Real Estate vs. Interest Rates - 12/22/2023

Top charts and trade ideas from the Real Estate sector

Note: There will be no note on Monday, December 25th. With the time you might have spent reading, take a moment instead to be thankful for the people in your life. Merry Christmas

The mean reversion in Real Estate is complete. Now what?

It all depends on interest rates.

Take the trend of the sector vs. the rest of the market, then overlay that with Treasurys - you’ll find a fair resemblance. When interest rates go up, Real Estate underperforms, and vice versa.

Higher interest rates are a two-fold headwind. One, they make fixed income more attractive to investors and lower the relative appeal of stocks with high dividend yields. Consider this: Two years ago, 10- year Treasury rates were just 1.5%, while the dividend yield on Real Estate stocks was among the highest in the S&P 500 at about 3%. Today, the risk-free Treasury yield is closer to 4%, while Real Estate pays one of the highest dividend yields of any sector at around 3.5%. For income-focused investors, there’s little comparison.

Second, rates are a problem for the business activities of real estate stocks, which tend to have high debt loads. Real Estate has just a 2.5% market cap share of the S&P 500, but it has a 5.5% share of net interest expense. By that measure, Real Estate stocks are already paying 2.5x more interest than the average S&P 500 company. Only the Utilities compare, and they’re even worse, with a ratio of interest expense to market cap share of 6x.

The Utilities have one distinct advantage, though. The weighted average maturity of debt for Utilities stocks is more than 13 years - double that of Real Estate at 6.7 years. That means Real Estate companies will be repricing their high debt loads at higher interest rates at a much faster pace.

To sum it all up, higher interest rates = bad news for real estate.

