Rotation, Rotation, Rotation

If you’ve paid even the slightest bit of attention this year, you know that returns in 2023 have been all about large cap tech. It seems you can’t turn on the TV or read a single email without some mention of AI or the like.

Perhaps it’s time for a change. The power dynamics are shifting beneath the surface.

Small caps are poised to fall back into favor, at least according to momentum. Below we’ve got the Russell 2000 versus the S&P 100. Check out how the RSI has continued to improve, even as the ratio continued to fall.

Momentum divergences don’t mean anything, though. Not without confirmation. Even in the chart above, momentum has been improving since April! There needs to be a catalyst. And what better place for buyers to step in than the 2020 lows?

Before we get too excited about the small caps, we have to assess how they’re trading on their own merits. In that regard, there’s not much to see. The Russell 2000 is rangebound, and it has been for more than a year.

The Russell 2000 was actually the first of the major indexes to bottom during last year’s bear market, but it’s been notably absent during the rally of 2023 – especially since the March banking scare. So even though the group is showing signs of a potential bottom on a relative basis, it’s not because price action has improved. At least not yet.

Instead, small cap relative strength has more to do with the relative weakness we’re starting to see in large cap growth. Below we have the Russell 1000 Growth Index compared to the Russell 1000 Value Index. Growth has undoubtedly been in the driver’s seat since year-end.

Over the last several weeks, though, momentum has weakened considerably. As the Growth/Value ratio set new 52-week highs in June, RSI came nowhere close to the highs set in May. In fact, RSI never even reached overbought levels. That bearish momentum divergence stands in contrast to the bullish divergence that signaled a big reversal 6 months ago.

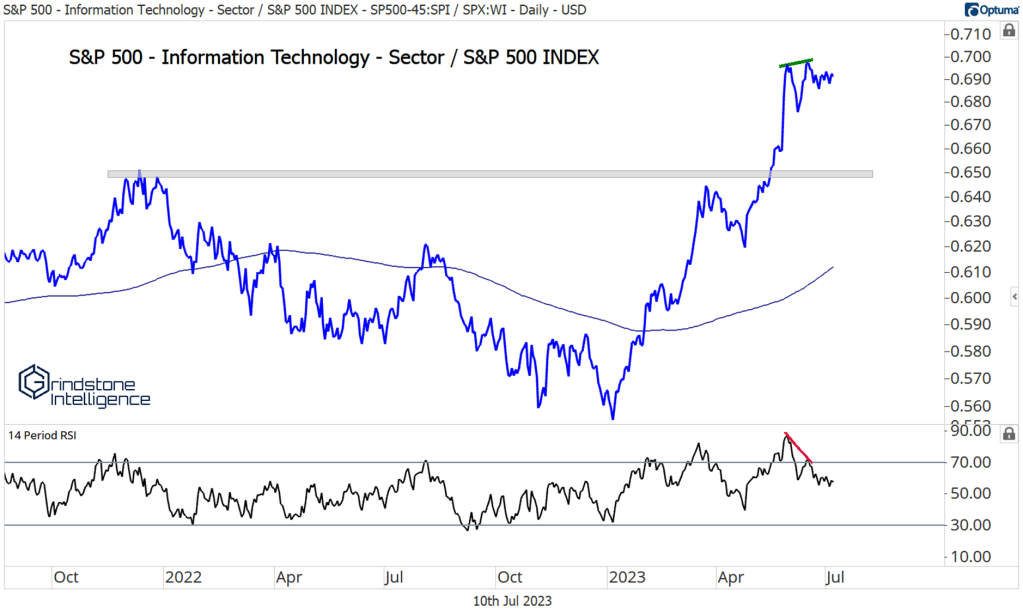

We’ve got the same dynamic when we look at the Tech sector. Momentum put in a bearish divergence at the most recent high. Structurally, Tech is still in a long-term relative uptrend, but that doesn’t preclude the group from going back to test the breakout level. Remember, those highs from 18 months ago were also the dotcom bubble highs, so there’s plenty of memory there.

