(Premium) Real Estate Sector Deep Dive – July

Slowly but surely, fears of a recession are fading from investors’ minds. Inflation is falling faster than just about everyone expected, and the path to a ‘soft-landing’ seems a lot clearer. Somehow, we even managed to shake off a banking panic earlier this year, thanks to aggressive ring-fencing actions and deposit backstops by policy makers.

Among the biggest risks that remains is in commercial real estate, where mass defaults have the potential to cause shockwaves throughout the economy. The epicenter is in office real estate, where remote work policies and evolving urban populations have pushed vacancy rates higher and property values lower. Those occupancy issues are mostly limited to office, but other issues like higher interest rates and tightening lending policies are more widespread.

As a result, Real Estate has been steadily underperforming the rest of the market since the Fed initiated its monetary policy tightening actions last year. The weakness pushed the sector to multi-decade lows.

We’ve traditionally categorized Real Estate as a boring, ‘risk-off’ sector, akin to Health Care, Utilities, and Consumer Staples, but all throughout 2022, Real Estate was indistinguishable from large cap growth. It was one of the more interesting relationships of the year.

As we turned our calendars to 2023, market leadership took a sharp turn in favor of growth stocks, as Information Technology, Consumer Discretionary, and Communication Services surged. Real Estate tagged along for the ride.

A sharp reset over the following months has the sector right back where it belongs.

The reason Real Estate looked so much like growth in 2022 was because of interest rates. Rising interest rates impact growth stock valuations and their future growth trajectories. For heavily indebted Real Estate stocks, higher rates threaten financing capabilities and debt service costs.

Interest rates stopped rising last year, though, removing much of the overhang for growth stocks. Stable interest rates, even high ones, can be managed by growth-focused business managers and investors. Unfortunately, elevated rates are still a problem for debt-laden Real Estate stocks, even if rates are stable.

That makes it tough to get excited about much in the sector, and a reason why we have an Underweight rating on the sector.

We know that stock prices tend lead fundamental improvement, though, and we stand ready to adjust our rating should trends improve. We’re just not seeing enough yet at the sector level.

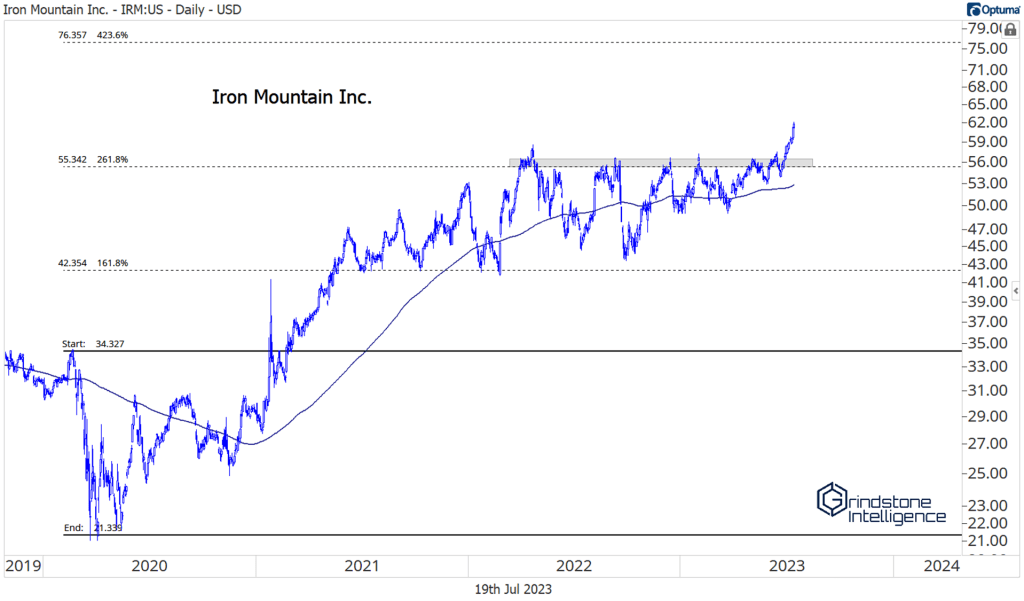

A few individual names are showing marked improvement, however. Iron Mountain finally broke out to new all-time highs. We’d been watching IRM closely, since it kept challenging those highs while the rest of the sector was falling apart. That’s the type of relative strength we like to see. Now that the stock is above $56, which is the 261.8% retracement from the COVID selloff, we can be long IRM with a target of $76, which is the next key Fibonacci retracement level.

We’d like it even more if it can resume its uptrend relative to the S&P 500, after being rangebound for the last year.

Avalonbay continues to work on a bearish to bullish reversal, and the risk is very clearly defined. We can own it above $185.

And CBRE is trying to set new 52-week highs as it challenges the 161.8% retracement from the 2020 decline. On a breakout, we’re targeting the 261.8% retracement, which is up at $122.

Despite a few names starting to perk up, we’re still skeptical about most of the group. Compared to the 10 other sectors in the S&P 500, Real Estate has seen the fewest number of stocks setting new highs – by a wide margin.

The post (Premium) Real Estate Sector Deep Dive – July first appeared on Grindstone Intelligence.