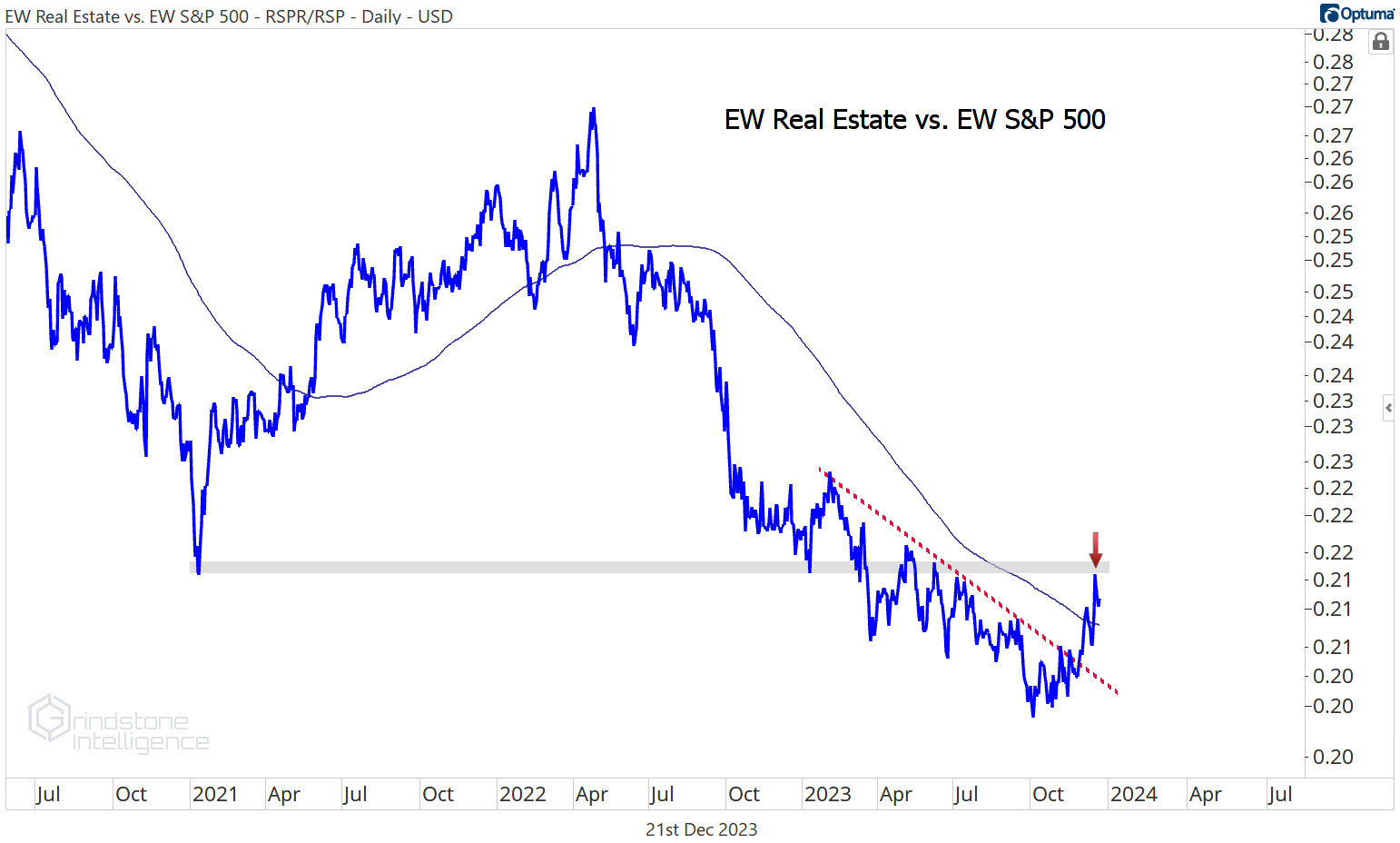

But higher interest rates haven’t been a problem lately - not since rates peaked at 5% in mid-October. True to form, Real Estate stocks have outperformed the S&P 500 by 10% since then, pushing the Real Estate/S&P 500 ratio right up to its 200-day moving average.

We’re left questioning whether this recent spate of outperformance is simply a mean reversion within an ongoing downtrend or the start of a much larger reversal.

It’s not so much a question of whether Real Estate stocks are poised for significant downside. That seems the least likely outcome. Here’s the sector on its own, now further above its 200-day moving average than at any point in nearly 2 years after a failed breakdown in October.

Momentum for the sector is bullish, too. A bullish divergence at the lows helped confirm the failed breakdown, and now RSI is more overbought than it’s been in years. Contrary to how it sounds, a stock or sector getting ‘overbought’ is actually a good thing. It shows that bulls are very much in control. Check out the last time momentum was this elevated, back in 2021. Prices ended up going a lot higher after those overbought readings.

So the question we have is not whether Real Estate sector prices go higher - the evidence indicates they most likely will - but whether they’ll continue to outperform the rest of the market. And from that perspective, we see some clear headwinds.

Check out the equally weighted Real Estate sector compared to the equally weighted S&P 500. Here we’re stripping away the outsized impact of the mega cap stocks and just comparing the underlying strength in Real Estate to the underlying strength in the S&P 500. The ratio has broken above the 2023 downtrend line, but it’s still stuck below the 2021 lows.

Those 2021 lows were a significant turning point, so we’d be surprised to see prices just ignore that level now. Perhaps Real Estate can complete the reversal and begin a new uptrend, but we think the least likely outcome here is that they do it right away. It’ll take some time to digest the level.

Of course, the market doesn’t care what we think. There’s so much data out there that we can always find evidence to contradict our views. The most convincing counter-argument for Real Estate is in strong breadth readings. Every single S&P 500 Real Estate stock is above its 50-day moving average, and all but one are above their 100-day. Both readings are the best of any sector in the index. That seems to favor continued outperformance.

