June Technical Market Outlook

Don’t fight the tape.

Marty Zweig said it best: The trend is your friend, don’t fight the tape.

At the start of each month, we take a top-down look at the US financial markets and ask ourselves: Is this a time to buying stocks and increasing our exposure to risk? Or are we better served looking for stocks to sell and finding alternative places to invest?

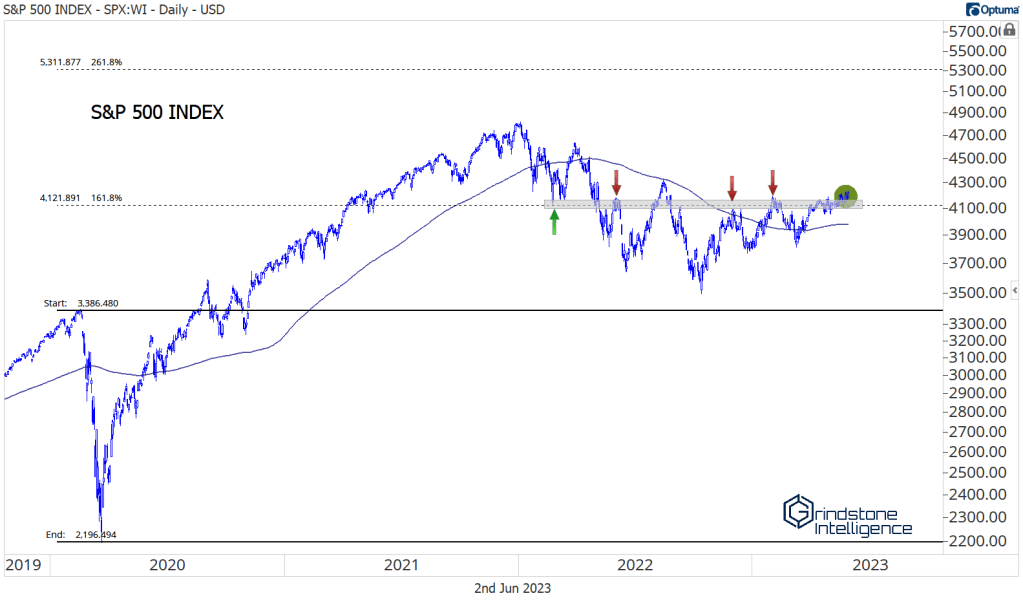

All year, we’ve come away with the same conclusion: if the S&P 500 is above the resistance area near the 161.8% retracement from the COVID selloff, then we need to be focused on buying stocks, not selling them.

In May, the bulls got the resolution they were looking for. The SPX absorbed all that overhead supply from 14-months of rotation and now sits at its highest level since last August. Mr. Market is indicating that higher prices are ahead.

Unless you’ve been living under a rock over the last few weeks, it’s not hard to guess what fueled the breakout. Growth stocks – and especially those in the Information Technology sector – are driving the gains. The NASDAQ Composite has now risen an impressive 25%in the first five months of the year. The NASDAQ 100, which includes only the largest stocks on the exchange, has jumped 32%. What’s not to like about that?

The NASDAQ Composite was the first to clear key resistance when it surged past its own 161.8% retracement. That level also held significance because it marked the September 2020 peak that began a multi-year rotation from growth into value. So long as we’re hanging above 12400, how can we approach this index with anything but a bullish perspective?

The next hurdle for the index is those August highs. After such a strong move over the last few weeks, it wouldn’t be surprising to see the NASDAQ take a breather. But even a pullback to the 12400 breakout point wouldn’t alter the bullish structure.

Of course, investing isn’t an easy endeavor, and there’s plenty not to like about these breakouts. For one, the move simply isn’t that broad.

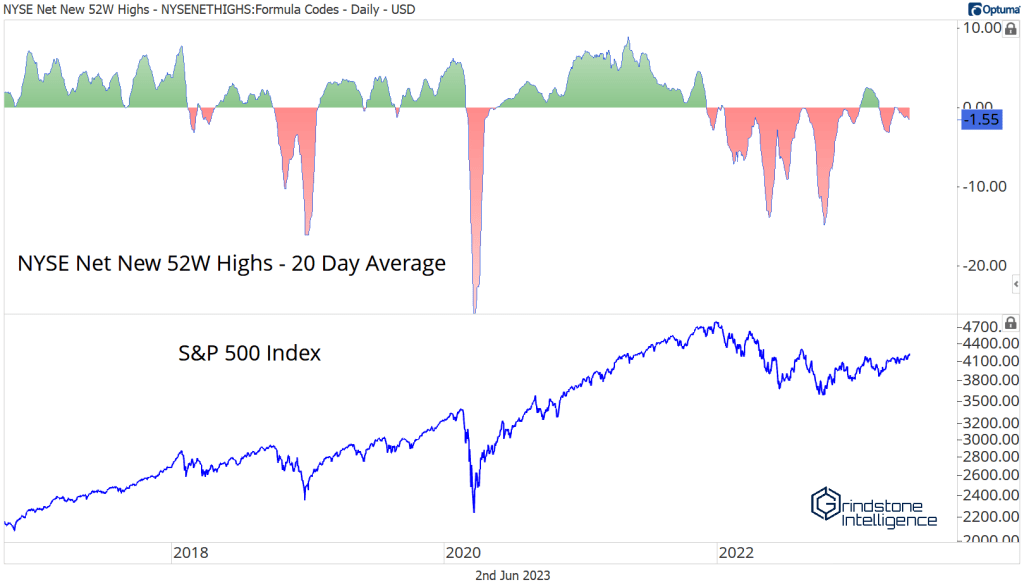

When we talk about ‘breadth’ in the market, we’re talking about the number of stocks participating in a trend. The more stocks that participate, the healthier a trend is and the more likely it is to last. A lack of bullish breadth warns of a weak uptrend.

