The Truth About Long-Term Returns – U.S. Bonds

Bonds are a staple of investment portfolios in the modern era. They don’t just help to offset the volatility associated with stocks. Since January 1926, an investment in long-term (20-year), risk-free U.S. Treasury bonds would have annualized at 5.70%. Nearly 6% per year from an investment guaranteed by the United States Government sounds like a pretty good deal, especially in today’s world of near-zero interest rates. The performance certainly deserves some credit for popularizing the “60/40” portfolio. But alas, things are not always what they seem.

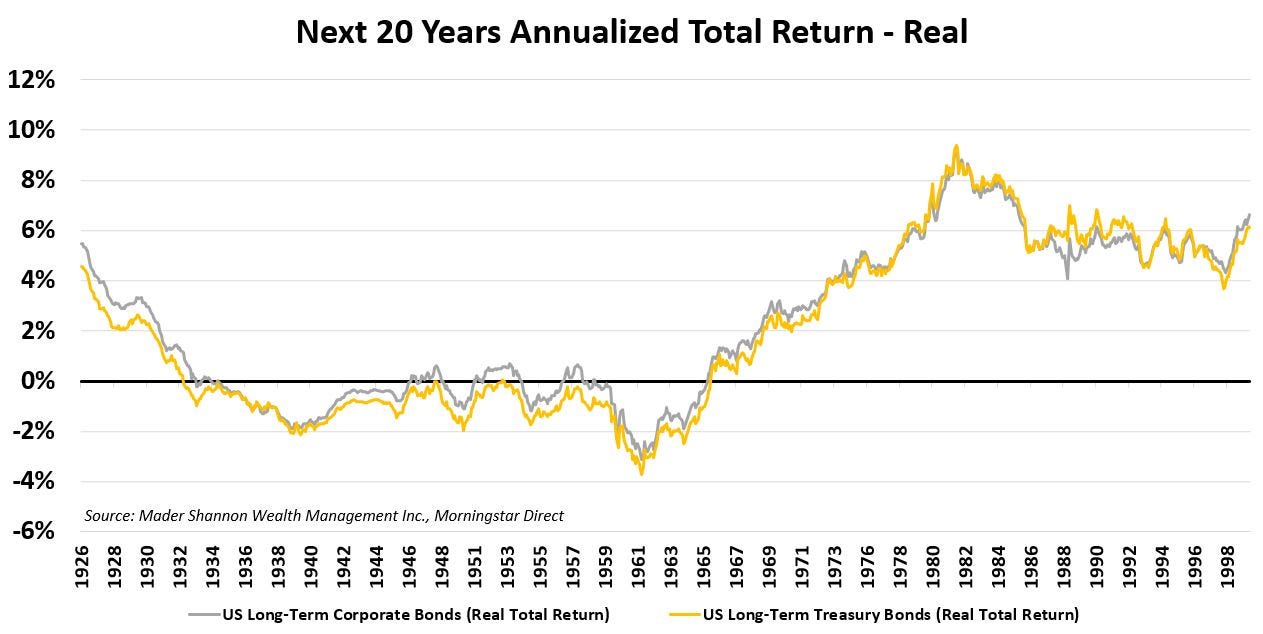

Over the last 100 years, long-term bond investing in the U.S. resulted in quite different outcomes for investors, depending on when they started. Many investors today have never experienced a true bear market in bonds. In the early 1980s, interest rates peaked near 15%, and have fallen steadily since. Not only did bond investors of the 80s and 90s get to purchase abnormally high yielding bonds, but they also benefited from capital appreciation related to falling rates. Additionally, they invested in a world where inflation was falling.

Inflation is the arch-enemy of bond investors. Since 1926, inflation has chipped away half of the 5.70% annual return achieved by U.S. bonds, resulting in a more sobering 2.76% return per year in real terms. Unsurprisingly, inflation took the largest toll during the 1970s and early 1980s, but when rates are low, even subdued inflation has an impact.

The impact is clear in the decades prior to the 1980s. In fact, buying long-term bonds was a remarkably terrible decision from the 1930s throughout the 1960s. The chart below depicts the real annualized return for someone that invested in bonds for a 20 year period. Note that while the average annual return (inflation adjusted) over the entire period was 2.76%, hardly anyone with a 20 year time horizon actually experienced that 2.76%.

As one of the aforementioned investors that’s never seen a bear market in bonds, it’s hard to fathom losing nearly 4% per year for 20 years. Moreover, it highlights just how remarkable the interest rate environment of my lifetime has been. Returns are positive for investors of the 1920s, but that’s largely a result of deflation in the 1930s. Putting that aside, virtually ALL of the cumulative real returns for bonds over the past 100 years have been achieved in the last 40 alone.

To further illustrate the true impact of bond returns, imagine you made a $1 per month contribution for 20 years. By the end, you’ll have contributed $240 to your ‘bond retirement fund.’ Investors that started in 1961 had less than $150 in equivalent dollars after 20 years of saving and contributing. Alternatively, an investor in 1977 would have ended with more than $600.

A few months ago, I discussed how ‘average returns’ in the stock market can be misleading. The same holds true for bonds. In investing, there are no guarantees of success or failure. Whether you’re a long-term investor, trend following speculator, or momentum-chasing day trader, we’re all playing a game of market timing.

If you missed my reviews of U.S. stock market returns, be sure to check them out here and here.

Nothing in this post or on this site is intended as a recommendation or an offer to buy or sell securities. Posts on Means to a Trend are meant for informational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in posts. Please see my Disclosure page for more information.

The post The Truth About Long-Term Returns – U.S. Bonds first appeared on Grindstone Intelligence.