Sector Deep Dive - 12/20/2023

Top charts and trade ideas from the Materials sector

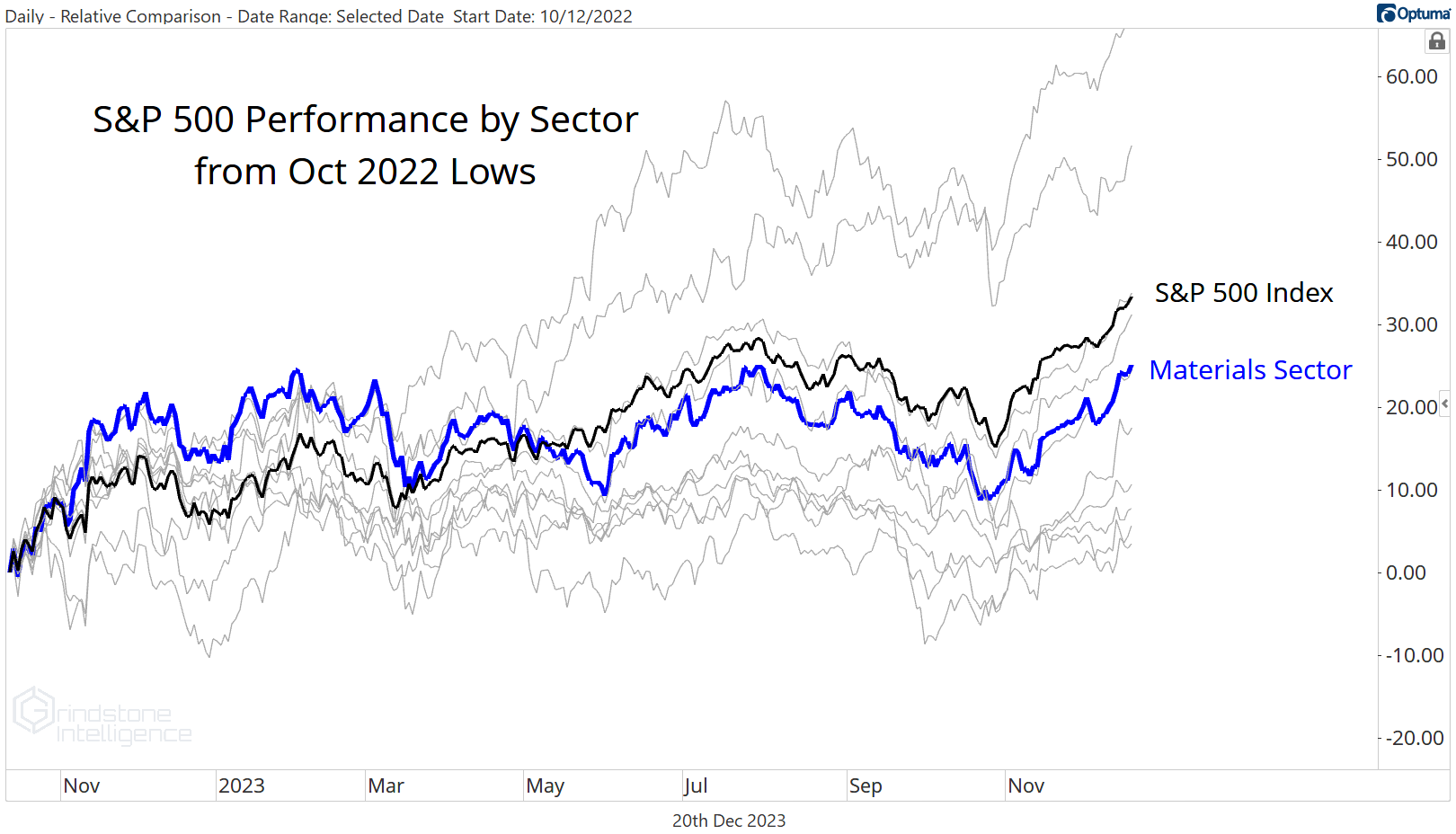

The S&P 500 Materials sector was the best place to be in the first few months following last October’s bear market bottom, but it’s been nearly a year since the sector has done anything at all. Since the end of January, the sector has climbed just 1%, while the S&P 500 has risen 17% over the same period.

