Monday Morning Grind - 11/13/2023

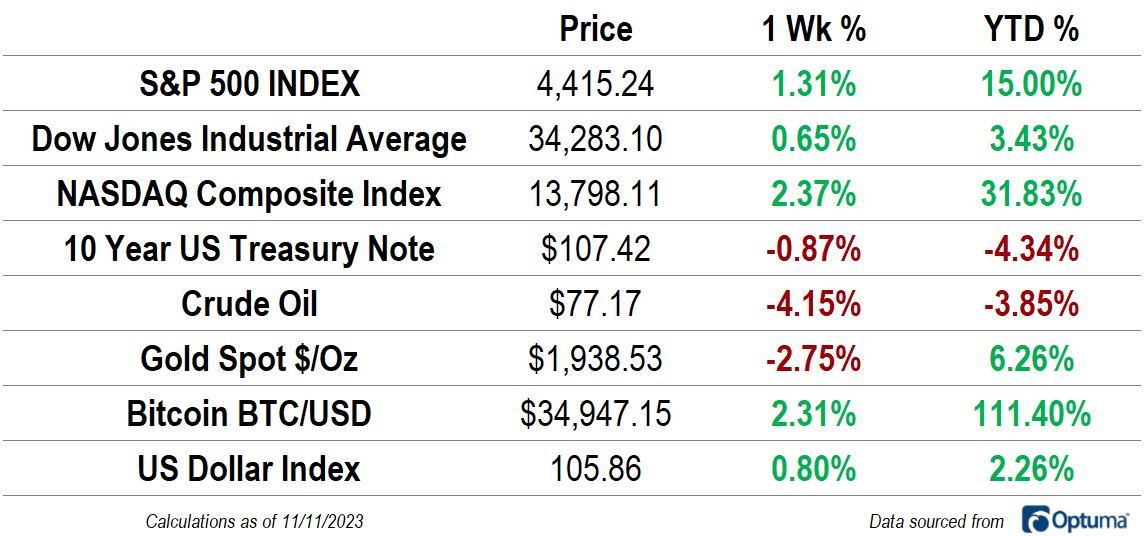

The S&P 500 rose for the second straight week and the NASDAQ Composite had its highest weekly close since September 1st. The NASDAQ’s rally pushed the index back above 30% for the year. The Dollar Index had its best week in 2 months as interest rates rose modestly, and that helped to drive a 4% decline in the price of crude oil and a 2.8% decline in the price of gold.

Jerome Powell didn’t close the door on additional interest rate hikes when he spoke last week, but as far as fed funds futures markets are concerned, the peak policy rate is in. Futures are pricing in just 15% odds of an additional 25 basis point hike by the end of January, but 50% odds of a cut by the middle of the year.

