Taking Stock of the US Labor Market

If you asked people on the street to describe the state of the economy, there’s a good chance they’d start by talking about the labor market. For most people, jobs and wages are the key economic indicators to watch. Right now, financial markets seem to agree.

At the end of August, the Federal Reserve Bank of Kansas City hosted its annual economic symposium in Jackson Hole, Wyoming. The closely watched event featured an 8-minute speech from Fed Chairman Jerome Powell, where he reiterated his commitment to bringing inflation back down to the Fed’s 2% target – even if that meant economic pain.

For many, economic pain means job losses. Traditionally, labor market tightness has been associated with higher inflation. The relationship is logical – a mismatch between supply and demand for workers leads to higher wages, which increases demand for goods, which leads to higher prices and the need for more goods, which increases the demand for workers, and so on and so forth. Despite the logical relationship, though, the correlation between labor and inflation had weakened in the years prior to the pandemic. But inflation has returned, and monetary policy makers are embracing the so-called Philips Curve once again. Powell seems set on tightening policy until the jobs market slows, in hopes demand weakens enough to cool inflation.

The Jackson Hole speech put a spotlight on the labor market – just in time for a slew of data the following week. On Wednesday morning, we got our first look at ADP’s reconfigured jobs report. ADP’s records showed the economy added 132,000 jobs in August, indicating a slowing pace of hiring when compared to July. Annual pay, though, was still up 7.6%, with pay for job-changers up a whopping 16.1%.

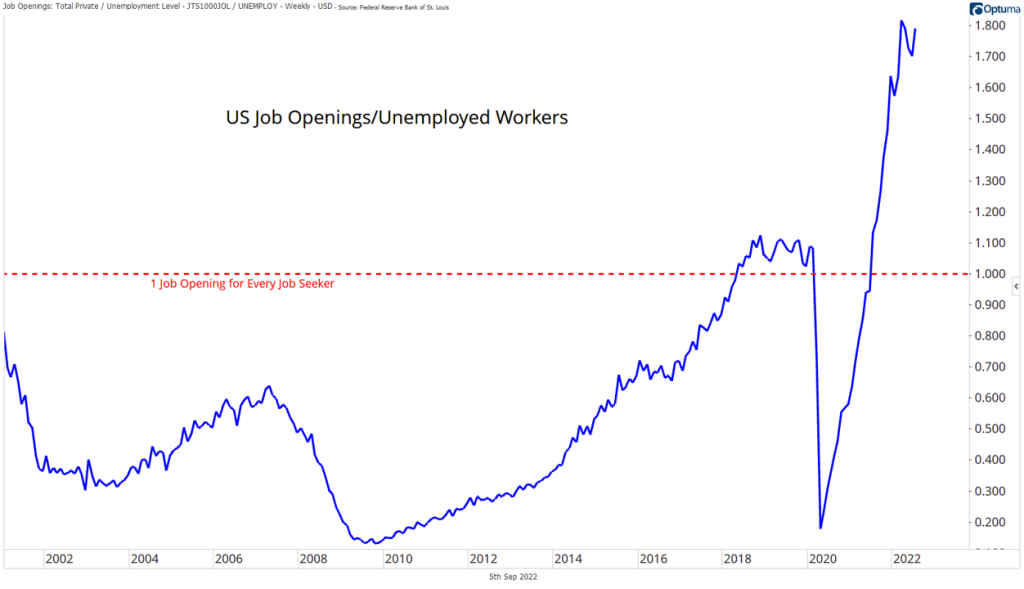

Later that morning, we received an update on the number of job openings available. This data set isn’t the most timely – we just received July numbers – but it is the basis for my favorite labor market chart: the ratio of job openings to jobless. Right now, there are close to 2 jobs available for every unemployed person. If that sounds extreme, it’s because it is. Powell probably didn’t see the softening he was looking for here, and financial markets weren’t pleased. Stocks fell and interest rates climbed following the release.

