Rate Resets, Bank Failures, and an Expansion of New Lows

Were you able to keep up with everything that’s happened over the last week?

If you weren’t, don’t worry. In a year or two, you’ll be able to read all about it in a book that’s number one on the New York Times Bestseller list. And better yet, it’ll probably be riddled with insider accounts of how one of the largest bank failures in history came about.

The week seemed to begin like any other. The most interesting thing on the agenda was Fed Chair Jerome Powell’s semi-annual testimony in front of Congress – an occasion where he’d have the opportunity to adjust expectations for the upcoming FOMC meeting.

For his part, Powell lived up to the hype. In testimony before the Senate Banking Panel, he said that recent economic data would likely require a higher terminal Federal Funds Rate and could force the committee to reaccelerate the pace of interest rate hikes. Powell attempted to walk back those remarks somewhat on Wednesday when he appeared before the House, saying no decisions had been made about the upcoming FOMC meeting. But the damage was already done.

When the week began, the S&P 500 stood near 4050, 2-year Treasury yields were at 4.85%, and markets were pricing in a modest 0.25% hike at the March meeting. By the time Powell finished on Wednesday afternoon, though, stock prices were 2% below their Monday highs, that same 2-year Treasury yield was above 5% for the first time in more than 15 years, and a 50bps hike was fully baked in.

If the week had ended there, it might’ve been among the most eventful of the year. Instead, Powell’s words were a forgotten footnote just two days later.

On Wednesday evening, Silicon Valley Bank surprised investors by announcing plans to sell additional stock. They’d been forced to liquidate some holdings at a loss, and needed additional capital to fill the hole. By Friday morning, SVB was shut down and placed in FDIC receivership – the biggest bank failure since Washington Mutual in 2008.

So what the hell happened?

This wasn’t a repeat of 2008, when a housing collapse triggered a meltdown in the mortgage backed securities market, and the value of some banks’ assets fell below that of their liabilities (a solvency crisis). Nor was this Silvergate Bank, a much smaller, crypto focused bank that also went into liquidation last week after losses forced it to reassess its viability.

Instead, SVB fell victim to the age old enemy of all deposit-taking institutions: the bank run.

Banking’s basic business model presents a liquidity conundrum. Banks have short-dated liabilities (customer can take their deposits out at any time) but long-dated assets (your bank can’t call you up and demand you pay your mortgage in full this afternoon). If customers withdraw cash at a rate that exceeds the banks levels of reserves, the bank must cover the difference with its own capital OR sell those long-dated assets.

Enter Silicon Valley Bank. SVB specializes in banking for startups – the type of firms that burn through cash, but make up for it with venture capital funding that’s lured in by tantalizing growth prospects. Thanks to slowing activity and a weakening economic outlook, companies burned through even more cash. And for those same reasons, the funding environment became more difficult. Deposits at SVB shrank more quickly than the bank planned.

At the same time, the bank’s long-dated assets were under pressure. During the pandemic, SVB apparently loaded up on Treasuries and other low-risk assets yielding less than 2%. Thanks to out of control inflation and the Fed’s response, interest rates have sky-rocketed in the years since, pushing that book of bonds into the red.

Here, we have to know a little bit about banks accounting. Securities held on bank balance sheets can be classified in one of two ways: held-to-maturity (HTM) or available-for-sale (AFS). The bank’s capital position isn’t affected by market fluctuations in HTM securities, an important classification for banks – and for those Treasuries SVB was holding. Their pandemic era bonds were yielding a paltry 2% or less, but that was still higher than what SVB was paying depositors. So although the current market value of those bonds was significantly lower, holding them until they matured would still be a low risk and profitable venture. Unfortunately, when deposit outflows increased, SVB had to sell some HTM securities. And when that happened, a whole tranche of HTM securities now had to be re-classified as AFS and marked to the market, resulting in a significant loss.

That’s why SVB announced on Wednesday that they’d be selling additional stock to raise capital – they needed to fill the hole left in their balance sheet by the reclassification. With a successful capital raise it might have ended there.

Instead, things only got worse. With blood in the water, SVB customers were advised to start pulling what deposits were left. These were large corporations, whose deposits far exceeded the $250,000 protection offered by the FDIC – they had no interest in being left holding the bag. With even fewer deposits, SVB’s capital position worsened, and regulators stepped in to stop the bleeding.

Over the weekend, the contagion continued to spread. Signature Bank was shuttered, and the US Government has announced that they’ll backstop deposits for customers at both banks. Many investors aren’t waiting around to see which domino will be the next to fall – shares of First Republic Bank are down more than 70% as I write this morning.

This saga’s ending has yet to be written.

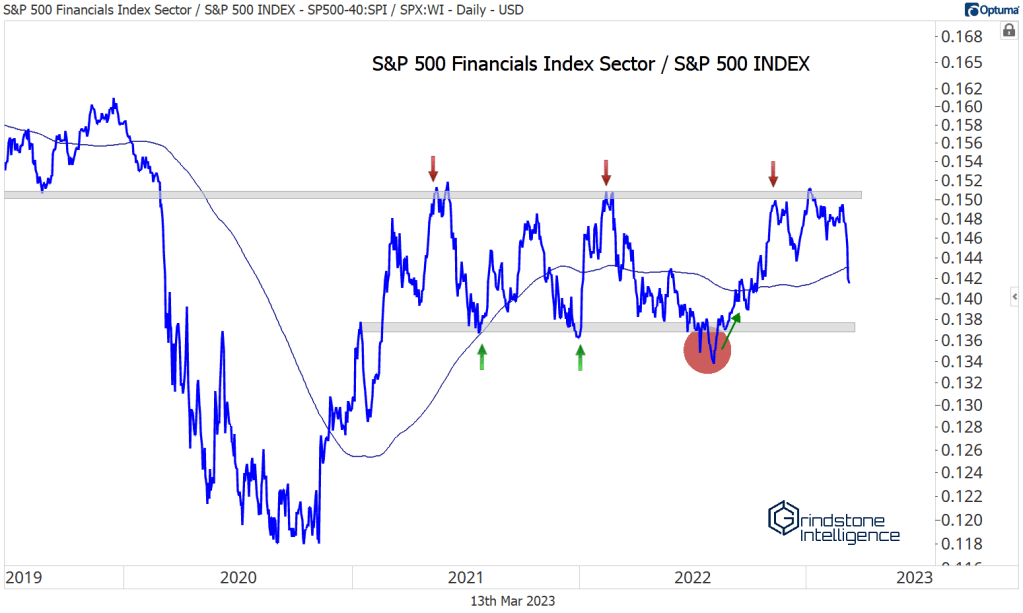

The calamity struck as the Financial sector was trying to break out of a multi-year base relative to the S&P 500. For the time being, a resolution from this range is on hold.

The S&P 500 Regional Banks sub-industry is to blame for the weakness, as it’s dropped to its lowest level since October 2020.

But the damage hasn’t stopped there. Bank failures – especially the failure of 2 large cap banks in 72 hours – have a way of making investors reassess risk across their portfolios. More S&P 500 companies set new 52-week lows on Friday than on any day since markets bottomed in October.

Unless this banking crisis is contained, expect more new lows to head this way.

The post Rate Resets, Bank Failures, and an Expansion of New Lows first appeared on Grindstone Intelligence.