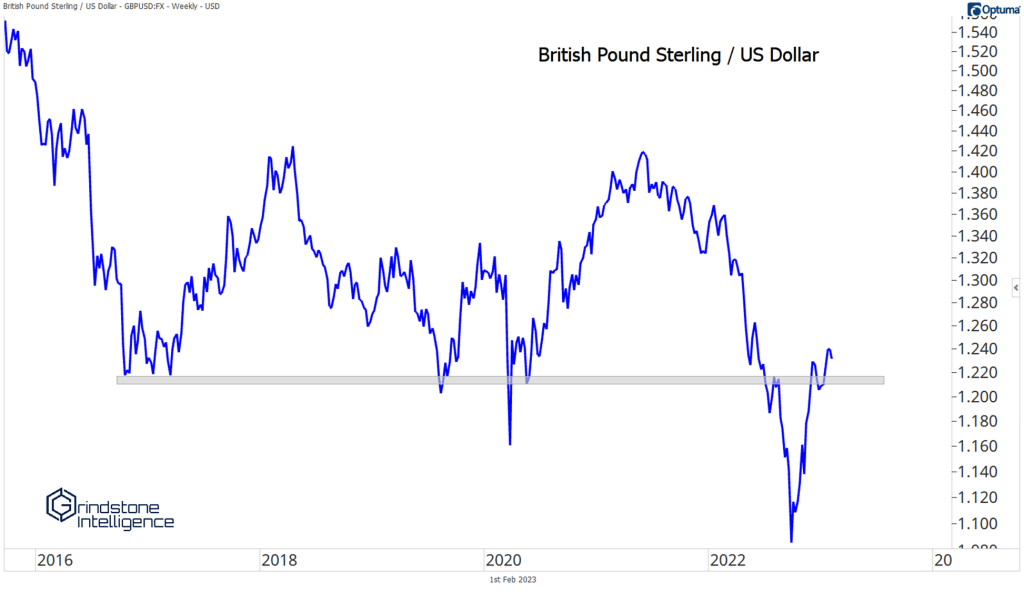

If you look at the individual currency crosses, though, that line of support has already broken. The Euro is now comfortably back above its 2015-2017 lows relative to the USD.

So is the British Pound. Between the two of those, that’s almost 70% of the US Dollar Index. It’ll take some pretty major reversals to change the landscape at this point.

Bitcoin

Here’s what we had to say about Bitcoin last month:

There’s really no good reason to get involved from the long side unless we’re back above 20000, and even then, we’d be fighting the trend.

Well, prices started the year by promptly jumping above 20000. While a new uptrend may have started with the turning of the calendar, we’re skeptical that it will be all smooth sailing from here. Still, it looks like the downtrend is broken. A neutral approach is best until the next trend shows itself. That’ll be when prices are either above 30000 or back below 20000.

Precious Metals

Gold continues to rally since finding a bottom in November. It’s up almost 7% for the year, and it’s not something we want to be approaching from the bearish side.

The long-term bull case for the yellow metal is easy to make. We just spent a decade digesting a decade-long 600% rally, which itself began after a decade-long consolidation. Wouldn’t it make sense for the 2020s to be the decade that gold returns to the forefront of investor returns? First, we need to see it surpass $2000/oz.

Here’s the one problem for precious metal bulls: Silver hasn’t confirmed the latest rise.

Back in early November, when gold was breaking to new lows, we pointed to silver as a reason not to turn completely negative on the space.

Silver and gold tend to be highly correlated, but silver tends to move in greater magnitudes. As such, when the precious metals space is under pressure, silver tends to lag, but it outperforms during bull markets. With gold breaking to new 52-week lows in October, we should have expected silver to do the same. Instead, it’s working on what looks like a rounded bottom at multi-year support.

And in December, silver’s rapid rise gave us confidence in our bullish outlook for the group. But now silver just isn’t playing along. The intermediate-term trend is higher, so we should expect this little consolidation to resolve higher. If it doesn’t, you’re going to have a hard time convincing us that gold prices are moving materially higher.

The post (Premium) February FICC Outlook first appeared on Grindstone Intelligence.