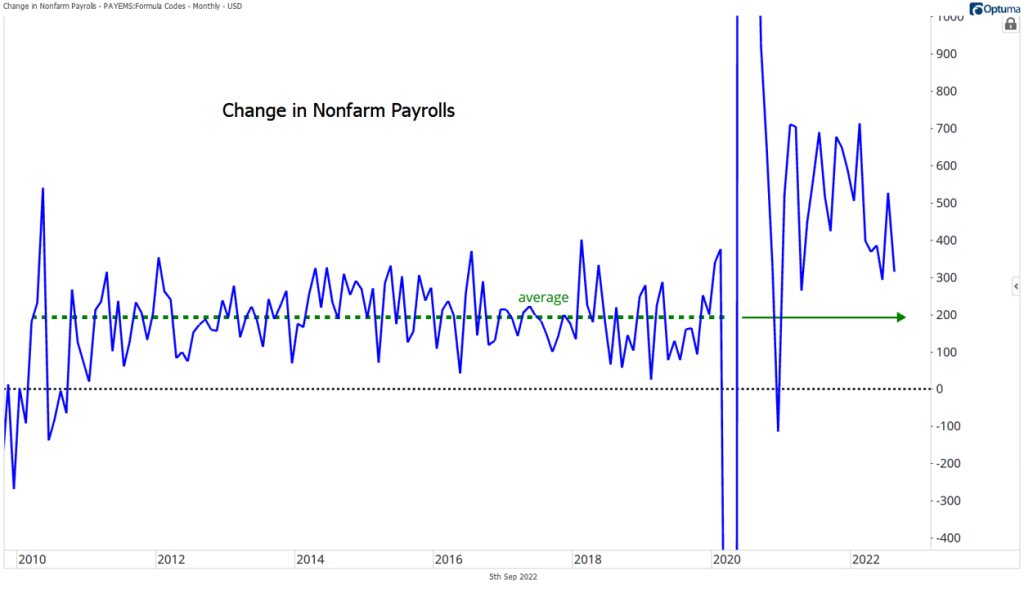

Powell didn’t find what he was looking for in Friday’s nonfarm payrolls number, either. Stocks and bonds tumbled further The BLS said the economy added 315,000 more jobs in August, one of the lowest numbers since the end of the pandemic, but still well above the average seen in the decade prior to COVID, and quite a bit stronger than the number estimated by ADP earlier in the week.

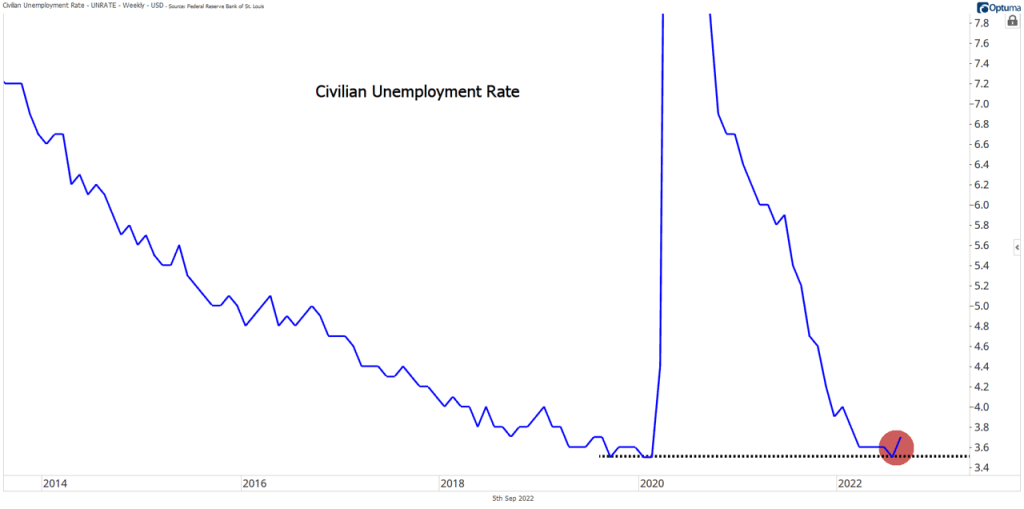

Despite the strong headline number, though, the U-3 unemployment rate actually moved up 0.2% in August. July’s 3.5% unemployment rate had matched the multi-decade, pre-pandemic lows.

