The Commodities Landscape in 10 Charts

There’s a base metal which is said to have a PhD in economics. Right now, it needs a different kind of doctor.

Copper just ended the week below its 200-day moving average for the first time all year after dropping 3.7%. Over the last 4 weeks, it’s fallen more than 9%, the largest such decline since the metal bottomed last July. The recent weakness comes despite the long-awaited and ongoing economic reopening of China, the world’s most important copper consumer.

Copper is quite sick indeed.

Partly to blame for last week’s bloodbath is the US Dollar.

The Dollar Index roared 25% higher in just 18 months following its May 2021 low, as interest rates moved up and the US economy offered a safe haven from the turmoil in Europe and the lockdowns in China. After finally peaking last fall, the Dollar quickly fell back to the top end of its 2016-2021 range, providing a tailwind to equity and commodity prices along the way.

Now, the index is trying to rally from this long-term level. Back-to-back half-point gains on Thursday and Friday drove the Dollar to its best week since peaking last September.

Copper isn’t the only base metal under pressure. Zinc, nickel, and aluminum, are all trending lower, too.

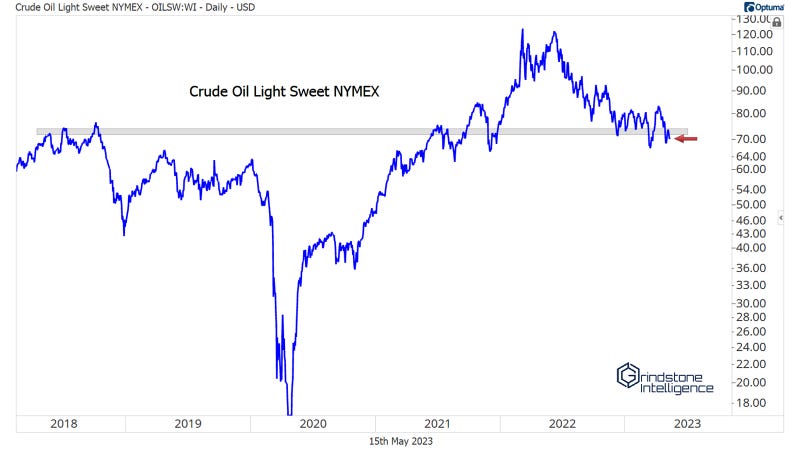

Crude oil has suffered a similar fate, despite a surprise production cut from OPEC in April. OPEC production cuts have an inconsistent track record when it comes to propping up oil prices. This time, the announcement served to push crude higher for a few weeks, but now we’re back to where we started. Their cut was in response to the risk of weakening global demand and macroeconomic uncertainty. If that pessimistic outlook proves correct, though, no amount of collusion will be able to offset the decline in consumption. Lower oil prices over the past few weeks reflect that risk.

Weakness hasn’t spread to the entire commodities space – at least not yet. DBA, a basket of agriculture commodities, is still hanging near support from last fall’s swing highs. For now, we can still classify this action as a healthy consolidation of the huge runup during 2020 and 2021.

The relative strength shown by this particular fund masks a wide dispersion in performance within the softs, though. Wheat, oats, lumber, and soybean oil all broke to new lows in recent weeks. Meanwhile, orange juice, cattle, cocoa, and rough rice are all near multi-year highs. Sugar, the largest component of DBA, has been especially strong.

We’re getting similarly mixed signals within precious metals. Gold just broke out to multi-year highs relative to copper, a bullish resolution that reinforces an uptrend in place since last spring.

On an absolute basis, gold prices are a whisper away from new all-time closing highs after spending the last 3 years digesting the 2018-2020 run-up.

The trend here is not down. On an intraday basis, the yellow metal just set new 52-week highs, and that’s not something you see in downtrends. But there can’t be an ‘all-clear’ signal with prices still just below resistance from those 2020-2022 highs.

This is the third attempt to break 2100 – why might this time be any different? For one, the more times a level is tested the more likely it is to break. Each time buyers push prices up to that level, they absorb more supply. Eventually, there’s no one left to sell.

How high could the metal go on a breakout above 2100? Perhaps above 3000. That’s the 1794% Fibonacci retracement from the 1990s decline. Prices have respected these retracement levels all the way up: The hiccups in 2006 and 2008 occurred near Fib levels, the ceiling from 2013-2019 was the 684.4% retracement, and right now, were stuck below the 1109% retracement. It would make a lot of sense to go up and touch the next one. That might even be a conservative expectation – prices rallied a lot more after the 2004 breakout.