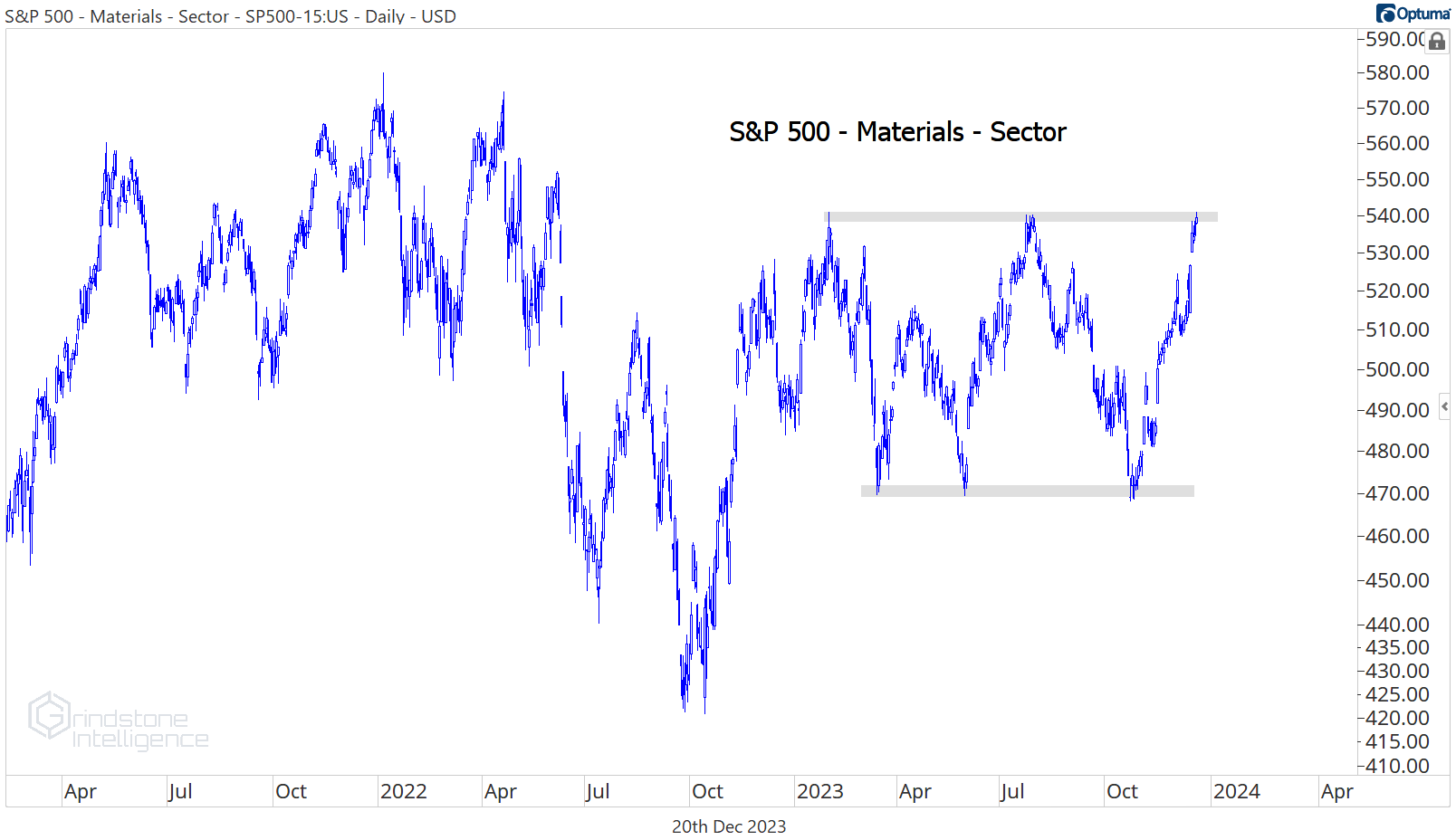

Yesterday, the Materials barely set new 52-week closing highs, but there’s still plenty of work to do before the group challenges the peaks from February 2022.

There are still 6 trading days left in the year to complete the breakout, but new highs in January 2024 will be harder to come by. January is historically among the worst months of the year for the sector, with negative price action more than half of the time over the last 30 years.

