(Premium) January Consumer Discretionary Outlook

We were premature in our upgrade of the Consumer Discretionary sector last month. We believed the relative lows from the spring would act as support and offer a relief rally, but that thesis proved incorrect. Instead, the sector broke to new lows on both a relative and absolute basis:

There’s really only one name to blame for the weakness, and that’s Tesla. Tesla dropped more than 40% during December, and its size dragged the entire sector index lower. A 40% drop in one month could set the stage for a relief rally in the name, and with the stock positioned roughly midway between the January 2020 and August 2020 highs, this isn’t an ideal place to be initiating new shorts. But this is not what an uptrend looks like.

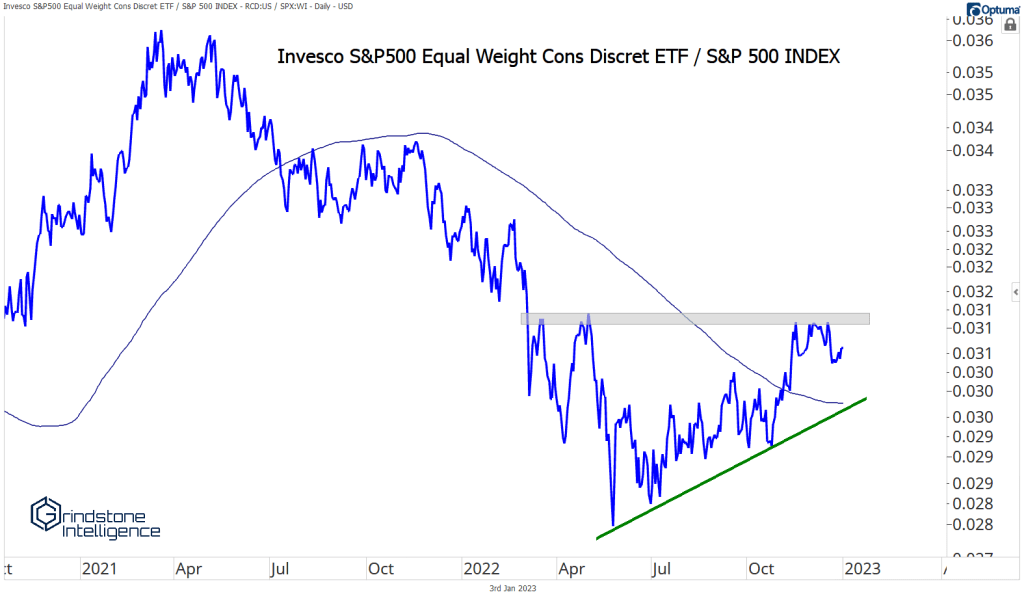

Removing Tesla’s outsized effect from the index gives us a different feel for the sector, though. The equally weighted Consumer Discretionary sector bottomed relative to the S&P 500 almost a year ago, and it’s comfortably above a flat 200-day moving average. There are plenty of long opportunities in the sector.

Auto parts retailers have been on our radar for months, and they’re still in great shape. Here’s ORLY and AZO, still tracking towards our targets.

