September Technical Market Outlook

At the outset of every month, we take a top-down look at the US equity markets and ask ourselves: Do we want to own more stocks or less? Should we be erring toward buying or selling?

That question sets the stage for everything else we’re doing. If our big picture view says that stocks are trending higher, we’re going to be focusing our attention on favorable setups in the sectors that are most apt to lead us higher. We won’t waste time looking for short ideas – those are less likely to work when markets are trending higher. We still monitor the risks and conditions that would invalidate our thesis, but in clear uptrends, the market is innocent until proven guilty. One or two bearish signals can’t keep us on the sidelines.

Similarly, when stocks are trending down, we aren’t looking to buy every upside breakout we see. We can look for those short opportunities instead, or look for setups in other asset classes.

We’ve been decidedly bullish on stocks since May, when the S&P 500 broke out above a key resistance level near 4150. With prices setting higher highs, higher lows, and above a rising long-term moving average, how could we not be?

That’s still the case today – equity prices are undeniably in an uptrend. That means we shouldn’t be spending time trying to find stocks to short. Rather we should be asking ourselves how bullish we should be? How aggressively should we be looking for stocks to buy?

At the outset of August, we pointed to the return of a few familiar foes and advised that caution was warranted – especially since major stock indexes were near logical areas of resistance.

Not much has changed today.

The US Dollar was indeed headwind over the past month, just like it was in 2022. In fact, Dollar strength has been associated with weakness in equities for the past 3 years. Look how strong the negative correlation between the DXY and the SPX has been over that period.

And on Friday, the Dollar put the finishing touches on its 7th(!) straight week of gains. Since the turn of the century, only the 12-week rise in 2014 was longer.

Stock trends improved over the back half of August, however, despite the continued DXY strength. We have a reversal in interest rates to thank.

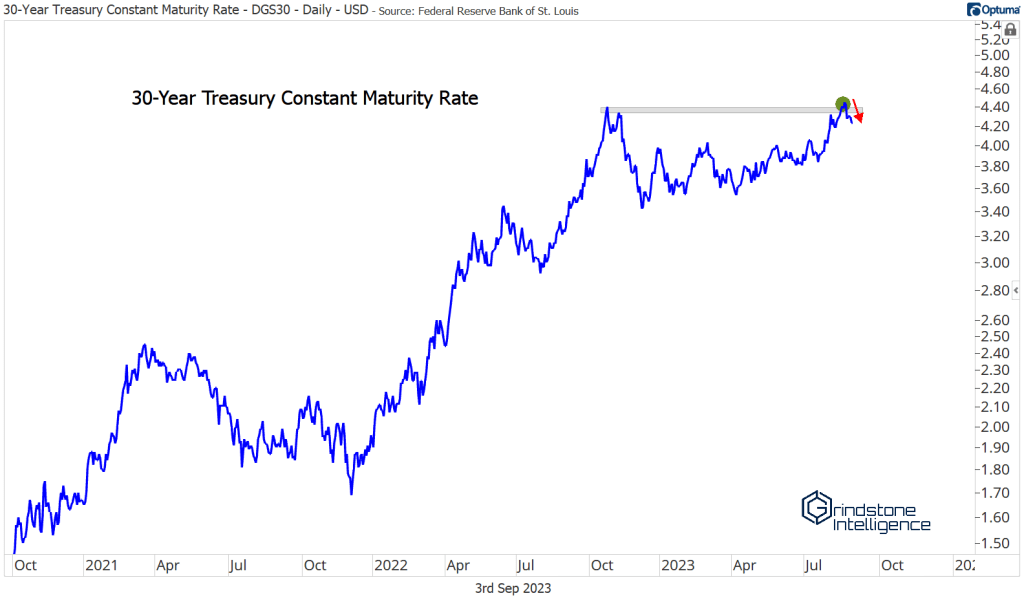

Like the Dollar, rates were a major headwind for stocks last year. When rates rose, equity prices fell. And, again like the Dollar, rates stopped rising about the same time as the S&P 500 bottomed.

For a brief moment last month, it looked as though long-term yields were set to begin a new uptrend when they pushed through last year’s peak levels. It wasn’t hard to imagine 30-year Treasurys rising to 5% or more after 10 months of consolidation. But then rates reversed course.