Outside of large cap tech, things aren’t as rosy as they look on the surface.

More than half of all S&P 500 members are stuck in technical downtrends, i.e., their current price is below a falling moving average. That’s true whether you look on a short, intermediate, or long-term timeframe.

Information Technology is the clear outlier, and given that Tech accounts for more than a quarter of S&P 500’s market capitalization, we certainly can’t ignore the strength we’re seeing there. But the majority of sectors are facing some serious headwinds.

Moreover, it’s not just that those stocks aren’t improving. They’re actually getting worse. We’ve seen an expansion of new 52-week highs thanks to big breakouts in growth. But we’ve also seen an expansion of new one-year lows. The net number of new highs vs. new lows remains below zero – that’s not something you’d expect to see see in a bull market.

We’re seeing that weakness show up in the non-growth indexes. The Dow Jones Industrial Average, which is tilted towards value-oriented names, failed to break out above its own key resistance level last month. Not only has the Dow not moved higher along with the S&P 500 and the NASDAQ, it’s fallen.

The DJIA is in negative territory for 2023.

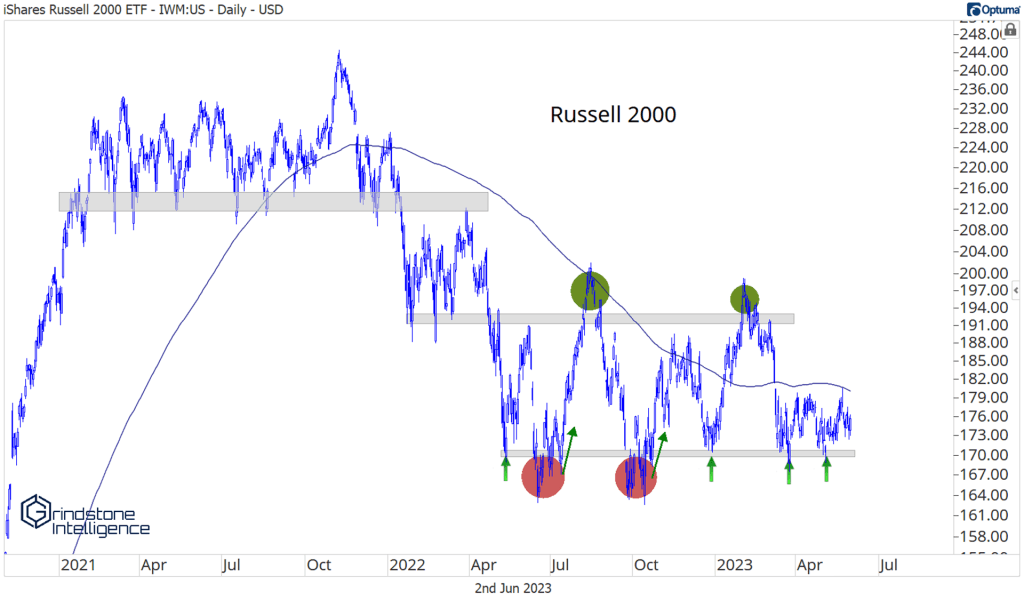

Things are just as ugly for small caps. The Russell 2000 is much closer to new 52-week lows than to setting new highs.

We can take heart in the fact that the Russell isn’t getting worse. True, the index is stuck below a falling 200-day moving average, so we can definitively rule out an uptrend. But prices are at the same level they were last May, a level of support that’s held for over a year.

Unsurprisingly, those April lows happen to hold a bit of historical significance as well. That’s also where small caps peaked just prior to the COVID-induced bear market of 2020. Price has memory.

Yes, breadth stinks. Leadership is narrow. The market is top-heavy. But don’t fight the tape.

Poor participation rates can be corrected in one of two ways: the leaders can catch down (bearish) or the laggards can catch up (bullish). Thus, weak breadth alone isn’t a sell signal. Instead, it’s simply a warning sign that tells us to use caution. Right now, the NASDAQ and S&P 500 are both breaking out. As long as that’s the case, we need to take a bullish approach toward stocks.

The big question, though, lies in what happens once those big growth names stop to catch their breath. Will money rotate into the laggards? Rotation is the lifeblood of a bull market. Or will a lack of leadership cause prices to fall below support?

The Russell 2000 is the one to watch. If an entire index is breaking down to multi-year lows, we won’t be able to brush off weak breadth anymore. After all, price is king.

We write about some of our favorite stocks and share other investment ideas each week. Here are links to our most recent sector and asset class reports.

(Premium) FICC in Focus: Gold Breakout on Hold, Dollar Bounces Back, Rates on the Rise

(Premium) Consumer Staples: Rejected Again

(Premium) Time for a Bounce in Utilities?

(Premium) Time to Buy the Beaten Down Financials?

(Premium) Real Estate Stocks in a World of Hurt

(Premium) If You Can’t Beat ’em, Join ’em

(Premium) Health Care Stocks Out of Breadth

(Premium) Communication Services: What’s Not to Like?

(Premium) Consumer Discretionary Coiling Up

(Premium) Energy Stocks Struggling to Find Their Footing

(Premium) Mixed Bag of Materials

(Premium) Industrials Searching for Support

The post June Technical Market Outlook first appeared on Grindstone Intelligence.