Mid-Month Macro Update

Closing the Book on Inflation

The market’s inflation story has run its course.

Yes, inflation is still much too high. At 5.3% on a year-over-year basis, Core CPI is still more than double the Federal Reserve’s 2% annual target. Even when we look at just the last 3 months and annualize that number, prices have proven to be quite sticky – they’re running at a 5% annual rate.

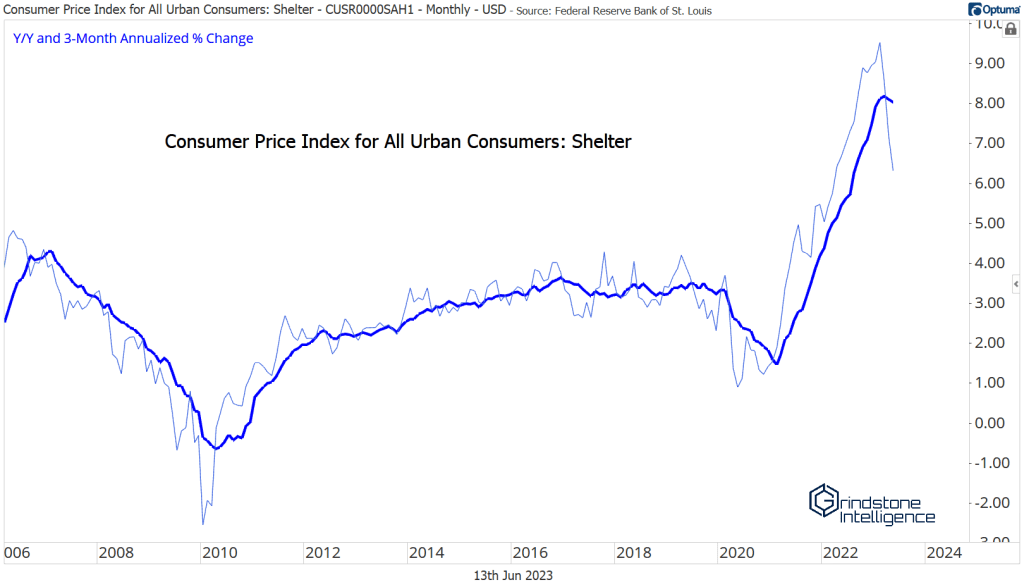

But measuring inflation is tricky, and these calculations have well-documented flaws when it comes to measuring housing inflation. Consider that back in July 2020, home prices began accelerating. By the end of the next year, home prices were rising at a pace of more than 20% per year, the fastest we’d seen in decades. Yet for the first 6 months of that historic rise, the CPI measure of shelter inflation was actually falling.

Part of the problem is that rent prices didn’t follow the same arc as homes prices, and rents are an important component in the CPI calculation. But the lag effect is still quite clear: home prices have a significant, but delayed impact on CPI for shelter. We saw the same phenomenon back in 2005, when home prices began to fall. It took almost 18 months for the inflection lower in home prices to show up in the measure of housing inflation.

Now, home prices are falling again. The peak in annual home price gains was more than a year ago, and the Case-Shiller National Home Price Index even went negative in recent months.

We’re finally starting to see those softer home prices show up in the CPI data. CPI for shelter has peaked, and on a 3-month annualized basis it’s already dropped more than 3.0% from its peak.

So why is all that important?

Because CPI ex-housing has been running at or below the Fed’s 2% target since last fall. The 3-month annualized change for this measure dropped to zero last September, and hasn’t really changed since. We’re now a whisper from hitting 2% on a y/y basis, too. Housing inflation is coming down, and inflation less shelter is already under control.

Energy prices coming down have been a big tailwind for lower headline inflation, to be sure. But even excluding that, as we do in the core measure of inflation we shared at the outset of this update, inflation is trending lower at a rapid pace. Shelter is a whopping 40% of core CPI. Currently running at 8%, that means shelter alone accounts for 3.2% of the 5.3% annual core rate. Everything else sums to just a 2.1% annual rate.

Inflation just isn’t what it was.

And the market has been saying that for nearly a year. Inflation was a problem for asset prices last year because higher inflation meant higher interest rates, and higher rates meant a stronger US Dollar. We shared with our subscribers many times an overlay of 10-year Treasury yields, the US Dollar Index, and the S&P 500 index, pointing to how tightly correlated the 3 were.

But last October (coincidentally about the time it was reported that CPI less shelter had dropped to normalized levels) interest rates stopped going up, and so did the Dollar. Those correlations that mattered so much in 2022 have stopped mattering at all. Interest rates and stocks are now positively correlated, and the Dollar isn’t correlated with equities at all.

Similarly, the market has been discounting actions from the Federal Reserve since about that time. When stocks troughed in October, money markets were baking in a terminal Fed Funds rate near 5%. Today, that terminal rate expectation is only modestly higher.

The FOMC’s most recent Summary of Economic Projections, published earlier this week, showed that participants expected to raise interest rates two more times this year. That would bring the overnight rate to a range of 5.50% – 5.75%, the highest in more than 20 years. But their decision to not raise rates after doing so at every meeting for more than a year is a clear signal that the hiking cycle is nearing its end.

Modest changes to the terminal rate aren’t the same as what happened in 2022, when the Fed went from talking about one 0.25% hike at year-end, to implementing the fastest tightening cycle in 40 years. Here’s a brief timeline recap for those that have blocked last year’s turmoil from their minds:

What could go wrong?

One, a huge inflationary shock that forces Jerome Powell & Co. to significantly alter their plans. Another couple of 25 basis point hikes by year-end isn’t catastrophic – but another 200 basis points in 2024? That’s a different scenario altogether.

The bigger risk, though, is that the Fed has already gone too far. The nation’s monetary authority has a long and storied history of tipping the economy into recession. Perhaps they’ve done it again?

Recession has admittedly been top of mind since last year, and doomsdayers have time and again been forced to push back their expectations of an economic downturn. This year, with the stock market rallying, many economists and strategists have pulled a recession out of their forecasts entirely. The housing market has recovered, unemployment remains low, and consumers are still spending money. All is well.

We aren’t trained economists here at Grindstone, and we aren’t in the business of forecasting recessions. Professional economic forecasters have a habit of seeing recessions that aren’t there and missing recessions that are right in front of their eyes. It’s not a knock on their credentials. It’s just that the economy is huge and incredibly hard to predict.

What we do know is that asset prices don’t tend to do well during recessions, and we haven’t seen historical examples of the stock market bottoming before a recession even begins. If we are headed for a recession, stock prices are most likely headed lower.

The other thing we know is that you can’t have a recession if everyone has a job. Jobless claims remained at incredibly low levels all throughout 2022, and that was a big reason why the economy kept chugging along in spite of the Fed’s policy actions.

Now, though, claims are on the rise. Excluding the pandemic period and a brief aberration in 2017 due to hurricanes Harvey and Irma, Initial Jobless Claims just touched their highest level since 2016.

And while the level of continuing claims remains near historically low levels, the 6-month change in claims has already reached a level consistent with prior recessions.

The consumer has been driving the US economy, and they’ve been able to do so because 1. They have jobs, 2. They’ve still got excess savings from the pandemic, and 3. Debt service levels were low. Now, those excess savings are drying up. Student loan payments are set to resume later this year, and revolving debt levels are back on the rise. Is unemployment the next shoe to drop?

We don’t know. We’re not economists. We aren’t predicting a recession.

We aren’t ruling it out, either.

A Look at What’s Ahead

The post Mid-Month Macro Update first appeared on Grindstone Intelligence.