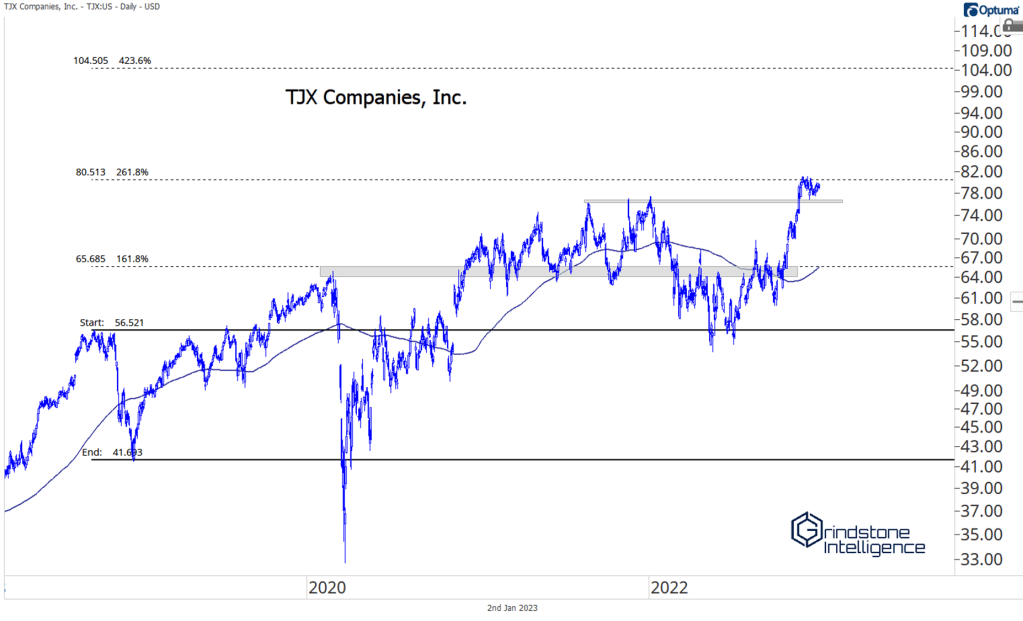

A handful of other retailers have nice setups as well. TJX is near 52-week highs. If it’s above 80, we can be long with a target of 104.

It’s not just names that are in established uptrends that are showing signs of strength, either. Etsy and Bath & Body Works have both exited clear downtrends and are now working on higher highs and higher lows.

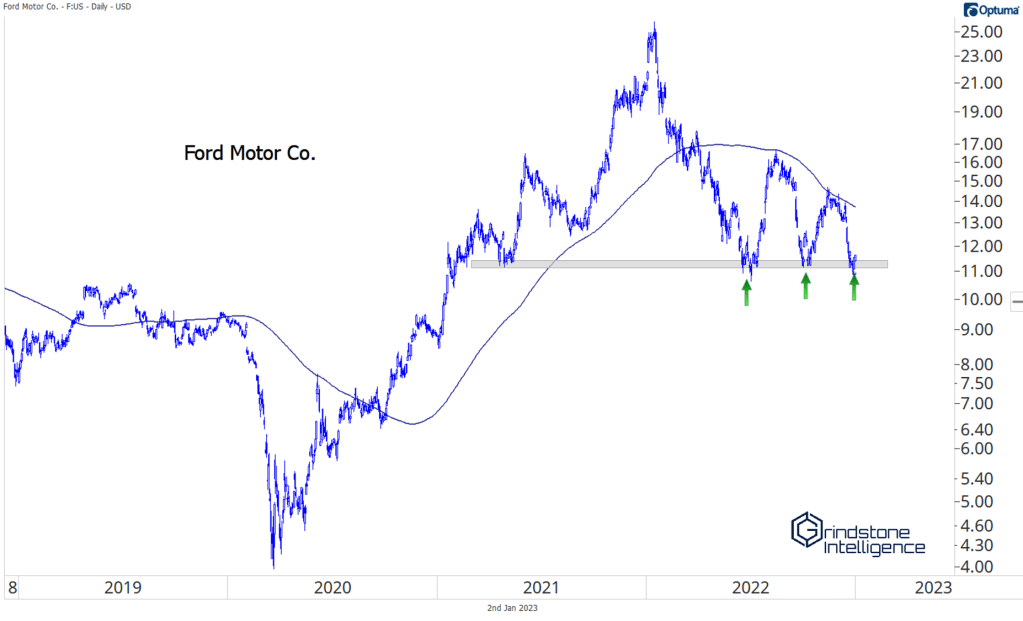

And the weakness from Tesla hasn’t bled over to other auto manufacturers (at least not yet). Check out Ford continuing to hold above key support.

So despite Tesla’s terrible month, there’s lots of underlying strength in the Consumer Discretionary sector. We just have to be selective.

The post (Premium) January Consumer Discretionary Outlook first appeared on Grindstone Intelligence.