Relative weakness out of Tech and other growth sectors doesn’t necessarily mean that stocks overall are headed lower. It could just mean that other sectors start to outperform during this advance – something we call rotation. And rotation is a healthy thing for the market.

Of course, if there are big losses in big tech, it’ll be hard for the indexes to keep rising. The 8 largest issues – all of them tech-oriented – in the S&P 500 comprise 27% of the index.

Fortunately, we aren’t required to just own the indexes. We can find the sectors and stocks that are poised to outperform (like small caps). Another candidate is Energy, which was the top sector in both 2021 and 2022 before falling out of favor in 2023. Contrary to the negative momentum divergences we’re seeing in growth and Information Technology, we’ve got a positive divergence shaping up in the Energy sector, and it’s happening at a key rotational level.

Once again, we’re not looking at Energy on a stand-alone basis, but instead in comparison to the benchmark S&P 500. Back in early 2020 when the global economy shut down and oil prices collapsed, Energy stocks broke to new relative lows and accelerated lower. Two years later, in 2022, that breakdown point acted as resistance for several months. And a few months after that resistance level was surpassed, the same area acted as support on a backtest. It would make a lot of sense for the Energy to start showing relative strength here once again, in respect of this level.

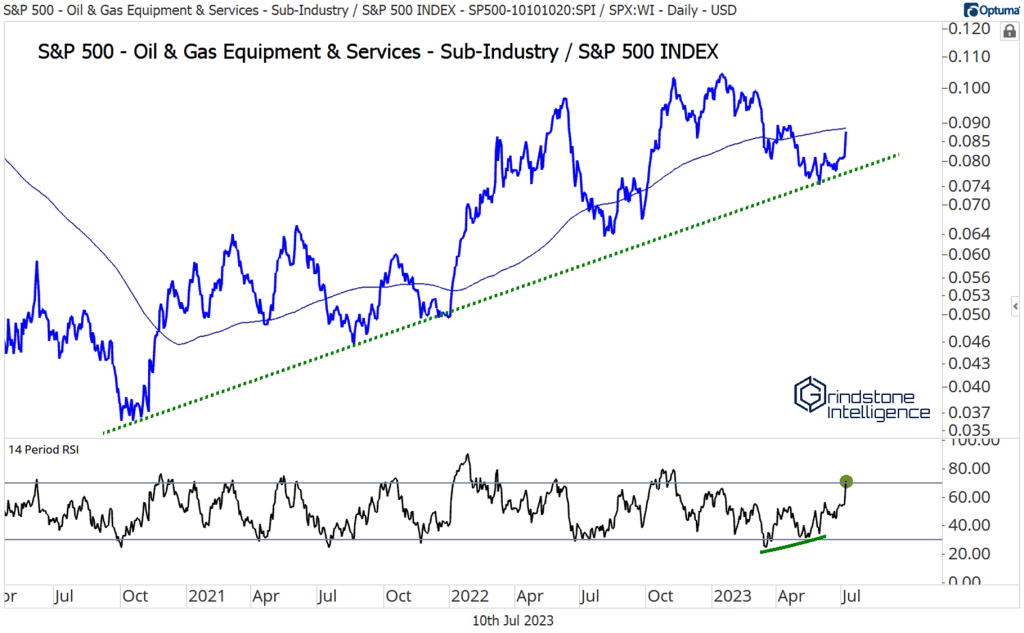

And who better to lead than the stocks that have shown the most relative strength? The Oil & Gas Equipment & Services sub-industry established a bullish momentum divergence of its own over the past few months.

More than that, though, the group ended last week in overbought territory. Only 2 of the 111 other S&P 500 sub-industries managed to do so. Perhaps the weakness in Energy has run its course.

The post Rotation, Rotation, Rotation first appeared on Grindstone Intelligence.