Interest Rates are Rising. Is it Time to Worry About Home Prices?

Over the last 2 years, my conversations with friends and family have turned to housing more often than not. I’d wager yours have, too. With prices surging at a pace not seen in over a decade, homeowners equity reaching new highs, reports of all cash offers, bidding wars, ecstatic sellers and frustrated buyers, how could they not?

History painted a bleak outlook for housing after the global pandemic struck – recessions aren’t exactly a tailwind for real estate values. But this time was different. Consumers were flush with cash after unprecedented stimulus payments, and the work from home movement drove a newfound appreciation for larger living areas. Couple that with the demographic backdrop of accelerating millennial household formation that began in the years prior to 2020, and real estate was able to buck its historical trend.

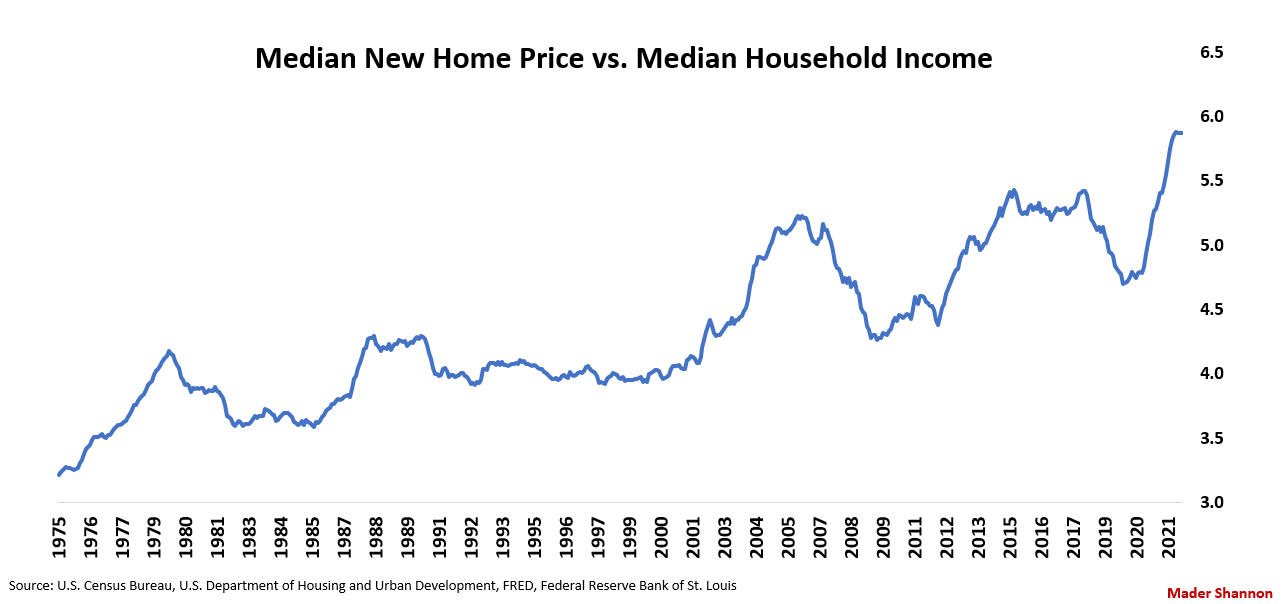

Trees don’t grow to the sky, though. Home prices can only rise so quickly before they become unaffordable. The median price of a new home in the United States is now nearly 6 times the median annual household income, the highest on record and almost double the level in 1975.

Yet price levels don’t tell the whole story. Despite the anecdotal evidence to the contrary, most of us aren’t paying cash for our homes, we’re taking out a mortgage. And interest rates have rarely been lower than they are now. In fact, if you can muster the funds for a down payment, the monthly mortgage payment for a new home isn’t much different than it was 45 years ago – and it’s significantly less than it was during the early 1980s.

That won’t remain the case if rates continue to rise. The average 30-year mortgage rate has jumped 1.3% since year-end, and with the Federal Reserve seemingly bent on controlling inflationary pressures in 2022, it could climb much higher.

With the 2006 housing collapse still fresh in the minds of the public, the rise in mortgage rates has sparked concerns about affordability amid elevated price levels. The median price of a new home today is $416,000. If rates climb to 6%, prices would have to fall to $348,000 to maintain the same monthly mortgage costs. At 8%, the sticker price drops to $284,000.

Will a spike in rates trigger another housing meltdown? Maybe. But consumer credit profiles are much stronger than they were in 2005, reducing the risk of widespread foreclosures. Moreover, borrowing costs are only one factor at play in this red-hot real estate market. Inventories of existing homes are hovering at record lows, with less than 2 months of supply on the market.

Strong demand has contributed to the shortage of existing home availability, but the larger issue is short supply of new homes. In the aftermath of the Great Financial Crisis, the U.S. experienced the weakest period of single family home starts in decades. After under-building for a 10 years, there simply aren’t units available to satisfy the demand from new households.

Unfortunately, new construction capacity can’t be turned on with the flip of a switch. Publicly traded homebuilders accepted record order increases in 2020, but quickly found that labor and material shortages were too severe to keep pace. They’ve since curbed new orders by limiting lot releases and waiting until later in the build cycle to make homes available. Meanwhile, they’ve worked with vendors to secure materials and appliances months in advance, only to see suppliers still unable to meet their commitments. Build times for most builders are at least 6-8 weeks longer than they were a year ago. Somehow, despite the operational headwinds, the industry has maintained margins. In fact, they’ve expanded them to the highest level in recent memory. Price is a powerful tool.

The question is, can they maintain those margins in the face of rising mortgage rates and price pressures?

Nothing in this post or on this site is intended as a recommendation or an offer to buy or sell securities. Posts on Means to a Trend are meant for informational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in posts. Please see my Disclosure page for more information.

The post Interest Rates are Rising. Is it Time to Worry About Home Prices? first appeared on Grindstone Intelligence.