The 10 Charts to Watch in 2023

It’s a new year, so there’s no better time to take a step back and think about what will drive markets in the months ahead.

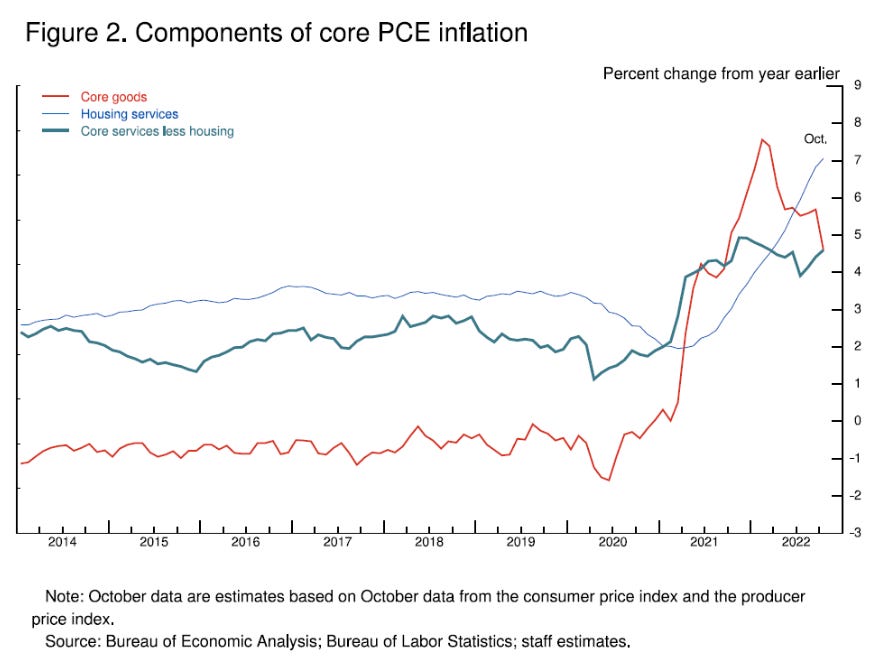

The Components of Inflation

At his November 30, 2022 speech, Federal Reserve Chair Jerome Powell described the 3 primary components of inflation – Core Goods, Housing Services, and Core Services less housing. Core goods drove the first wave of this inflationary cycle, as surging demand for tangible products during the pandemic came face-to-face with sagging production and supply chain disruptions. The next wave was led by a spike in the cost of housing.

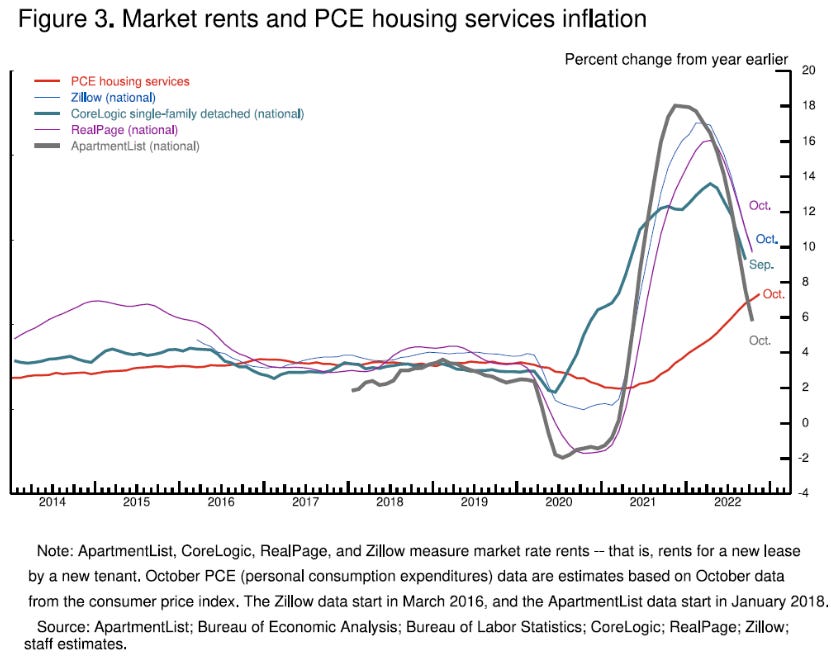

Core goods inflation peaked in early 2022, and housing will likely peak around the middle of this year (see Figure 3 below). The Fed will look past what it sees as ‘transitory’ declines in core goods and housing inflation, and instead focus on the price of core services. These charts are from his presentation:

The Tightening Cycle

Powell and Co. claim they’ll do whatever it takes to cool inflation, even if it pushes the US economy into recession. It’ll take higher interest rates for longer, according to their models.

Wall Street doesn’t seem to believe them. While the median dot from the FOMC’s December Summary of Economic Projections implies a year-end 2023 rate of more than 5%, Fed Funds Futures are pricing in a rate not much higher than where we are now.

Labor Market Showing Signs of Weakness

The primary goal of the Fed’s interest rate hikes is to put a stop to excess inflation. To do that, they need to loosen an extremely tight labor market and dampen demand.

If you look at the unemployment rate alone, you won’t see much change, but beneath the surface, tightening monetary policy is having an effect. Weekly continuing jobless claims, while still near the lowest levels of the last 50 years, have jumped by 400,000 in the last 6 months. The 8 other times claims have risen this quickly, a recession has followed.

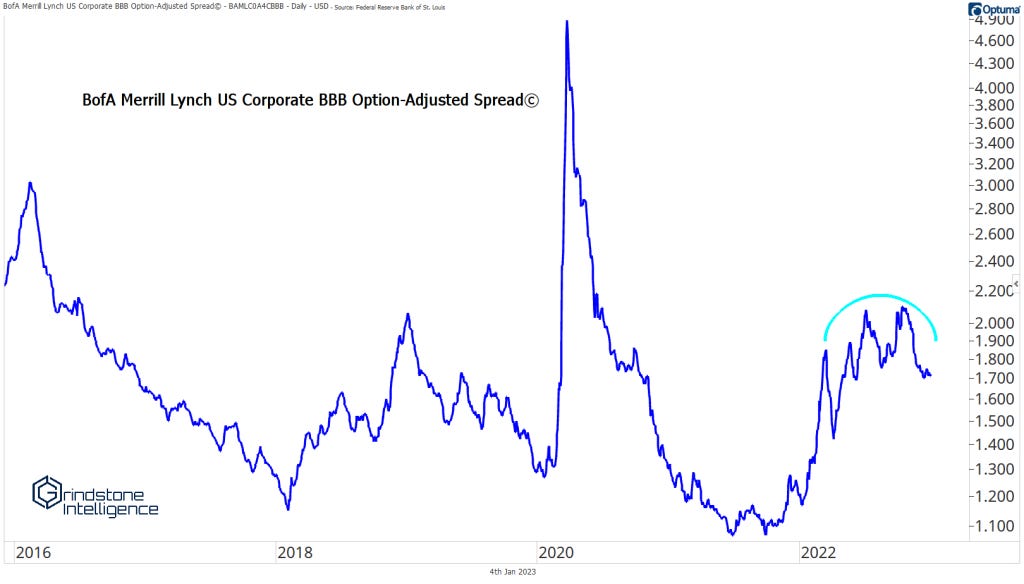

Credit Spreads

If the US economy is headed for recession, credit spreads aren’t showing it. A common feature of slowdowns in economic activity is increased default rates by both consumers and businesses. As a result, lending rates to those borrowers rise faster than the risk-free rate paid by the US government.

Credit spreads increased in the early part of 2022, but they’ve since stabilized. If negative GDP growth is ahead, this chart should give us advance warning.