From failed moves tend to come fast moves in the opposite direction, and sometimes they result in full-fledged trend changes. The prospect for a new bull market in bonds put growth stocks back in rally mode to end the month.

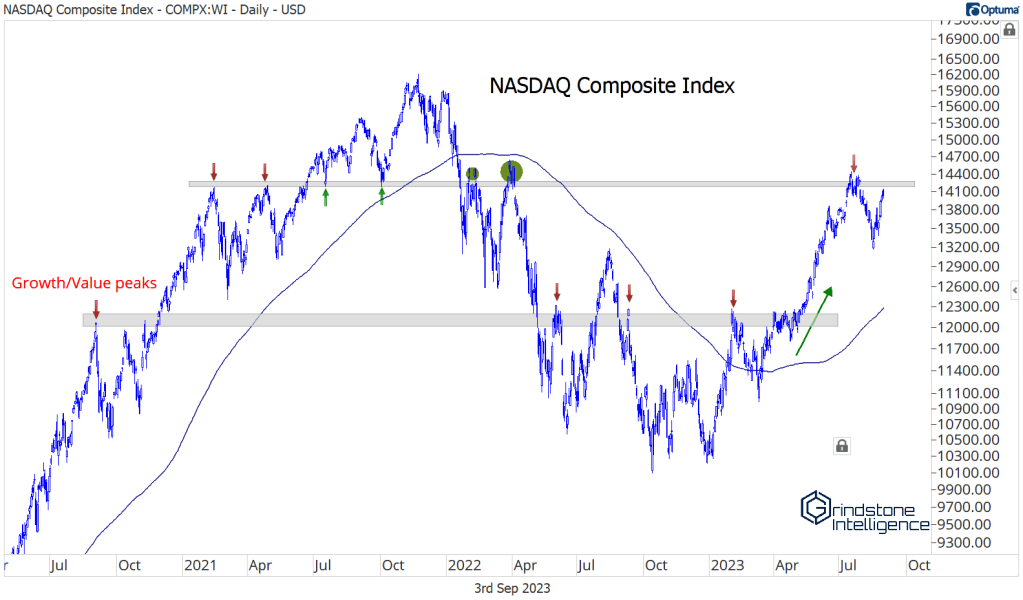

Check out the NASDAQ, this year’s big winner, coming back to challenge this key level of former resistance. The area near 14200 was an important rotational level throughout 2021 and 2022, acting first as resistance, then support, then resistance again.

The more times a level is tested, the more likely it is to break.

And value stocks are holding up well, too. We can’t be bearish stocks when the Dow Jones Transportation Average is consolidating above former resistance. It was value-oriented areas of the market that led indexes off their lows last October, and despite their underperformance in 2023, they’re still the ones showing structural relative strength.