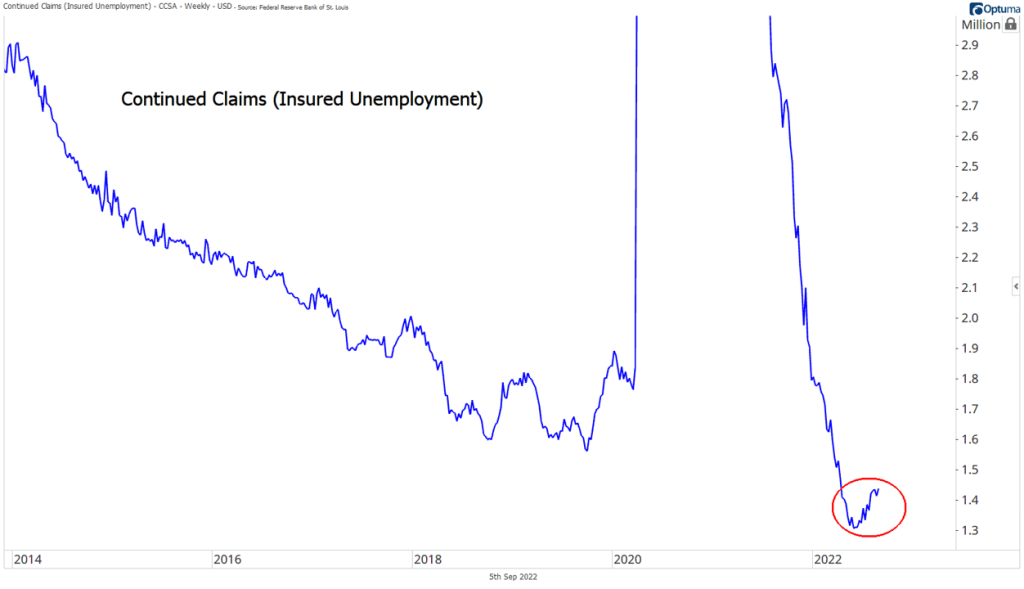

In some ways, the rising unemployment rate has been foreshadowed by a rise in weekly unemployment claims. Continuing claims, reported every Thursday morning, have been rising since May. Despite week-to-week volatility, this data set is one of the better economic leading indicators – when it rises for 6 months or more, recessions usually follow.

Still, a rising unemployment rate doesn’t seem to fit with an economy that just added more than 300,000 jobs. Unless, of course, you consider another variable from the BLS report.