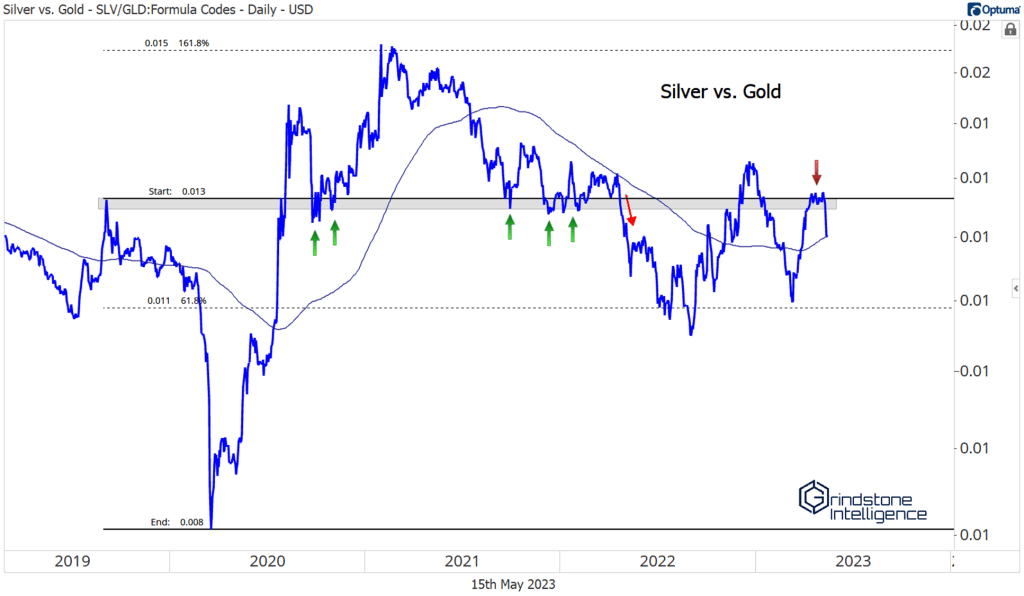

There’s only one problem: Silver.

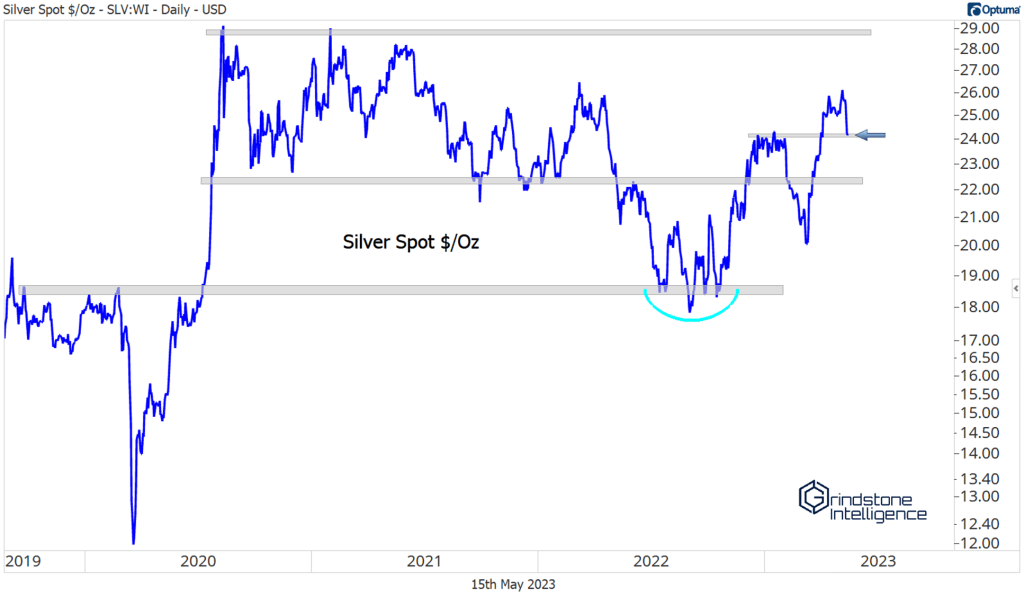

Silver and gold tend to be highly correlated, but silver tends to move in greater magnitudes. As such, when precious metals are rising, silver should outperform. Instead, silver refuses to lead. The silver/gold ratio just failed again at its 2019 highs, a level that’s marked several important reversals over the last 3 years.

The failing ratio reflects silver’s inability to avoid last week’s commodities selloff. It dropped 6.3% from near 52-week highs, the worst weekly performance since last October. Now, silver must try to find support above the December-January consolidation range.

If it can’t, it’s tough to picture gold marching to new all-time highs.

The post The Commodities Landscape in 10 Charts first appeared on Grindstone Intelligence.