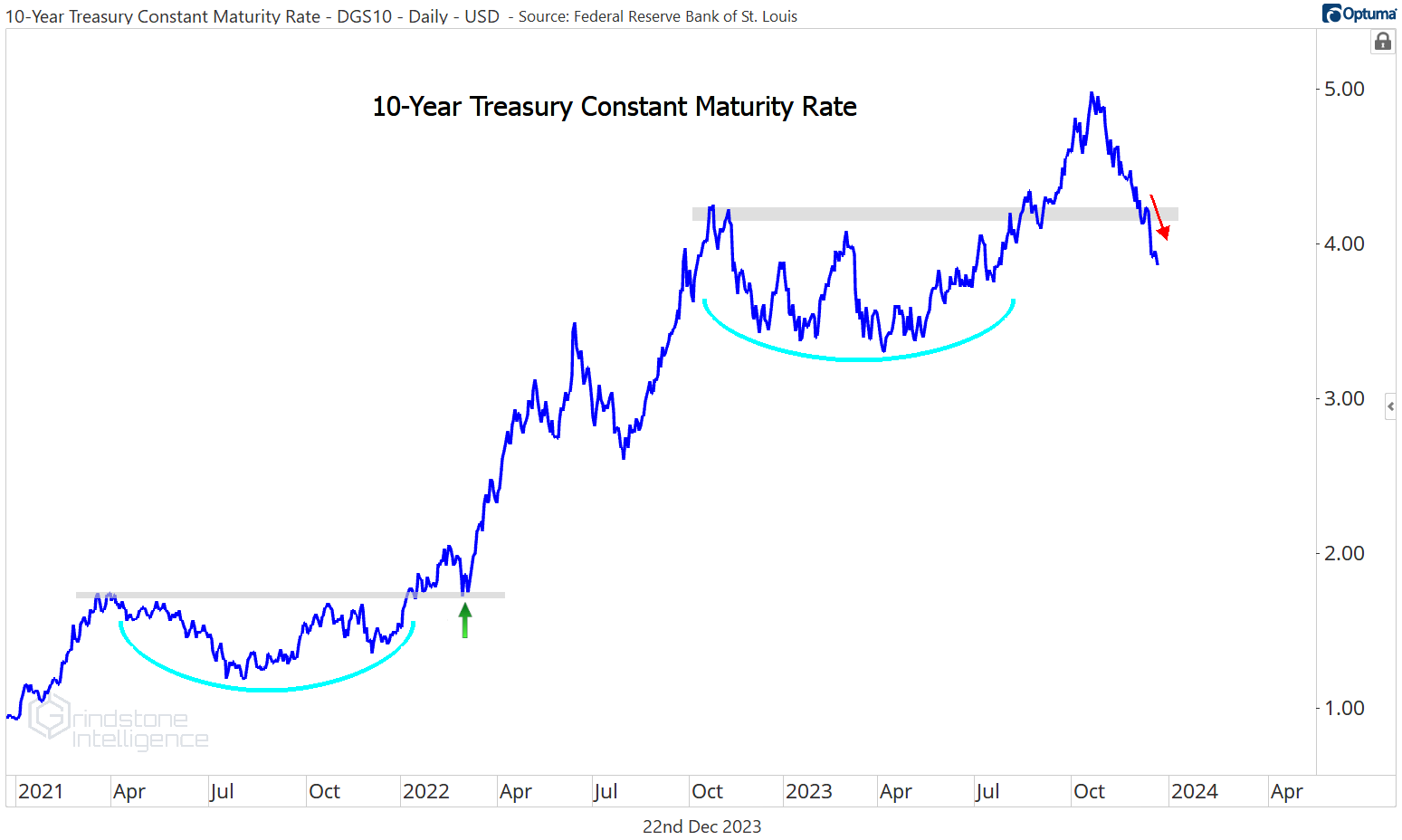

And of course, the trend in interest rates looks favorable for Real Estate stocks, too. Until mid-December, one could argue that the November drop in rates was simply a backtest of the breakout level, akin to what we saw back in early 2022. With yields convincingly back below their October 2022 highs, that thesis no longer holds water.

Interest rates may not be in a downtrend, but the uptrend is clearly broken. That’s good news for the Real Estate sector.

