Not Out of the Woods Yet

Stocks have embarked on an impressive rally since their mid-June lows. The growth-oriented Nasdaq Composite has led the charge, rising 22%, with the S&P 500 index up 16%, and the value-tilted Dow Jones Industrial average up 13%. A simple yet all-important question faces investors and traders these days: Is this just a vicious bear market rally, or is it the start of a new bull market?

We can’t know the answer to that question, but we can be sure of something else. This rally has been broad.

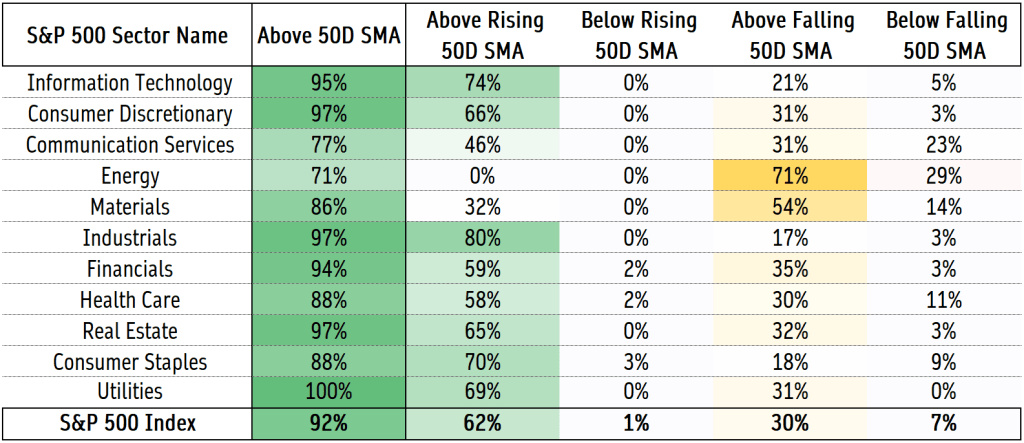

One of the most universal tests of an uptrend is to look at a stock’s price in relation to a moving average. As of Friday’s close, 92% of all S&P 500 stocks were above their 50 day moving average. That’s impressive, especially for an index that was indisputably in a bear market just two months ago.

But we can take things one step further. I like looking at both the price in relation to its average and the slope of the moving average. It gives us an even clearer picture. A stock whose price is above a rising moving average cannot be in a downtrend, and vice versa – a stock whose price is below a falling moving average cannot be in an uptrend.

Today, nearly two-thirds of stocks in the S&P 500 index are above rising 50 day moving averages. Just as telling, only 7% of index constituents are below falling 50 days.

By these measures, Energy is the weakest sector on a short-term basis. None of its members are above a rising 50 day moving average, and 29% are below a falling moving average. Surprisingly, despite Nasdaq names driving the rally off the lows, the strongest technically positioned sector is Industrials. Eighty percent of Industrials are structurally in short-term uptrends.

We can’t ignore the strength and breadth of the last two months of market action, but we aren’t out of the woods yet. Long-term trends for most stocks are still negative. Fifty-six percent of stocks are below their 200 day moving average and half of the benchmark S&P 500 is still solidly in downtrend territory, with a price below a falling 200 day average.

On this longer-term basis, the Communication Services and Consumer Discretionary sectors are still in critical condition: roughly 80% of each are stuck in downtrends. Energy stocks look healthy based on this technical measure, despite their relative weakness in the shorter-term. But in the aggregate, it’s defensively positioned sectors like Utilities and Consumer Staples holding up the average statistics.

If this really is a new bull market, we’ll need to see more structural improvement from risk-on areas of the investment landscape. Stay tuned.

Nothing in this post or on this site is intended as a recommendation or an offer to buy or sell securities. Posts on Means to a Trend are meant for informational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in posts. Please see my Disclosure page for more information.

The post Not Out of the Woods Yet first appeared on Grindstone Intelligence.