(Premium) FICC in Focus: Gold and Crypto Up, Dollar and Rates Down

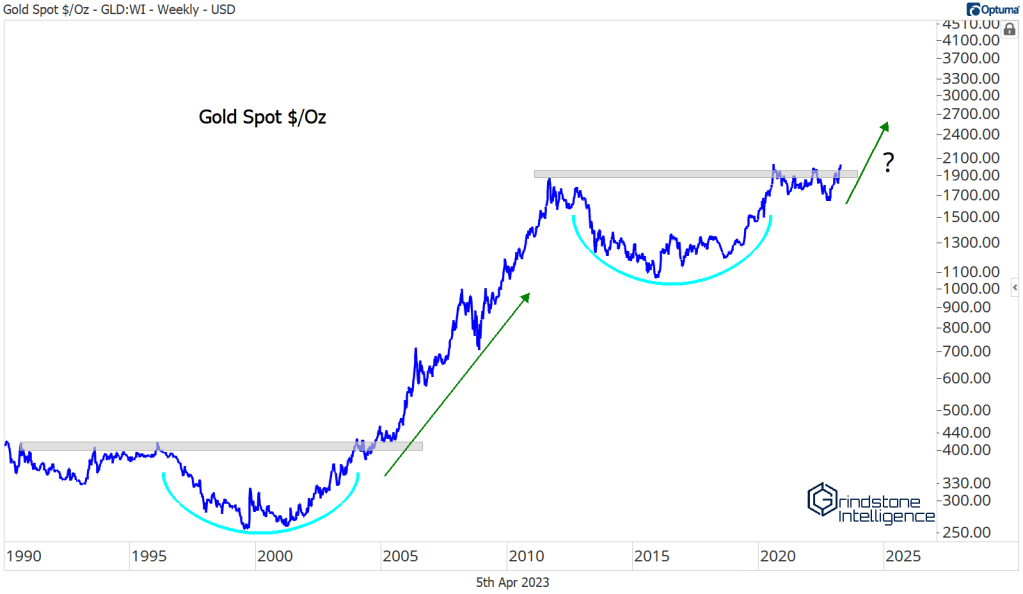

From 1990 to 1999, gold prices dropped by 40%. Over that same period, stock prices quadrupled. If Twitter was around back then, I bet the sentiment back then would look pretty similar to the kind of things we see and hear today: “Only old people and conspiracy theorists hold gold. Why would you hold a non-productive asset when you could own a piece of this high-flying growth stock or this new, disruptive technology?” And given the performance of gold vs. stocks over the last decade, who can blame them? Gold has gone absolutely nowhere since its 2011 peak. The S&P 500 has risen 250%.

I wrote a few weeks ago about a recent conversation with a financial advisor. When I mentioned gold, he announced proudly that he’d never allocate his clients toward precious metals. Stocks would invariably outperform over any meaningful period, he assured me. He must have forgotten about the 2000s.

It shouldn’t be surprising. He’s not yet 40, and most people in his role don’t bother learning market history beyond what’s needed to sell a product. I’m not yet 40 either, but at least I know better than to believe that the last 15 years are a representative sample of all modern history.

Gold rose from roughly $250/oz in 1999 to $1,900/oz in 2011 – a return of 650%. It outpaced the S&P 500 by 800%. If you were an asset allocator during that period and weren’t exposed to gold, you probably weren’t having much fun.

We believe gold could be headed for another run like that.

Mark Twain said history doesn’t repeat itself, but it does often rhyme. Look at what gold has done over the last decade, then compare that to the 1990s. See how similar they are?

Both saw 40% declines and bases that lasted for more than 10 years. Both periods were marked by the dominance of growth stocks and rising equity valuations. Why can’t both be followed by huge gains for gold?

The long-term narrative only works if gold is setting new highs, though. Without that, we’re still technically stuck in this long-term consolidation range. So let’s take a look at how things are shaping up in the shorter-term.

The trend here is not down. Prices just set new 52-week highs, and that’s not something you see in downtrends. But we can’t signal the all-clear with prices still stuck below resistance from those 2020-2022 highs.

This is the third attempt to break 2100 – why should this time be any different? For one, the more times a level is tested the more likely it is to break. Each time buyers push prices up to that level, they absorb more supply. Eventually, there’s no one left to sell. Also, last year’s failed breakdown is the perfect catalyst to get us out of this range. When gold was beneath the 2021 lows in November, we wrote the following:

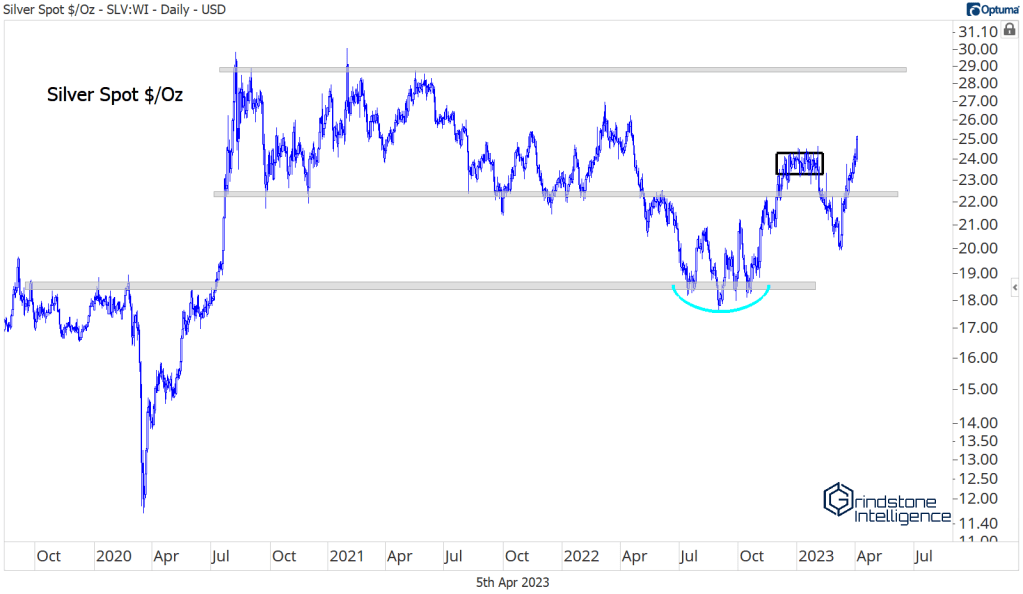

“The other red flag for precious metal bears is in Silver. Silver and Gold tend to be highly correlated, but Silver tends to move in greater magnitudes. As such, when the precious metals space is under pressure, Silver tends to lag, but it outperforms during bull markets.

With Gold breaking to new 52-week lows in October, we should have expected Silver to do the same. Instead, it’s working on what looks like a rounded bottom at multi-year support.”

From failed moves come fast moves in the opposite direction, and that’s exactly what we got. So often, those failed moves are the catalyst for a trend change, and we think it could be enough to push gold to new all-time highs.

If it is, we there’s a lot more potential upside. We’re targeting 3170 on a breakout above 2100. That’s the 1794% Fibonacci retracement from the 1990s decline. Prices have respected these retracement levels all the way up: The hiccups in 2006 and 2008 occurred near Fib levels, the ceiling from 2013-2019 was the 684.4% retracement, and right now, were stuck below the 1109% retracement. It would make a lot of sense to go up and touch the next one.

We won’t be able to get there without participation from silver. Just as silver tipped us off in November, it was screaming all throughout January that gold’s rally would fail. After a weak February for both metals, things are back on track. Silver is nearing new 52-week highs of its own, and it’s outperformed gold by double-digits over the last month. That’s exactly the type of action we want to see – silver should lead gold during uptrends.

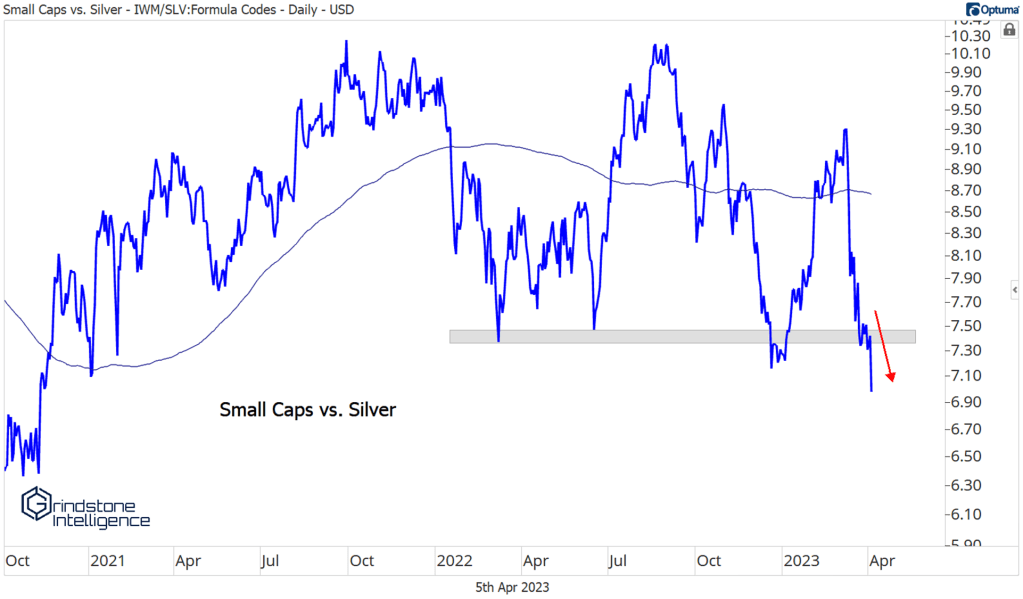

Silver’s not just showing relative strength among precious metals, either. It’s breaking out relative to small caps. Technician JC Parets calls the ratio of small caps to silver “the battle of the crazies”. Silver bulls and small cap bulls are a lot alike. When small caps lead large caps, it’s evidence of risk appetite for equities. When silver leads gold, it’s evidence of appetite for precious metals. You can find some real zealots in both the small cap and silver camps, so comparing the two offers an insight into asset class preferences. Right now, it’s signaling a desire to own precious metals. That’s what we want to see if gold is going to hit our target.