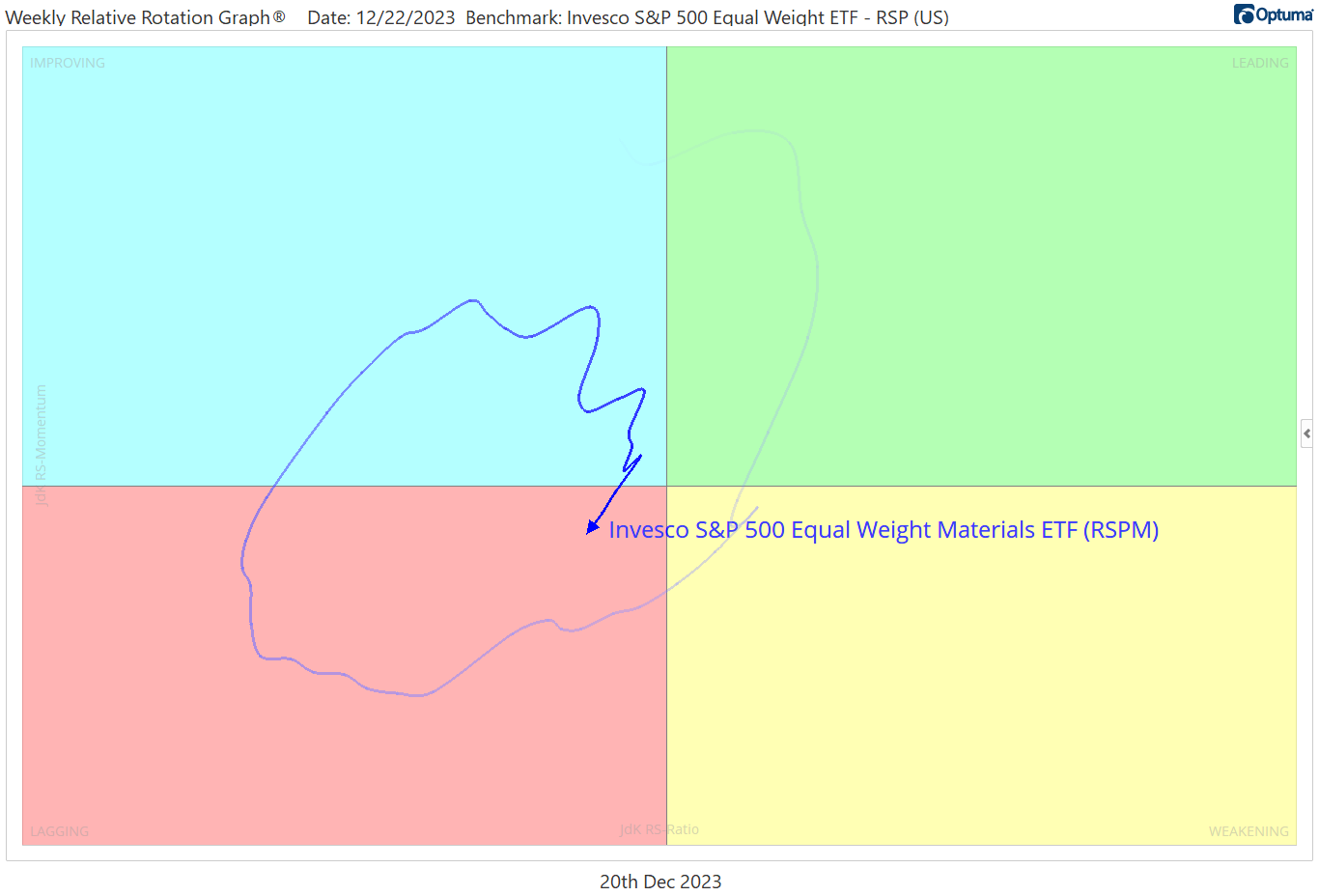

Beneath the surface, things aren’t much more compelling. The equally weighted Materials sector is in the lagging quadrant of the weekly Relative Rotation Graph, and it hasn’t graced the leading quadrant in nearly a year.