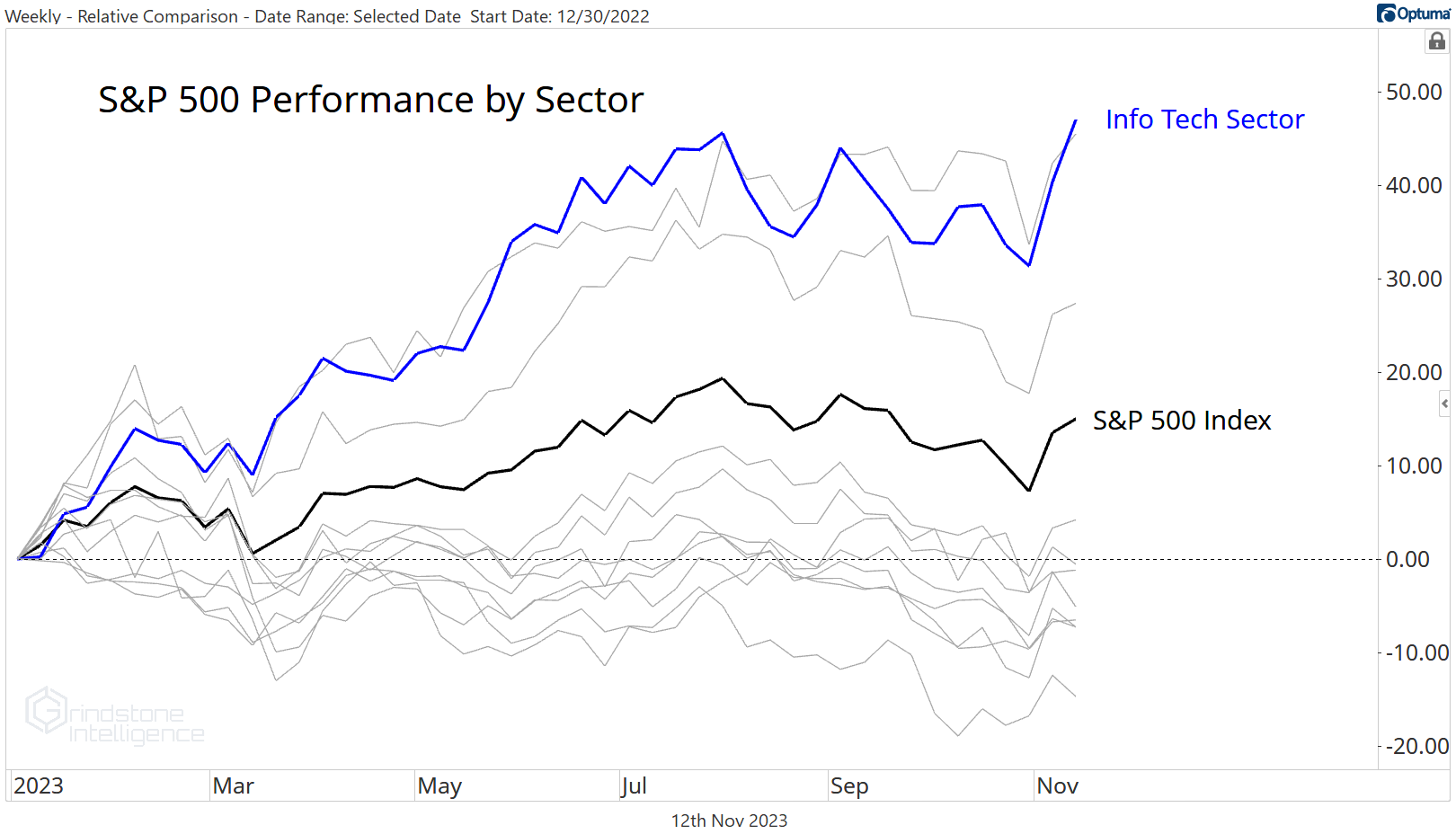

Meanwhile, Tech is back. Last week, the Information Technology sector had its best ever weekly close. That took the sector’s year-to-date gain to a whopping 47%. Meanwhile, just 3 other of the S&P 500’s 11 sectors are in positive territory for 2023.

Tech is a risk-on sector that tends to be a leader during extended market rallies, so seeing Tech lead now implies that investors are discounting the likelihood of a renewed bear market. Still, it’s unusual to see such a distinct bifurcation in sector performance this late in the year.

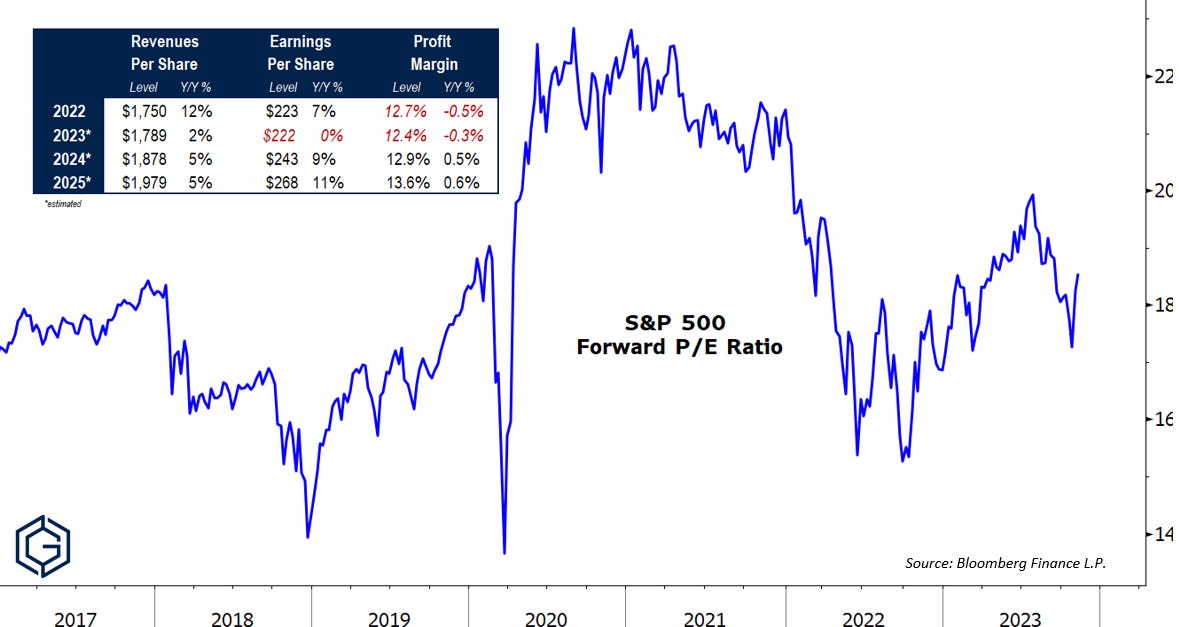

Earnings Expectations and Valuation

The 2022 bear market decline was not driven by a deterioration in corporate earnings. Though stock prices dropped well over 20% from their peak to trough, expected future earnings remained stubbornly high. That divergence pushed the S&P 500 forward price-to-earnings ratio from more than 20x (a level previously seen only during the late-1990s) to 15x (a level in-line with historical averages).

So far, 2023 has been the opposite experience: stock prices are up, but earnings are not. Profits began to stabilize in the most recent quarter after 3 consecutive periods of declines, but earnings projections for next year have started to deteriorate. With the market’s rebound over the last few weeks, valuations have climbed to roughly 18.5x next year’s earnings. That’s far from cheap when compared to historical norms.

What’s Ahead

Here’s the economic calendar for the week ahead