The Bull Case for Stocks

I don’t know which direction the stock market – or any other asset class – is headed next. No one does for sure. But whether your portfolio is prepared for impending doom or positioned for equities to rocket higher, it’s always important to understand both the bull and bear cases. By understanding where the risks to your thesis are, you’re more likely to know when your thesis could be wrong. Only then can you take corrective action

With stocks on pace for one of their worst years ever, the bear argument isn’t hard to see. Trends are down in most asset classes. Inflation is running rampant, cutting into consumer savings and crushing consumer confidence. War rages in eastern Europe. China clings to a Covid-zero approach that continues to wreak havoc on global supply chains.

Central banks around the world are pushing for tighter financial conditions. Our own Federal Reserve started the year still doing quantitative easing, and their policy rate was at the zero lower bound. It’s since implemented the fastest interest rate liftoff in decades and begun reducing the size of its balance sheet at the fastest rate ever.

Earnings growth has weakened on the back of margin pressures and unrelenting Dollar strength, and economists almost unanimously forecast a recession within the next 12 months. Home sales have come to a complete stop. And let’s not forget those 2 consecutive quarters of negative GDP growth.

Like I said, it’s easy to be a bear.

So what’s the bull case? What signs should we be watching for a change in the trend?

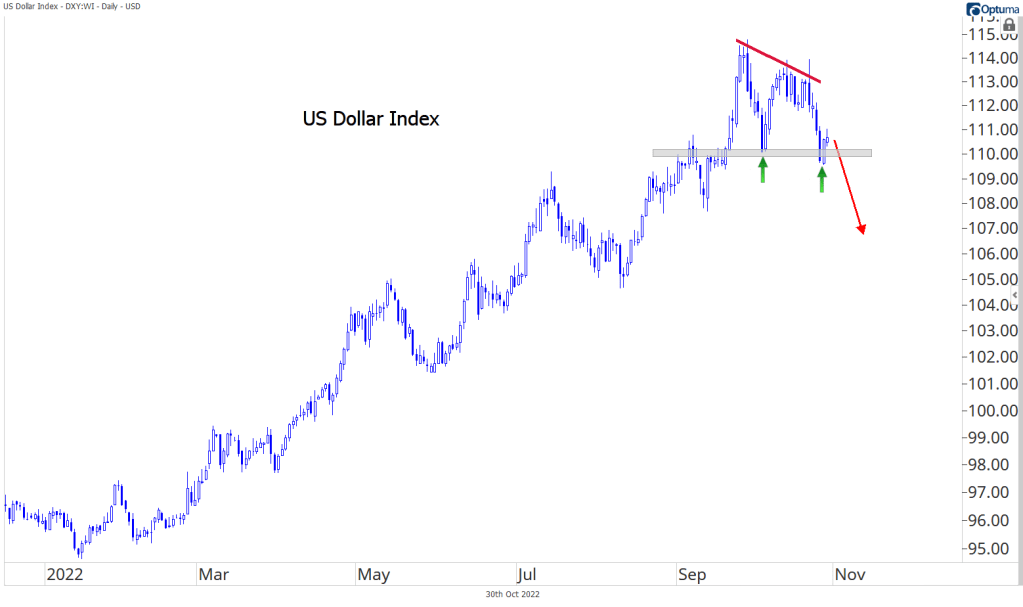

I think it starts with the Dollar and rates. If you flip a year-to-date chart of the US Dollar index on its head and lay it on top of the S&P 500, you can hardly tell the difference between the two. The correlation with yields has been nearly as strong.

Only a few times this year have one of the three diverged from the others, and each time, the majority proved right. Right now, stocks are moving higher and the Dollar is moving lower, but rates have largely failed to confirm the move.