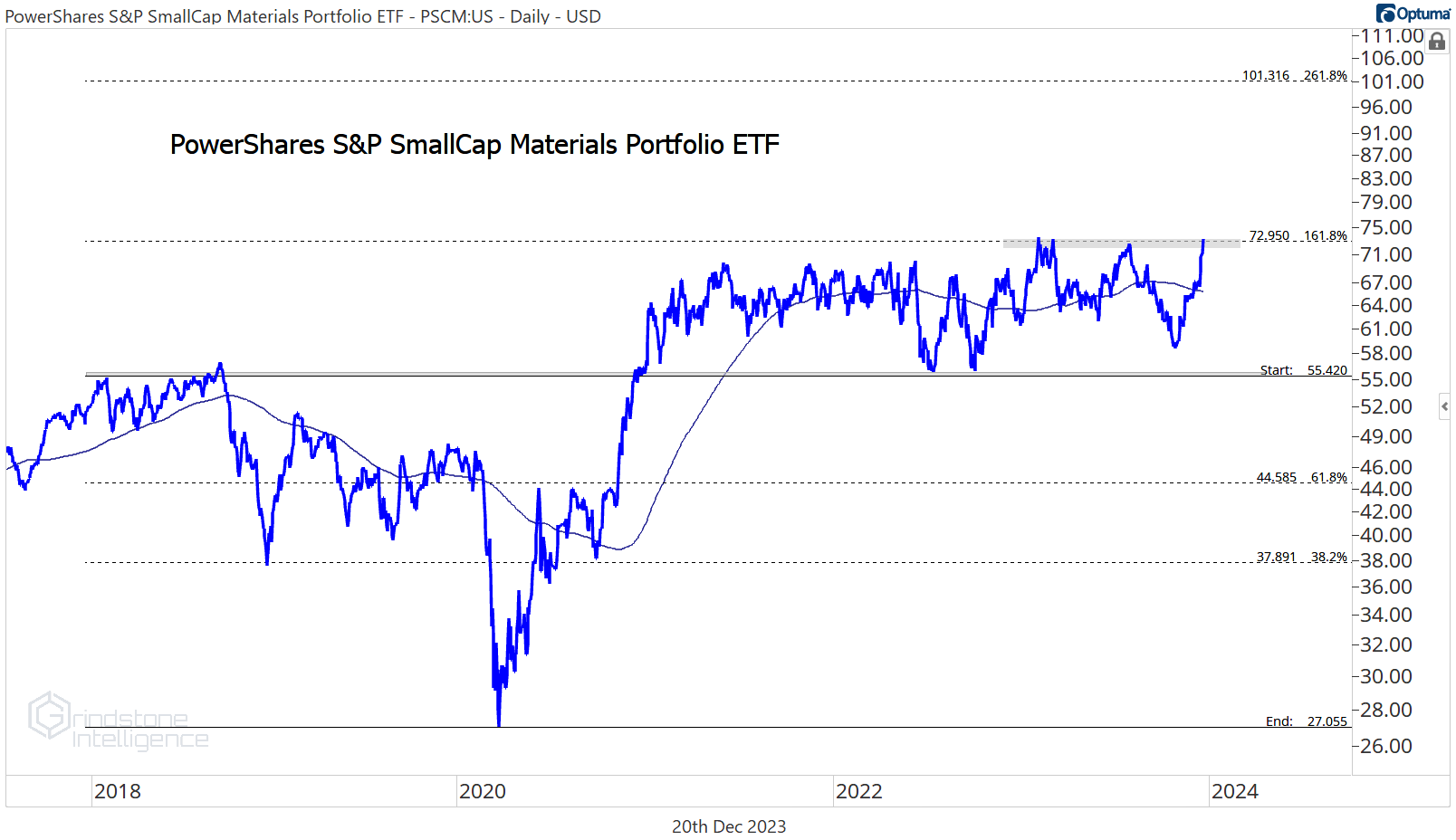

Before you completely ignore the Materials, though, check out the small caps. They’re painting quite a different picture as they attempt to set not just new 52-week highs, but new all-time highs. If PSCM is above $73, which is the 161.8% retracement from the 2018-2020 decline, we definitely don’t want to be betting against it. We’d rather be long with a target of $100, which is the next key Fibonacci retracement level.

And when we look at the small cap space as a whole, the Materials are threatening to step into the leading quadrant of the RRG. In other words, the small cap materials aren’t just rising, they’re also showing relative strength.

Why such a difference between the large cap and the small cap sector? It’s all about composition. Nearly 70% of the S&P 500 Materials sector is comprised by the Chemicals industry, and just 16% by Metals & mining. The small caps? They’re nearly 40% Metals & Mining stocks. And the Metals & Mining stocks are the ones leading the sector higher these days. Check out XME, which has jumped 20% since mid-November and is at its highest level since April 2022.

So if we’re looking for stocks to buy in the Materials space, that’s where we want to focus most of our attention.

