The Morning Grind - 12/26/2023

Inflation continues to slow

Last Week in Review

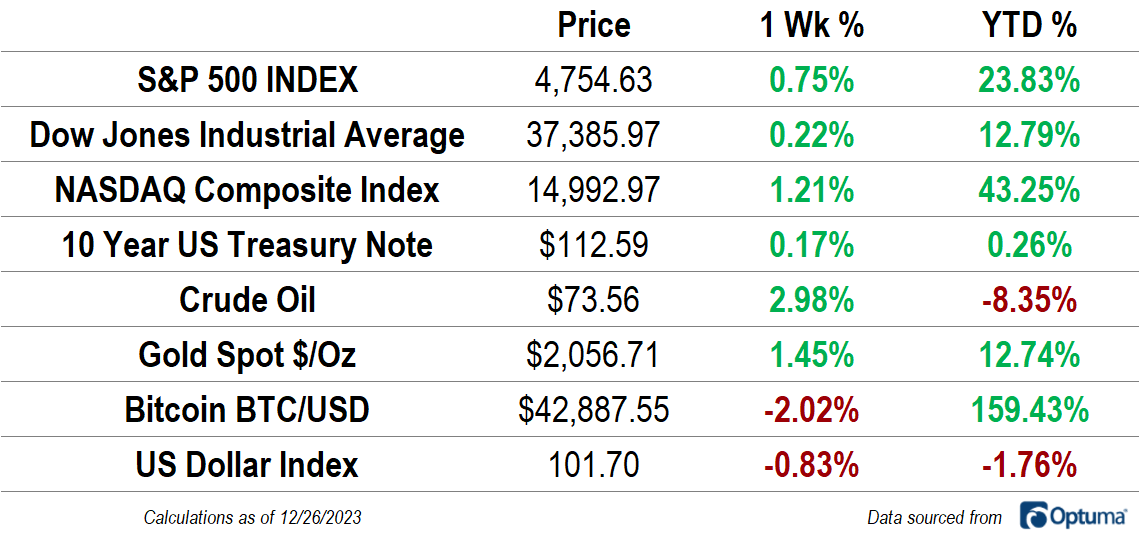

US stock prices rose for the eighth straight week, led by a 1.2% gain in the growth-oriented NASDAQ Composite. The Dow Jones Industrial Average closed at its highest level ever, and the S&P 500 ended the week just a whisker away from new highs itself. On this holiday-shortened week, the S&P 500 will try to match its longest win streak since 1985, when the index rose for 12 straight weeks.

It wasn’t just stocks on the rise. Gold notched a 1.5% gain for its second-highest close ever, and crude oil had its best week since October, rallying 3%.

Third quarter US GDP was revised down to 4.9% last week, down from a prior estimate of 5.2%. Lower consumer spending was to blame. It wasn’t all bad news, though, because price inflation continues to slow. The Fed’s preferred measure of inflation, the Personal Consumption Expenditures Deflator, fell to 2.6% in November, the lowest level since spring 2021. Core PCE, which Fed officials believe is a better indicator for the rate of underlying inflation, fell to multi-year lows as well. The 3-month change in Core PCE has annualized near 2% since July.

Relatively Speaking

Every single S&P 500 sector gained ground over the last month, paced by a 10% rally in the Real Estate sector. Industrials (+7.0%), Consumer Discretionary (6.9%), Materials (6.4%), and Financials (6.3%) all outperformed, while Utilities (0.9%) and Energy (1.0%) lagged.

Growth sectors are still in the pole position year-to-date, with Information Technology (+56.0%), Communication Services (55.0%), and Consumer Discretionary 41.6%) each on pace for banner performances. The massive gains aren't widespread, though. Investing in any other sector has yielded a return for the year that’s well below the S&P 500's 23.8% gain, and 4 sectors are on pace to finish the year in the red.

What's Ahead

Here are the key data releases and events to keep on eye on in the coming days.