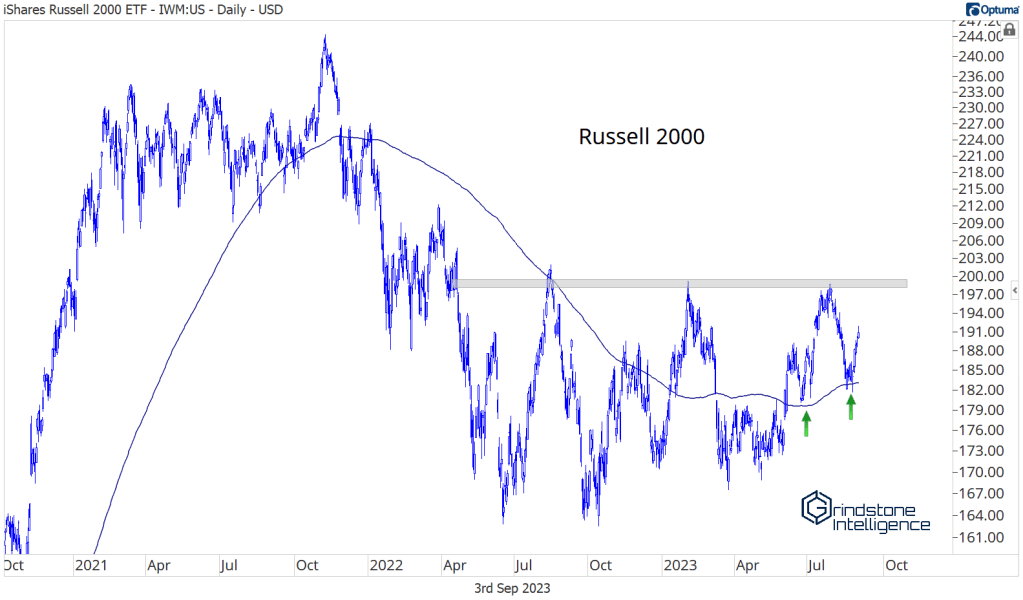

Even the weakest areas of the market have managed to hold up. Small caps haven’t made any progress since last summer’s peak, but they just bounced off their 200-day for the second time since June and have been setting higher lows for most of the year.

If this was a time to be bearish and betting on lower stock prices, we’d expect to see leaders failing and laggards breaking to new lows. We’re just not seeing that.

Instead, we’re seeing further evidence of risk appetite.

Consider the ratio of the Consumer Discretionary sector to Consumer Staples.

Earnings trajectories for Discretionary companies are tied to economic strength, and Staples less so – you’re probably not getting a new sports car during a recession, but you’re still going to the grocery store and buying toothpaste. When the economic outlook is uncertain, investors tend to favor those companies that offer stability.

If Consumer Staples stocks outperform, it’s a sign that investors are cautious. When Discretionary stocks lead, investors are adding risk to capitalize on faster expected growth. We’re seeing the latter right now.

Stocks are in uptrends and investors are favoring risk-on over risk-off areas of the market. This definitely isn’t a market we want to be shorting.

That said, stocks are still battling significant resistance. The NASDAQ Composite we looked at earlier is still below 14200. The Russell 2000 is stuck below the summer highs. And the S&P 500 hasn’t gotten past a key rotational level of its own.

In September 2021, the index was rejected at 4500. That same spot was support a few months later, then acted as resistance again in early 2022. The level has some historical significance, too. It’s the 423.6% Fibonacci retracement from the entire 2007-2009 decline. Notice how much the market has respected these levels over the last 10 years? The next leg of this young bull market can’t begin until we’ve absorbed all the overhead supply from this major resistance zone.

Will it happen soon? Maybe. But September tends to be a rough month for stocks. Over the last 70 years, September is the only month where negative returns have outnumbered positive ones.

There’s nothing magical about seasonality. Stocks don’t have to follow historical patterns. But a big bet on surging prices in September is a bet where the odds aren’t stacked in our favor. We continue to favor a cautiously bullish approach toward stocks – at least until the indexes can string together some bullish resolutions.

What would have us turning more bearish on risk assets? A big upside resolution from the US Dollar Index would certainly get our attention. For now, we believe a rangebound USD between 101 and 105 is consistent with a structural bull market for stocks. But a full-scale trend reversal – sparked by July’s failed breakdown and confirmed by a move above 105 – would force us to reevaluate that opinion.

That type of move would most likely accompany a reacceleration in interest rates, too. With the Fed nearing the end of its tightening cycle and inflation well on its way back to 2%, a big move higher in rates would catch a lot of people off guard. Are growth stocks and their premium valuations really prepared for a move to 5% in the risk-free rate? We doubt it.

That kind of move isn’t our base expectation by any means – but that doesn’t mean we can rule it out.

We write about some of our favorite stocks and share other investment ideas each week with Members and Subscribers. Here are links to our most recent sector and asset class reports.

(Premium) Communication Services Sector Deep Dive

(Premium) Consumer Discretionary Sector Deep Dive

Top Charts from the Tech Sector

(Premium) FICC in Focus – August

(Premium) Financials Sector Deep Dive – August

(Premium) Materials Sector Deep Dive – August

Top Charts from the Energy Sector

(Premium) Industrials Sector Deep Dive – August

(Premium) Utilities Sector Deep Dive – August

(Premium) Health Care Sector Deep Dive – August

Top Charts from the Real Estate Sector

(Premium) Consumer Staples Sector Deep Dive – August

The post September Technical Market Outlook first appeared on Grindstone Intelligence.