Digging Deeper

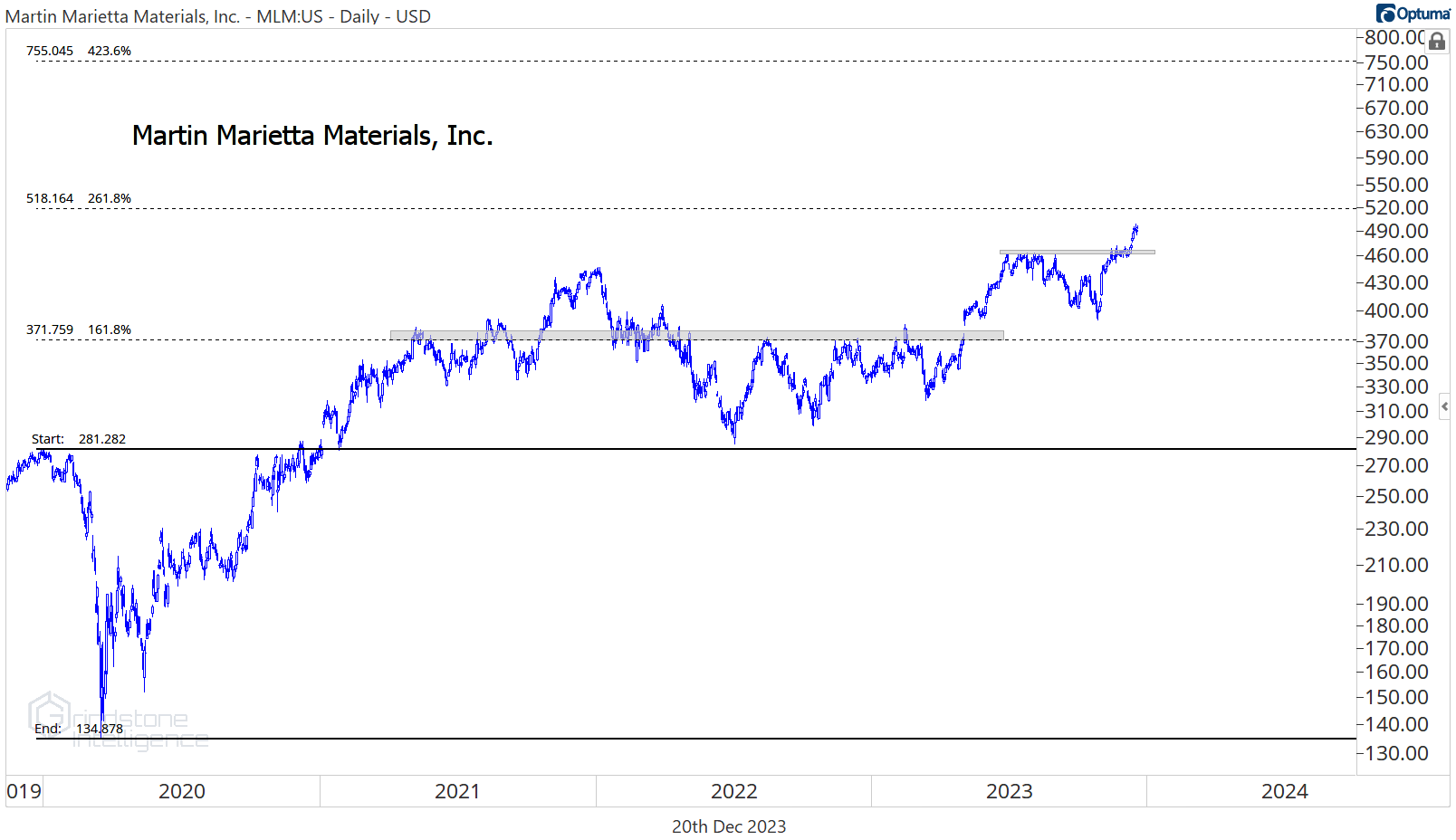

The Metals & Mining industry may be driving the latest stage of the rally, but the Construction Materials space has been the belle of the ball in 2023. Our favorite has been Martin Marietta, which is nearing our $520 target.