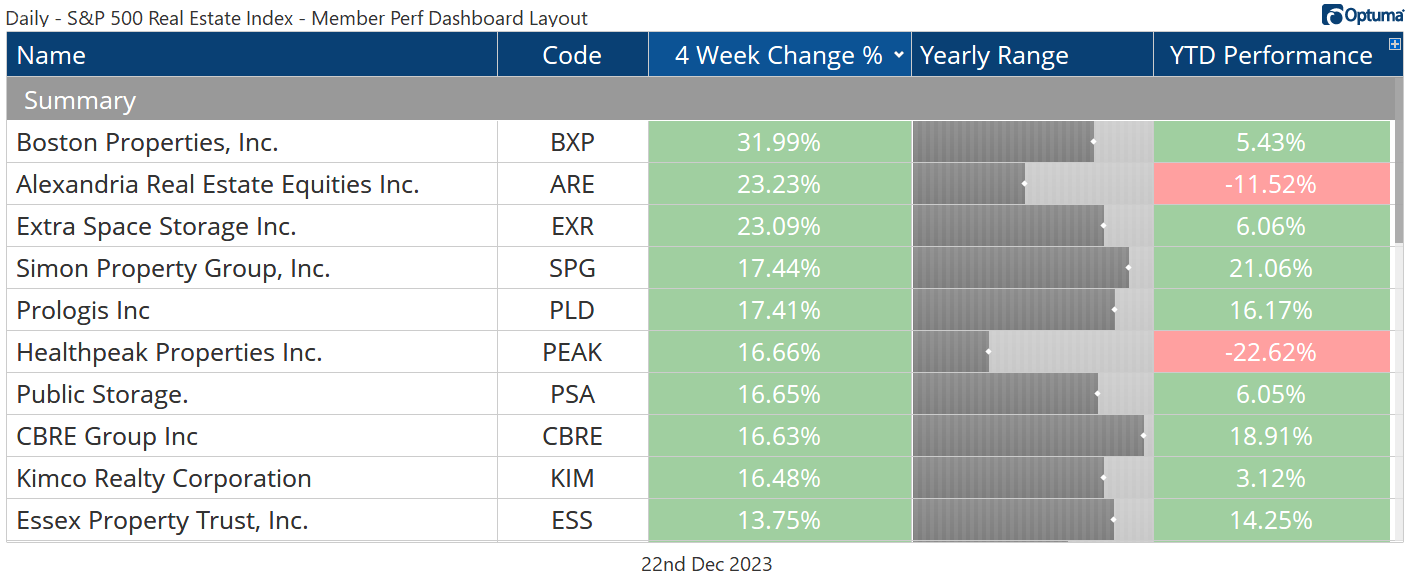

Leaders

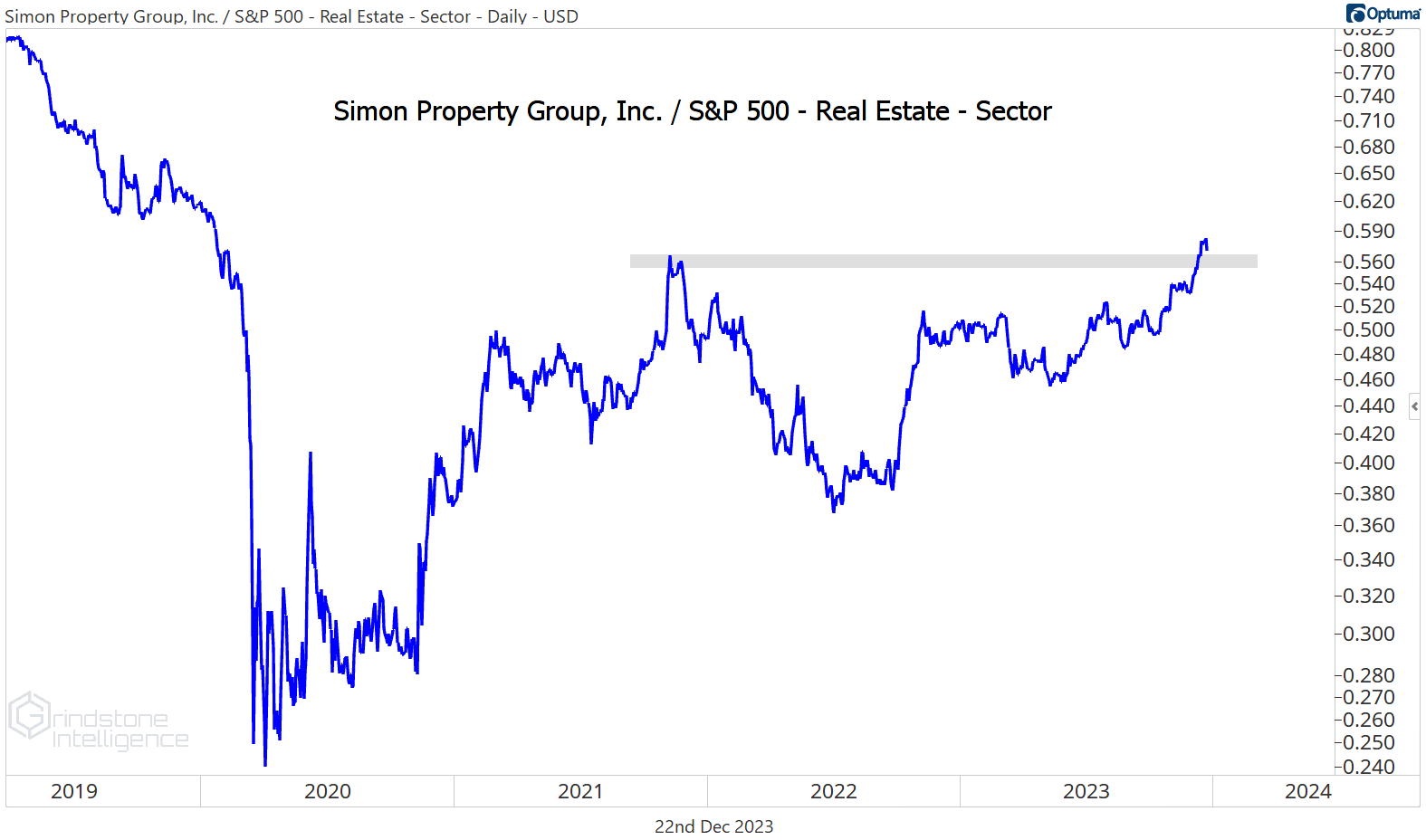

Simon Property Group was one of the top-performing stocks in the sector over the last 4 weeks, and it’s been one of the best for the year, too. The latest push helped SPG break out to multi-year highs relative to the rest of the sector.

We expect to see some consolidation here after a 40% run over the last 2 months, but as long as the stock remains above $140, we can continue betting on further upside. With our risk so clearly defined, we want to target the former highs at $170. On a break below $140, we can be looking to buy again if it gets close to the 38.2% retracement from the 2022 selloff, which is at $123.

CBRE is also breaking out relative to the rest of the sector. This multi-year consolidation looks a lot like the one we saw from 2018-2021, and we don’t want to miss out on another big breakout like we saw back then.

Our risk is really well defined for this one, too. We only want to be long above $87, with a target of $122.

Losers

The only Real Estate stock that’s been down over the last 4 weeks is Digital Realty Trust, and it happens to be one of our favorites. Relative strength is the reason. Even while the sector overall has lagged the S&P 500 over the last year, DLR outperformed. This looks like a routine backtest of the summer breakout level for the DLR/SPX ratio, and we like the stock as long as the level holds.

For the stock itself, the price is $130, which is the 50% retracement from the entire 2022 decline. We can own it above $130 with a near-term target of $142 and a longer-term target back at the former highs near $175.