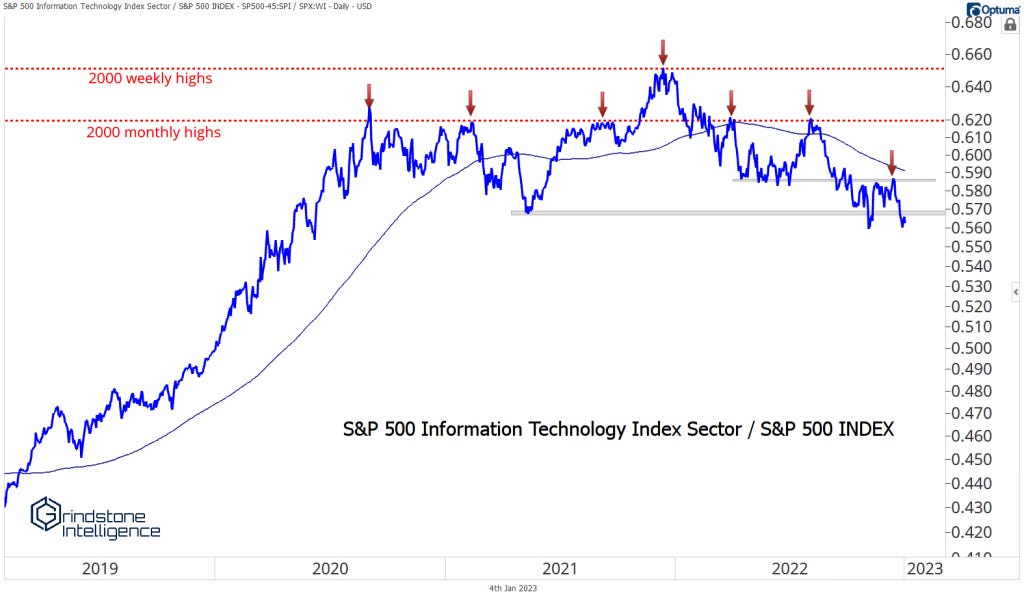

Tech Stocks’ Big Top

Growth stocks were in control for more than a decade after the financial crisis. Being a ‘Value’ investor was synonymous with underperforming. That changed in September 2020, when Information Technology ran into the relative highs it set at the peak of the internet bubble.

Lots of people will argue that technical analysis is a farce. Price moves are random, and historical moves have no bearing on the future. Even more folks will balk at the importance of prices from more than 20 years ago – let alone the ratio of two price indexes.

Does the chart below look random? Do you really think it’s just coincidence that after a decade-long bull market, Tech just happened to peak at exactly the 2000 highs – the height of the biggest Tech bull market of our lifetimes?

In any case, Tech won’t be a secular outperformer again until it absorbs all this overhead supply. In fact, the latest weakness makes it more likely that the sector will continue to underperform in 2023.

Growth vs. Value

Much like the ratio of Tech to the S&P 500, growth stocks have underperformed their value counterparts for much of the last 2 years. There hasn’t been much reason to like the prospects of growth companies, especially in the face of rising interest rates around the world.

That seems to be the consensus opinion, though, and it often pays to play devil’s advocate. Here’s one reason to think 2023 could be different: the Russell 1000 Growth index is nearing a potential level of support relative to the Russell 1000 Value index. The ratio is currently at the 38.2% Fibonacci retracement from the entire 15-year rally.

Crypto

Cryptocurrencies had a tough year in 2022, and that weakness looks set to continue.

Bitcoin is stuck in an indisputable downtrend, having broken the summer lows in November following the FTX meltdown. Former support around 19000 is now overhead supply, and the next area to watch on the downside is 13000. A rally back above 20000 could quickly change the narrative.

Precious Metals

It’s been a while since precious metals were cool. Gold and silver both outperformed handily during the onset of the pandemic in early 2020, but then they lagged in spectacular fashion over most of the next 18 months.

2022 was a year of consolidation for the two metals relative to equity markets. 2023 might be the year they become leaders.

Nothing in this post or on this site is intended as a recommendation or an offer to buy or sell securities. Posts are meant for informational and entertainment purposes only. See Terms for more information.

The post The 10 Charts to Watch in 2023 first appeared on Grindstone Intelligence.