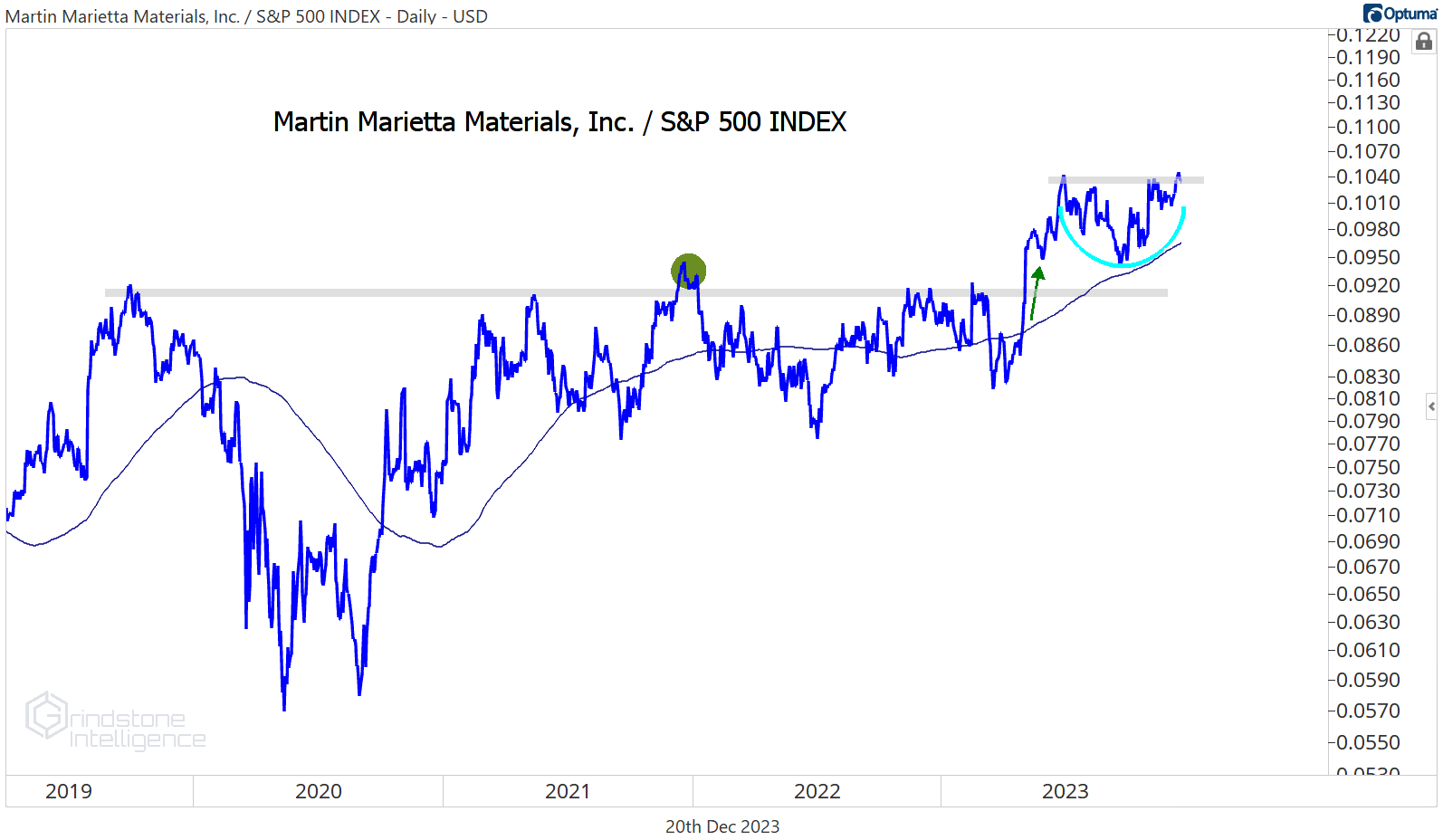

What we love most about MLM is the relative strength it’s showing vs. the rest of the market. After nearly 4 years of going nowhere against the S&P 500, MLM broke out to new relative highs in May. And now after 5 months of consolidation, it’s ready to start the next leg higher. Longer-term, we think the stock can go to $755.

Leaders

There is no shortage of stocks with big gains over the past 4 weeks. FMC is one former loser that’s worth keeping an eye on. It’s the sector’s single-worst performing stock in 2023, and it just put in a big failed breakdown below the 2020 lows. This is a great mean reversion play that in this bull market could go all the way back to the breakdown level near $85. More tactically-minded players can target $76.

International Paper is another stock working on a big reversal. It finally broke the downtrend line from the 2021 highs, and we think a move to $41 makes sense.

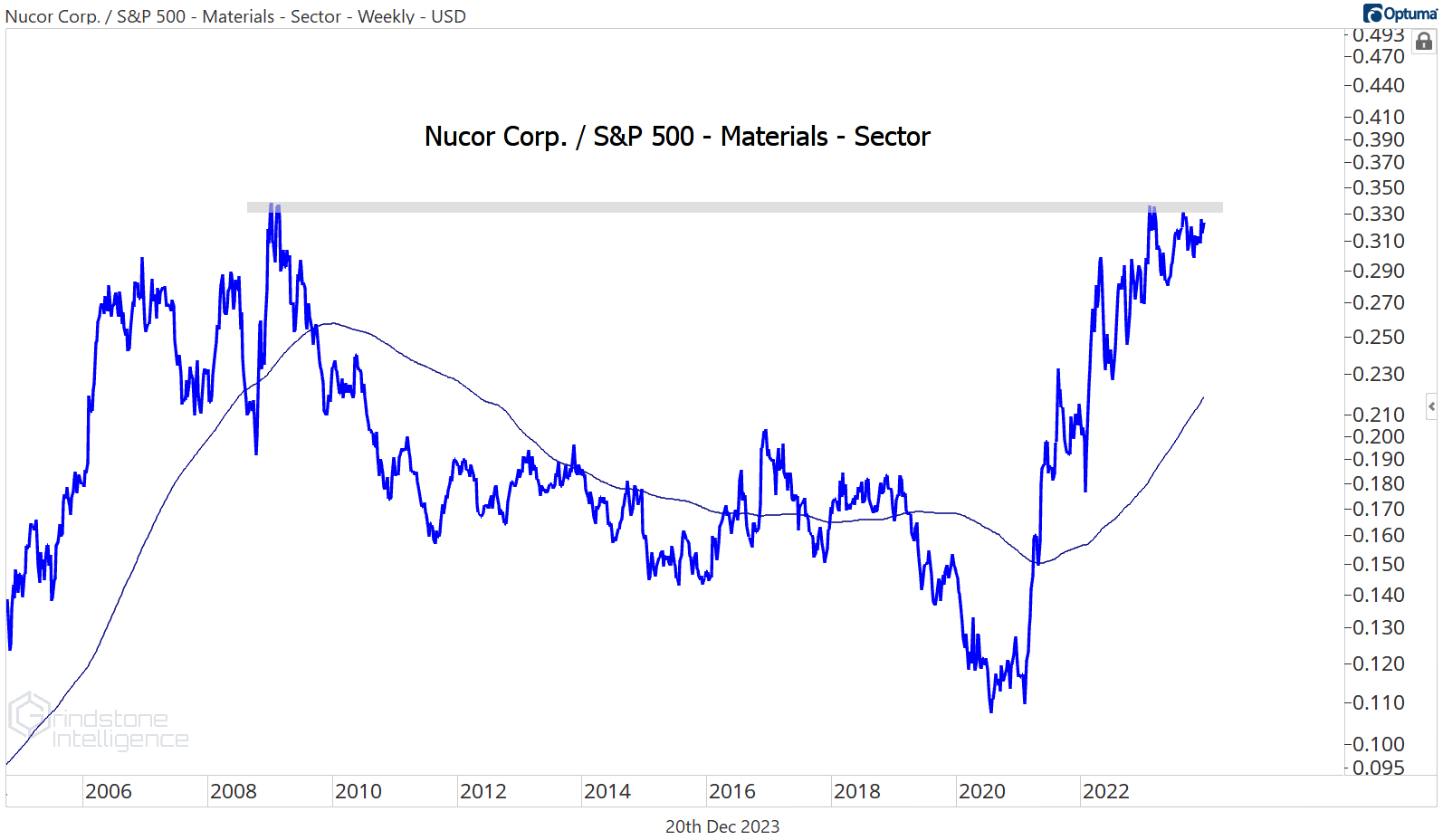

Jumping back to the metals space, Nucor just broke out of a big base. As long as NUE is above $175, we want to be long with a target of $220.