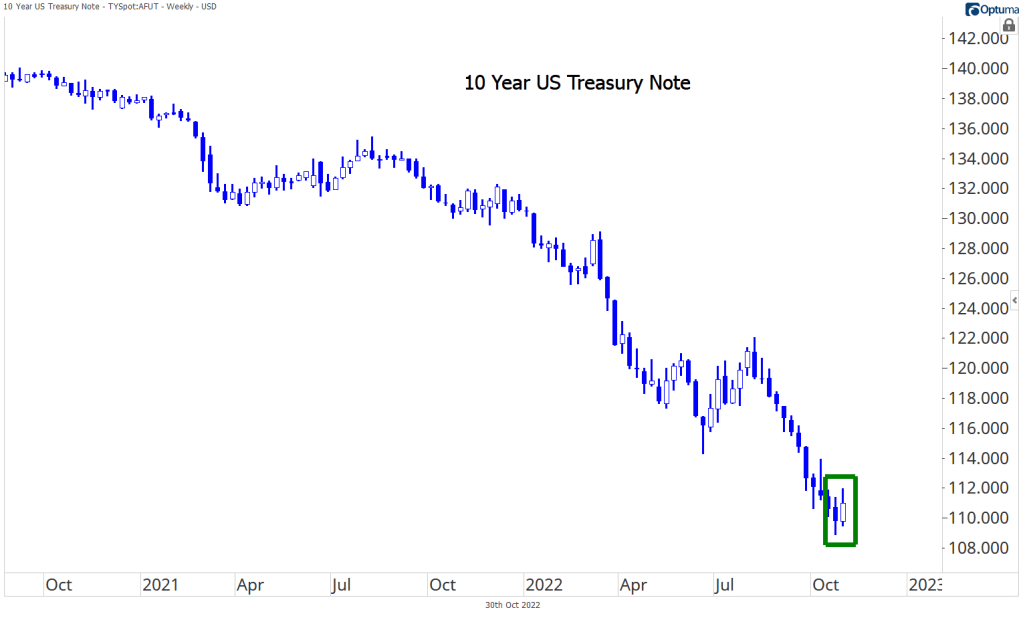

Last week’s bond rally did little to erase the prior 12(!) consecutive weeks of interest rate increases.

We’re looking for the bull case, though, right? And last week’s candle was a bullish engulfing one for 10-year Treasury notes. That could have marked a bottom for bonds that would confirm the move in stocks.

The rally will likely require further weakness in the U.S. Dollar. The USD hasn’t set a new high in over a month and is currently testing support. Failure to hold it would be a positive sign for bulls.

Equities have shown some strength in their own right.

The S&P 500 October lows didn’t quite reach the pre-Covid highs like they did for the Dow Jones Industrial Average. But the trough did occur at a pretty logical level: the September 2020 highs, which marked a major peak in Growth vs. Value. Prices have jumped 11% from their lows.

There’s been internal improvement lately, too. The S&P 500 index is back above its June lows, and so are most stocks. More than 70% of constituents are above those former lows, including 71% of Information Technology stocks and nearly every Energy company.

One group that isn’t above its June lows is Communication Services. This sector has been the worst place to be in 2022, down 38% since December. Yet even after it’s two largest companies disappointed investors last week and were punished accordingly, the sector overall closed the week above lows set earlier in the month. Moreover, daily RSI never even got close to oversold levels.

It could be that lows haven’t been broken yet, and momentum hasn’t gotten oversold yet. But the alternative hypothesis is that even the worst sector in the index has stopped going down. When that happens, the bears have lost their grip.

Here’s more evidence for the bulls: defensive areas of the market are no longer leading. The Utilities sector has been falling on a relative basis for the last month after being a leader for the first 9 months of the year. If that continues, it probably happens in a world where stock prices are rising, not falling.

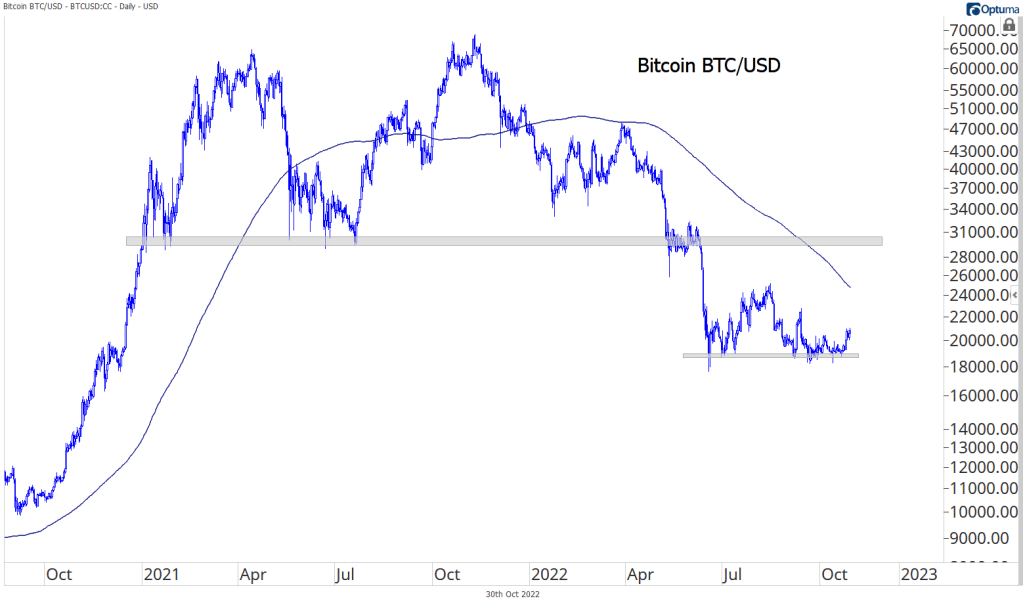

So if it’s not defensive areas of the market that are leading, who is it? Obviously, Energy stocks have been a dominant force. But there’s relative strength elsewhere, too. Small cap stocks never even broke their June lows.

And neither did Bitcoin. What does that tell you about risk appetite?

The bears are still in control of the market, and it’s not hard to understand why. We never want to lose sight of the trend and right now, that’s still down. But the night is always darkest before the dawn. Stay vigilant.

Nothing in this post or on this site is intended as a recommendation or an offer to buy or sell securities. Posts on Means to a Trend are meant for informational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in posts. Please see my Disclosure page for more information.

The post The Bull Case for Stocks first appeared on Grindstone Intelligence.