(Premium) If You Can’t Beat ’em, Join ’em

I keep hearing and seeing the same complaints about Tech

“All the gains are coming from a handful of stocks”

“Breadth is too narrow”

“This is unsustainable”

Someday (perhaps soon), those concerns will prove to have merit. For now, we’re quite happy with the overweight rating we’ve had on Information Technology. Tech is still the top-performing sector on the year, followed closely by Communication Services and Consumer Discretionary. Those 3 are all outpacing the S&P 500’s 8% year-to-date gain by a healthy margin.

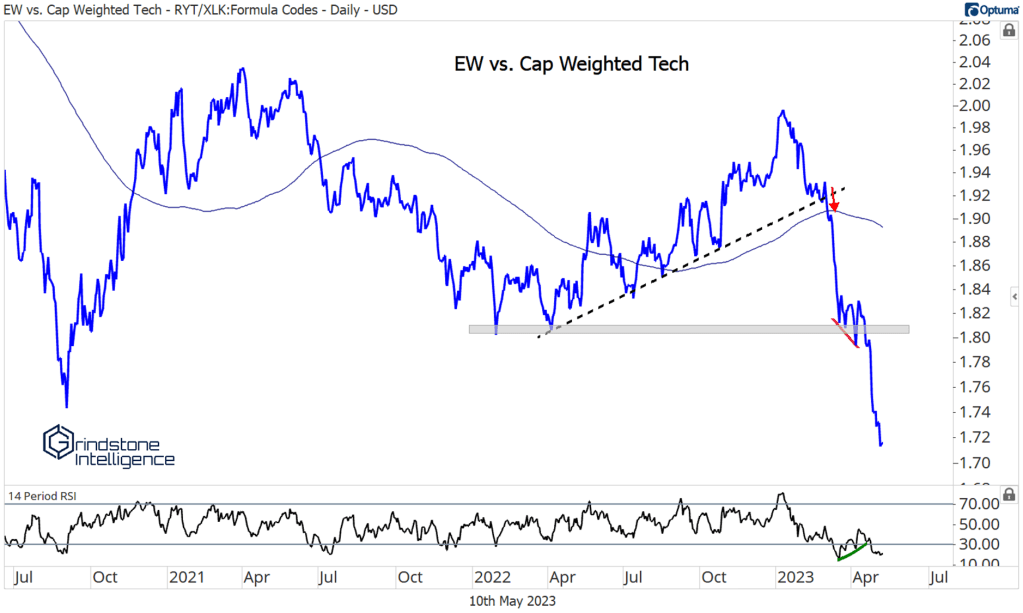

You may not like the dominance of large cap tech, but you have to respect it. We were skeptical ourselves in last month’s note, and we pointed out the ongoing bullish momentum divergence in ratio of equal weight tech vs. the cap weighted sector. But the strongest trends don’t care about momentum divergences, and price never confirmed our concerns. The EW index cratered to multi-year relative lows.

Narrow participation hasn’t hurt the sector’s performance relative to the rest of the market, though. Tech is knocking on the door of new all-time highs compared to the S&P 500.

For those of you who have followed our work for awhile, the chart below should look pretty familiar. It’s the Information Technology sector versus the S&P 500 index. Since September 2020, Tech has been in a sideways relative trend as it’s digested the internet bubble highs. Whenever you hear people say that technical analysis doesn’t work, try showing them this chart. Is it a coincidence that the ratio peaked at exactly the monthly highs from 2000 and reversed lower from that level 5 times over the past 3 years? Is it a coincidence that after breaking above that level in late 2021, the ratio then peaked at exactly the weekly highs from 2000?

In any case, after a failed breakdown in the first week of January 2023, we’ve seen a massive bullish reversal in Tech. It surpassed those dotcom monthly highs, and then successfully backtested them a few weeks ago. Mega cap dominance or not, we’re within striking distance of new all-time highs.

Apple, the largest and most important stock in the sector, is knocking on the door of new all-time highs, too. We don’t love the risk-reward setup with AAPL where it is today, but the stock is certainly not in a downtrend.

Microsoft is just as important. It ran into resistance at its August highs, and we noted in our last sector update that this was a pretty logical place for the stock to take a breather. Over the next week, it looked as though MSFT would do just that – then it reported earnings and gapped up to new 52-week highs. Again, this isn’t our favorite risk-reward setup. But if Microsoft is above $295, what is there to complain about? There’s nothing bearish about new highs.

We still like Motorola Solutions. It’s sitting near 52-week highs after spending more than a year stuck below the 261.8% Fibonacci retracement from the 2019-2020 decline. Only a handful of names in the sector are above their 2022 peak, and not many setups are cleaner than this one. If MSI is above $275, we want to own it with a target of $365.

Synopsys is another we’re watching. This one’s been a big leader within software, and it’s knocking on the door of another big breakout. The 423.6% retracement from the COVID decline has been the ceiling since late 2021. If it’s above those former highs near $380, we’re targeting the next Fibonacci retracement level from the 2020 decline, which is up at $519. We’re not ignoring the bearish momentum divergence that’s shaping up. Momentum divergences can be worked off either through corrective price action or through time. More and more, it looks like SNPS is choosing the latter.

ON Semiconductor showed relative strength all throughout the bear market of 2022. When the rest of tech was setting new lows, ON was breaking out to new highs. Price has been coiling up below the 423.6% retracement from the COVID selloff since early February, and we think a breakout comes sooner, rather than later. If it’s above $82, we want to be long with a target of $127, which is the next key Fibonacci retracement level. We’d be more concerned about the stock if it fell below $70.

All three of those names are near new highs, but we aren’t limited to looking at stocks that have shown multi-year relative strength. Applied Materials has put in a nice bottom since the October lows. The neckline from an inverse head and shoulders pattern offers near-term support and a clearly defined risk level at $110. If AMAT is below that level, we need to be wary of renewed weakness for both the stock and the sector overall. Otherwise, we’ve got an initial target of $145.

The post (Premium) If You Can’t Beat ’em, Join ’em first appeared on Grindstone Intelligence.