For confirmation, we’d like to see NUE get above the 2008 highs relative to the rest of the Materials sector. The stock has been digesting that 15-year resistance level for the last 9 months, and the breakout once it absorbs all that overhead supply could be massive. After all, it’s gone nowhere for 15 years.

Steel Dynamics is just as strong. We want to buy pullbacks in STLD toward $115 with a target above $150.

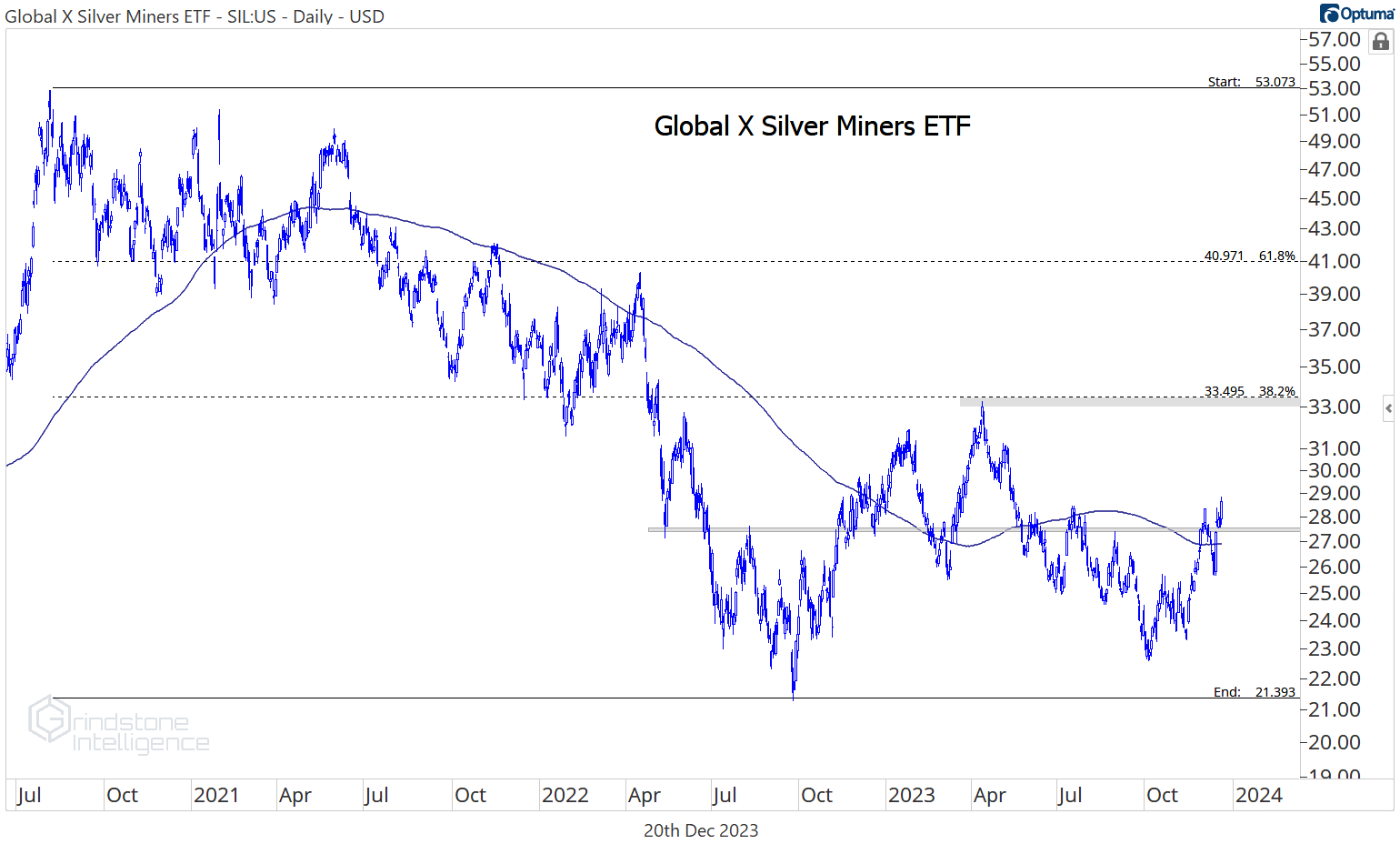

Don’t forget about the precious metals miners either, NEM has gained 11.6% over the past month, cutting its YTD losses in half. We like the setup in SIL, the Global X Silver Miners ETF. We want to own it above $27.50 with a near-term target of $33.

