Monday Morning Grind - 12/4/23

Value > Growth

Week in Review

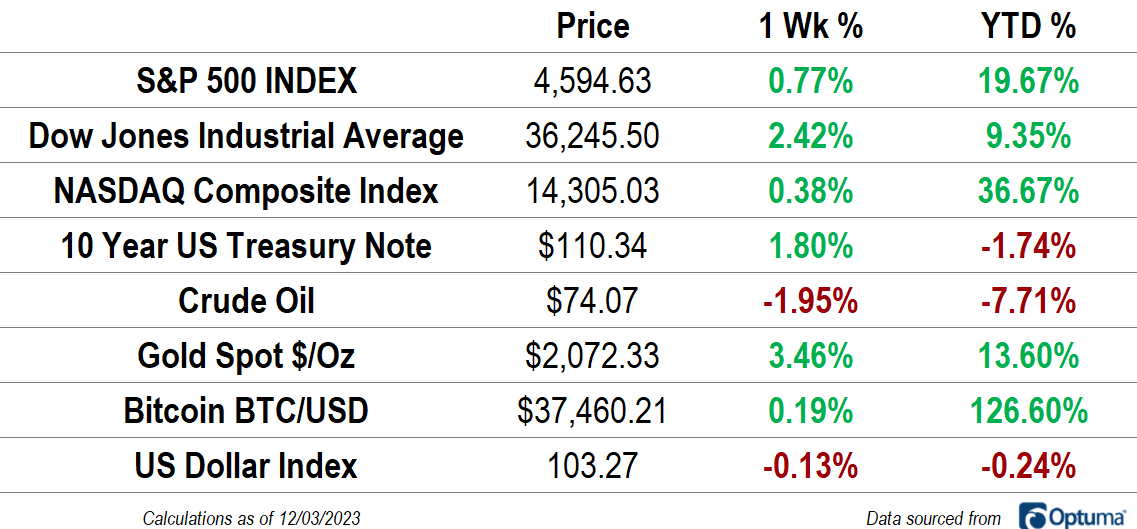

The Dow Jones Industrial Average climbed 2.4% last week, ending just a quarter percent shy of the all-time weekly closing high it set all the way back in January 2021. Gold, meanwhile, stole the show, jumping 3.5% for its best weekly close ever. Propelling gold has been a US Dollar index that slid for the third straight week, which itself was driven by a resumed downturn in interest rates.

The stage is set for value stocks to lead in December. Over the last 20 years, Value stocks have outperformed Growth in 61% of Decembers - that’s the best win rate for any month. Favorable seasonality for Value couldn’t be coming at a better spot, either: The Russell 1000 Growth vs. Russell 1000 Value ratio is reversing at the same place it did back in 2020 and 2021.

Market Internals

Breadth was a concern for most market watchers throughout March, April, and May, as the rally in growth stocks obscured lackluster performances from value-oriented names during the spring. After index-level declines in August, September, and October, breadth was as weak as it had been all year. Stocks had one of their best months ever in November and the S&P 500 surged to its highest weekly close in over a year, but many stocks are still refusing to participate: less than 2/3 of S&P 500 members are above their 200-day moving average.

Long-term trends are healthiest in the Financials, Industrials, and Information Technology sectors, where more than 75% of constituents have moved above their long-term moving averages. Traditionally considered a risk-off area, the Consumer Staples sector is the most weakly positioned. Just 26% of stocks in that group are in long-term technical uptrends.

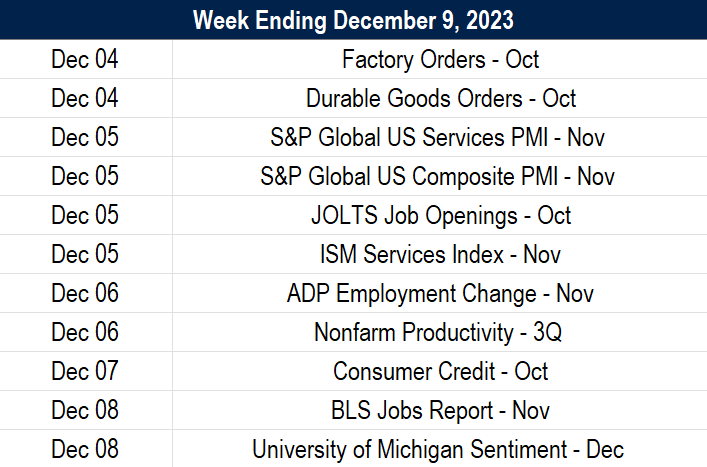

What's Ahead

Here's what to watch in the week ahead: