(Premium) November FICC Outlook

Currencies

The bull case for stocks still rests on the backs of the US Dollar and interest rates. The Dollar showed its first signs of weakness in months when it (barely) fell through a prior swing low. That’s been a major tailwind driving stocks for the last few weeks, and the outlook seems pretty simple. If the bottom is in for stocks, the top is in for the Dollar.

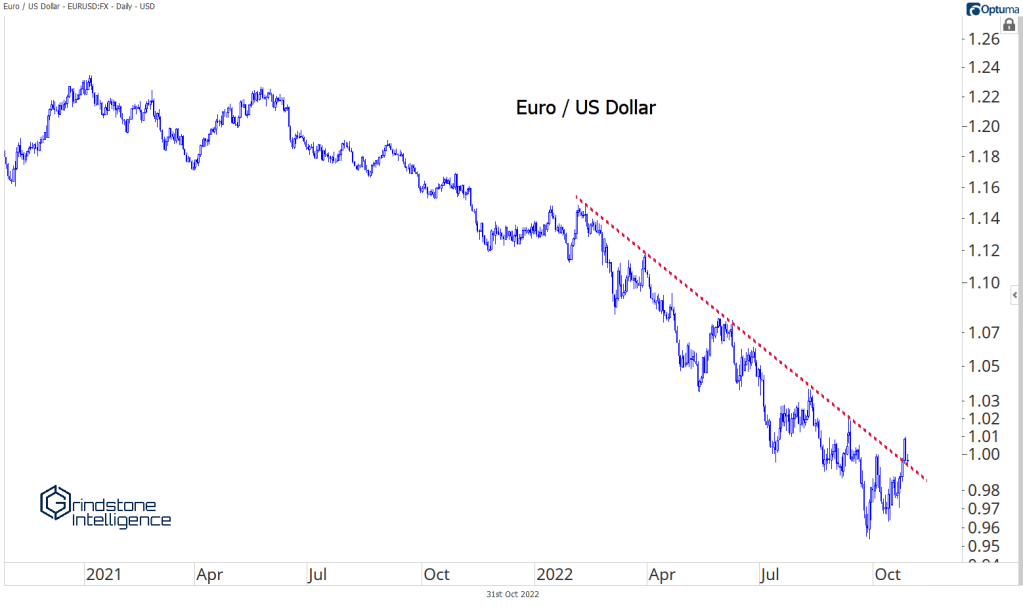

The weakening trend is most apparent in the Euro/Dollar exchange rate, where the year-to-date downtrend line is under assault. The cross is back to parity.

Fixed Income

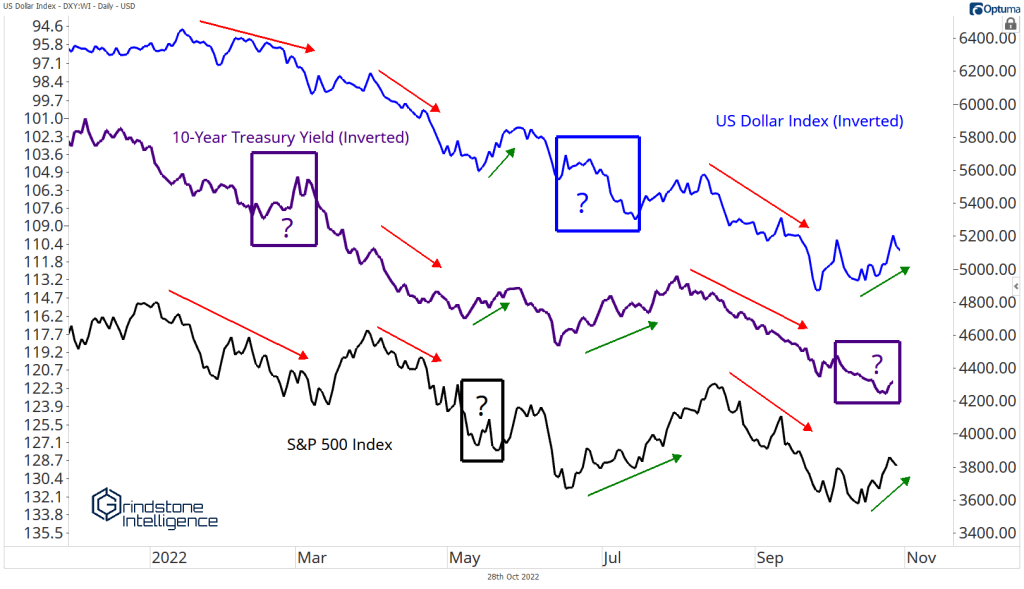

Interest rates are more concerning – they haven’t confirmed the move in stocks and currencies. Check out how closely the three have moved together this year.

We’ve seen one of the three do its own thing at various times, but it’s always been the majority that rules out. If history were to repeat itself, yields should fall. But the bond market is said to be wiser than the rest – does it know something we don’t?

Maybe. But a relief rally seems likely at this point. Ten-year yields just declined for 12(!) straight weeks. And last week’s bullish candle fully engulfed the body of the prior week’s decline – a classic reversal pattern.

There are also signs of a reversal in high yield bonds. HYG is back above its June lows, where it got rejected in early October.

And weekly momentum has put in a huge bullish divergence. We still need to see full confirmation from price, which wouldn’t happen until the ETF gets above $80, but even a mean reversion rally within this longer-term downtrend would be supportive for stock prices.

Bitcoin

Bitcoin has been boring. Volatility in the asset has completely dried up, and we’re still holding up above support in the 18000 range. The trend is lower, and consolidations like this should resolve in the direction of the underlying trend. But we never want to short a dull market. Bitcoin is a no-touch for now.

Precious Metals

Gold is a no-touch, too. Stuck below a ton of overhead resistance at 1700, there’s really no reason to be long from a near to intermediate term perspective. The lack of acceleration on the downside, though, raises some questions about being short the yellow metal.

The other red flag for precious metal bears is in Silver. Silver and Gold tend to be highly correlated, but Silver tends to move in greater magnitudes. As such, when the precious metals space is under pressure, Silver tends to lag, but it outperforms during bull markets.

With Gold breaking to new 52-week lows in October, we should have expected Silver to do the same. Instead, it’s working on what looks like a rounded bottom at multi-year support.

Silver and Gold are telling us different stories. We’re better off waiting for their trends to align before getting involved.

The post (Premium) November FICC Outlook first appeared on Grindstone Intelligence.