Losers

Linde is among the biggest losers over the last 4 weeks, but only because the rest of the sector was been off to the races. LIN was up 0.04%, bringing YTD gain for the sector’s largest constituent to 26.34%

We still think LIN heads to our target of $470, which is the 423.6% retracement from the COVID selloff, but this isn’t a great place for new entries.

The setup in Ecolab isn’t great either, but we want to take advantage of any pullbacks towards our risk level of $185, with a target back at the former highs near $230.

We could also use a breakout relative to the S&P 500 as a trigger. Check out ECL/SPX working on a 2-year inverse head and shoulders reversal pattern:

We need to be wary of this consolidation resolving in the direction of the long-term trend (which is still down), but a break above the neckline would give us confidence that ECL completes the reversal and becomes a leader over the next year.

One More to Watch

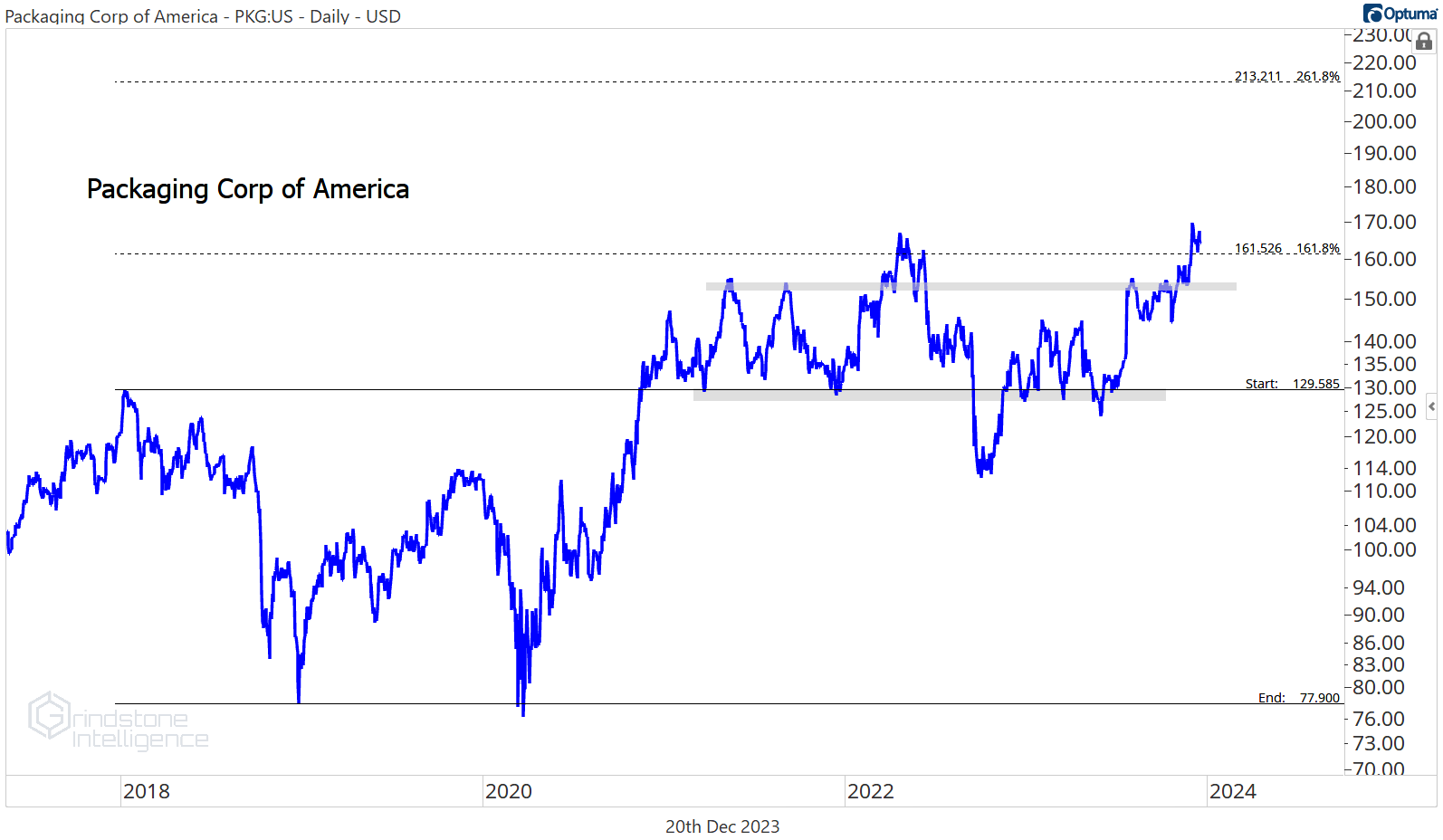

We like the setup here in Packaging Corp. We want to be long PKG above $160 - and only above $160 - with a target of $210, which is the 261.8% retracement from the 2018 decline. That’s about 30% higher from here.

That’s all for today. Until next time.