Precious metals strength reflects (at least in some part) a search for US Dollar alternatives. Despite its obvious flaws, I’m not one to root for the collapse of the US monetary system – if it does fail, I think we’ve all got some big, big problems. But I’m not so naïve as to think that’s what everyone else believes. Many crypto enthusiasts advertise Bitcoin as the currency of the future, so Bitcoin benefits from Dollar weakness in the same way that precious metals do. We’ve been neutral on Bitcoin between the 2017 highs and the 161.8% retracement of the 2017-2018 decline. It’s still stuck below 30,000, but we need to be approaching crypto from a bullish perspective if we’re above that level. A breakout would probably coincide with new highs for gold, too.

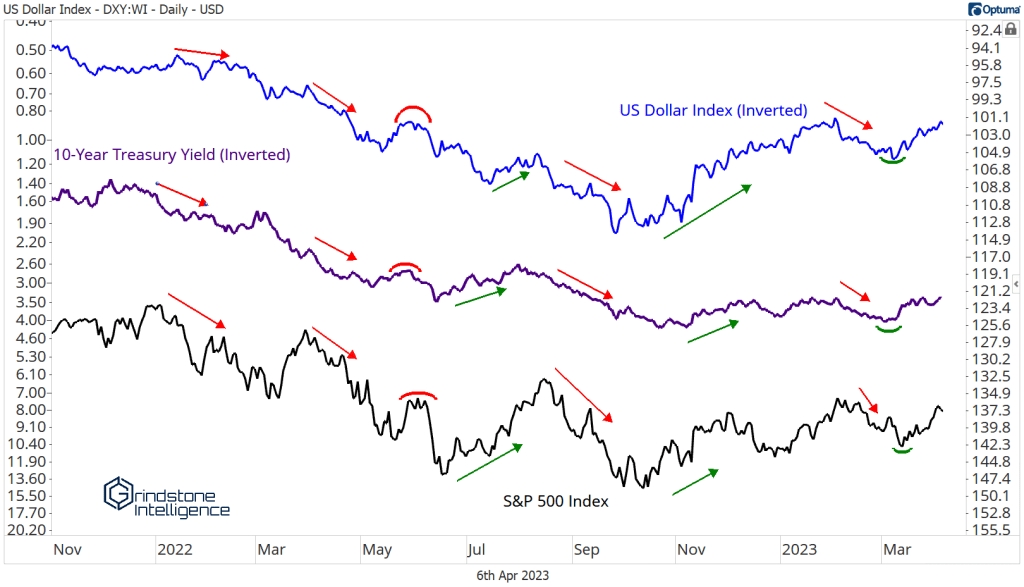

The Dollar outflows are having a clear effect on the Dollar Index. It’s down near 52-week lows and beneath support from the 2015-2021 highs.

There’s more to the Dollar’s weakness than the fear of a collapsing fiat regime. Interest rates in Europe and around the world are becoming relatively more attractive, so it would make sense to see some Dollar weakness. Europe’s policy tightening is just now hitting its stride. At the same time, Kuroda’s exit from the Bank of Japan at least introduces the possibility of a policy change in the world’s third largest economy. Meanwhile, the Federal Reserve is nearly done with hikes according to market rates.

Here’s a recap of the major policy and narrative shifts we’ve seen over the last 18 months.

Each time data strengthened or Fed officials gave hawkish guidance, rates rose, the Dollar followed, and stocks fell. Look at how closely the three have moved together.

Now it looks as though rates have peaked, thanks to the failure of Silicon Valley Bank. In the weeks prior the banking crisis, every piece of economic data pointed to stubbornly high inflation and a tight labor market. That pushed 2 year Treasury yields to the highest level since 2007 and implied a higher terminal point for the Federal Funds Rate target. In the weeks after the failure, though, 2 year rates have given back those gains and more.

Yields have fallen across the curve. Ten year Treasurys are breaking down to their lowest levels since last September.

Based on everything we’ve seen over the last year, that should be a bad thing for the Dollar and a good thing for stocks, right?

Maybe. Maybe not.

The correlations between equity prices, rates, and currencies aren’t quite as strong as they were.

Why might that be? Again, bank failures could be partially to blame. Higher rates and a stronger Dollar are still bad for stocks, just as they were last year. In that regard, nothing has changed.

The narrative around lower rates has. Throughout 2022, lower rates were reflective of softening price pressures and supported hopes that the Fed could softly land a hot economy. Fears of a deep recession are more in focus today. Deposits are flowing out of banks across the country and into money-market funds, and that disintermediation will force banks to pull back on credit issuance. Those types of credit crunches often lead to deep recessions, where the Fed will have a tough time keeping rates elevated.

Recessions just aren’t great news for stock prices, whether rates are coming down or not.

The post (Premium) FICC in Focus: Gold and Crypto Up, Dollar and Rates Down first appeared on Grindstone Intelligence.