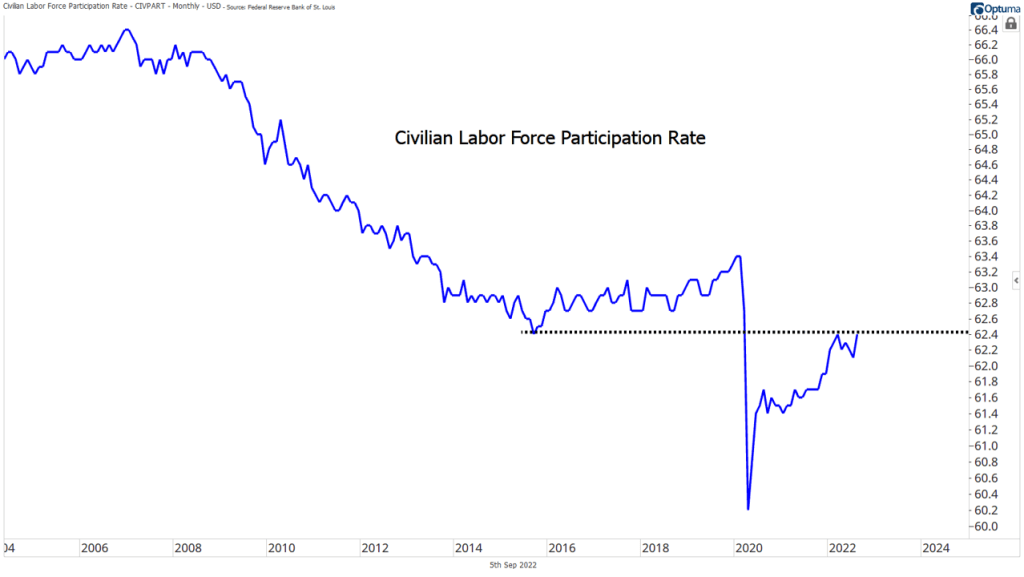

Labor force participation rose from 62.1% to 62.4%. More workers entered the jobs market, increasing the number of unemployed in the calculation of the U-3 rate. Participation now matches the high of the current economic cycle and the low of the last one, but there’s still a gaping hole when compared to the pre-pandemic level of 62.4%.

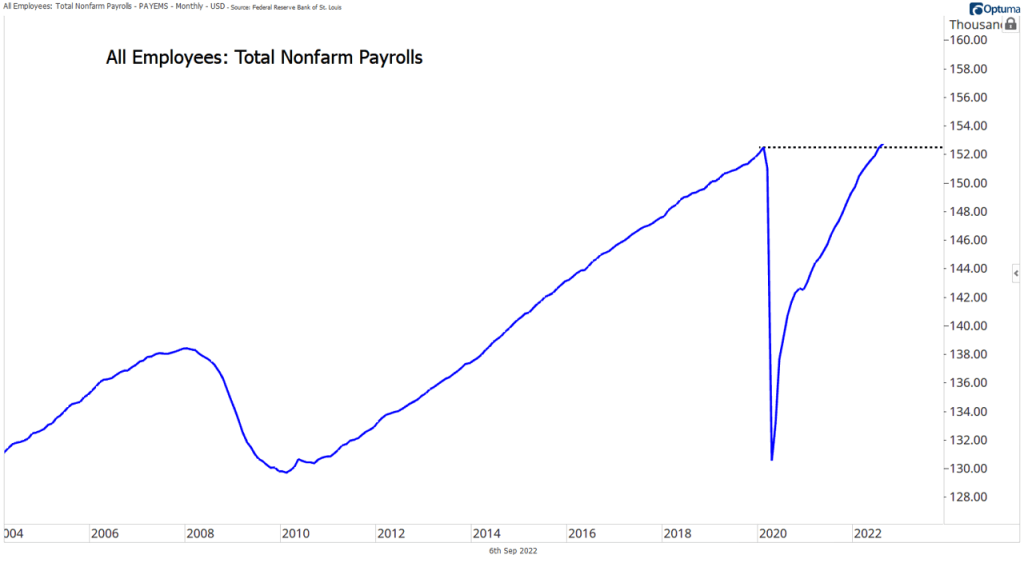

You can see it clearly in the total employment numbers. Total nonfarm payrolls are just now topping the February 2020 highs, and they’re well below the pre-pandemic trend. In short, there are still millions of people on the sidelines.

And that adds to Powell’s dilemma. He acknowledged at Jackson Hole that supply issues are at least partly to blame for the current inflationary environment, and many of those can’t be solved: China’s continued COVID lockdowns, Russian and Iranian oil embargos, European energy shortages, etc. The Fed instead must focus on things it can control, like demand. That’s the surest way to bring supply and demand into balance.

But how much would supply chains improve if all those who’ve left the labor force were to return? Some older workers took advantage of pandemic stimulus to retire early, some people can’t find affordable childcare, and some people are still afraid of the coronavirus. Would continued demand for labor and higher wages pull them back into the workforce? From 2015 to early 2020, the labor force participation rate rose from 62.4% to 63.4%, largely in thanks to the tightest labor market we’d seen in nearly 50 years. Could that happen again?

It’s likely we’ll never know the answer. With inflation at 8.5%, Powell can’t afford to wait and see.

Nothing in this post or on this site is intended as a recommendation or an offer to buy or sell securities. Posts on Means to a Trend are meant for informational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in posts. Please see my Disclosure page for more information.

The post Taking Stock of the US Labor Market first appeared on Grindstone Intelligence.