One more to watch

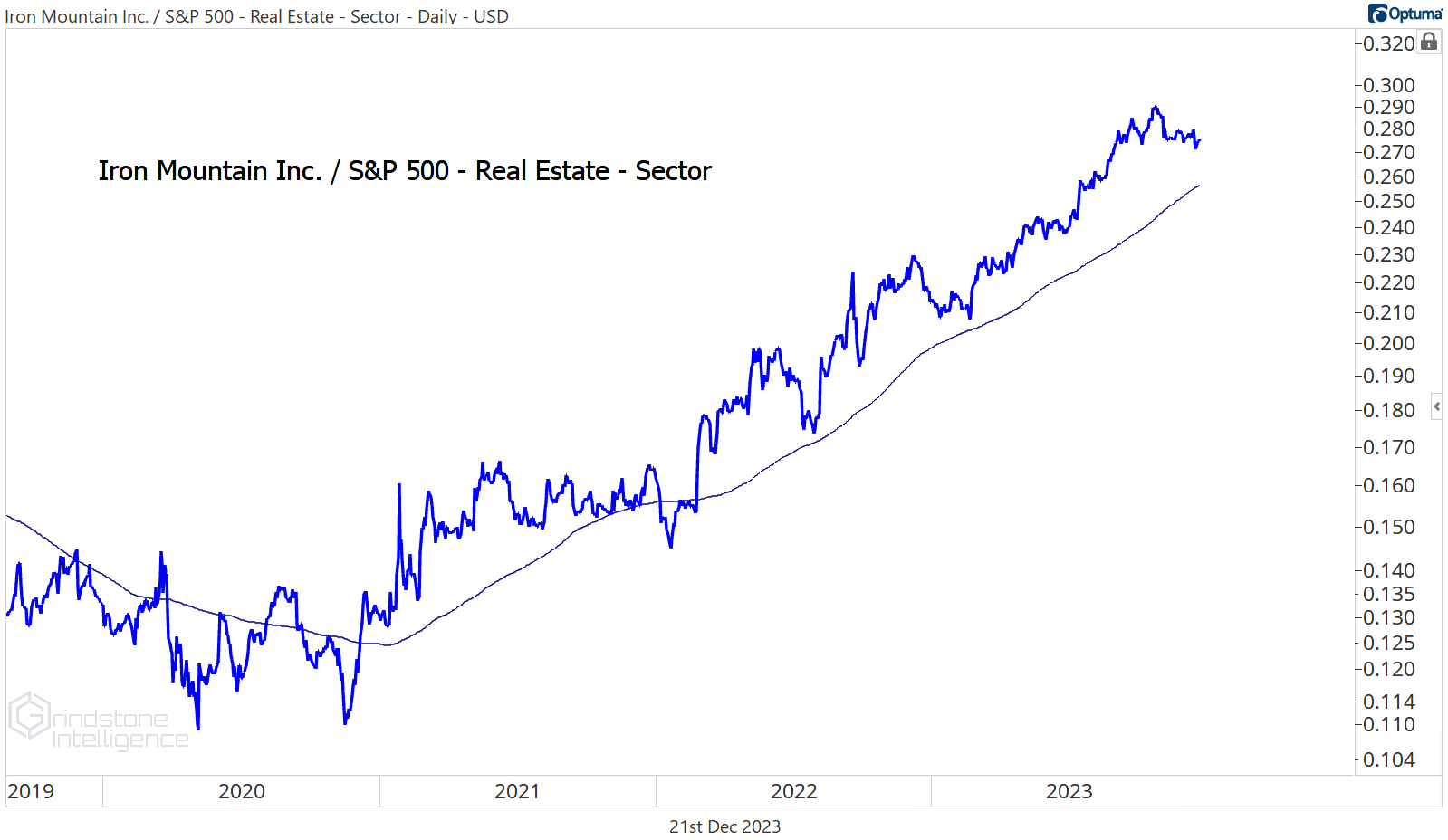

No Real Estate stock has shown more relative strength than Iron Mountain. It’s not just that IRM is the sector’s best performer on the year. Check out the uptrend when you compare IRM to the rest of Real Estate. You won’t find a smoother uptrend over the last 3 years. No matter what’s happening with interest rates or the rest of the market, IRM outperforms.

It’s also outperforming the S&P 500. Yesterday, it touched 6-year highs relative to the index. There’s nothing bearish about that.

The risk-reward setup here isn’t ideal for new entries, but we’ve been targeting $76 since the end of May. We see no reason to change that now.

That’s all for today. Until next time.