The Recent Rally in Real Estate Stocks: Mean Reversion or Major Reversal? - 11/16/2023

The Recent Rally in Real Estate Stocks: Mean Reversion or Major Reversal? - 11/16/2023

The Real Estate sector has been down in the dumps for most of the last two years. From the start of 2022, when the bear market for stocks began, to today, Real Estate has fallen nearly 30%. By comparison, the next worst sector is Consumer Discretionary, down just 14% from its highs.

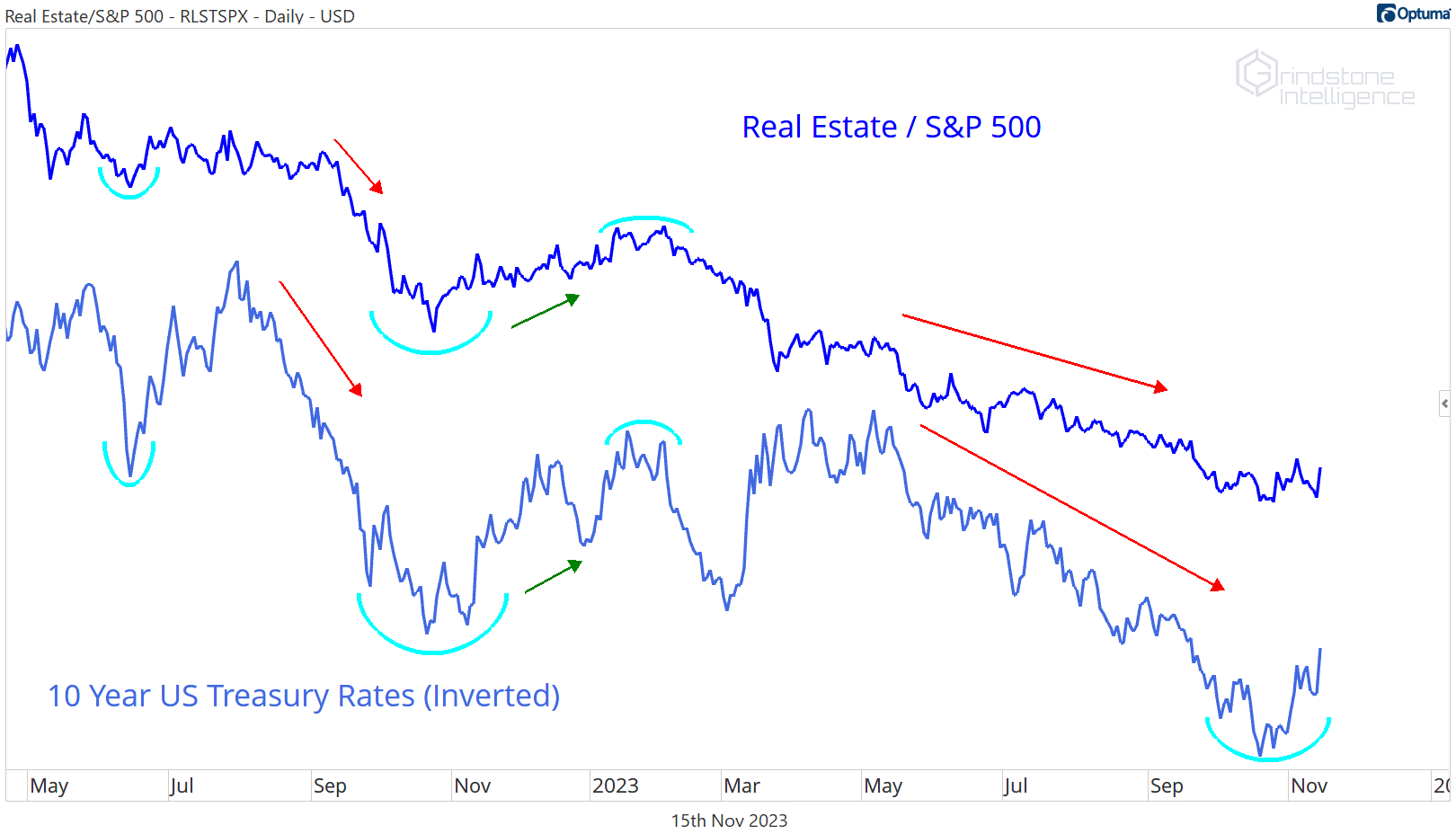

If you’re looking for a reason for Real Estate’s troubles, blame the rise in interest rates. Take the trend of the sector vs. the rest of the market, then overlay that with Treasurys - you’ll find an eerie resemblance. When interest rates go up, RE underperforms.

Higher interest rates are a two-fold headwind. One, they make fixed income more attractive to investors and lower the relative appeal of stocks with high dividend yields. Consider this: Two years ago, 10- year Treasury rates were just 1.5%, while the dividend yield on Real Estate stocks was among the highest in the S&P 500 at about 3%. Today, the risk-free Treasury yield is more than 4.5%, while Real Estate pays the highest dividend yield of any sector at just 3.5%. For income-focused investors, there’s little comparison.

Second, rates are a problem for the business activities of real estate stocks, which tend to have high debt loads. Real Estate has just a 2.5% market cap share of the S&P 500’s, but it has a 5.5% share of net interest expense. By that measure, Real Estate stocks are already paying 2.5x more interest than the average S&P 500 company. Only the Utilities compare, and they’re even worse, with a ratio interest expense to market cap share of 6x.

The Utilities have one distinct advantage, though. The average weighted average maturity for Utilities stocks is more than 13 years - double that of Real Estate at 6.7x. That means Real Estate companies will be repricing their high debt loads at higher interest rates at a much faster pace.

To sum it all up, higher interest rates = bad news for real estate.

What about lower rates, though?

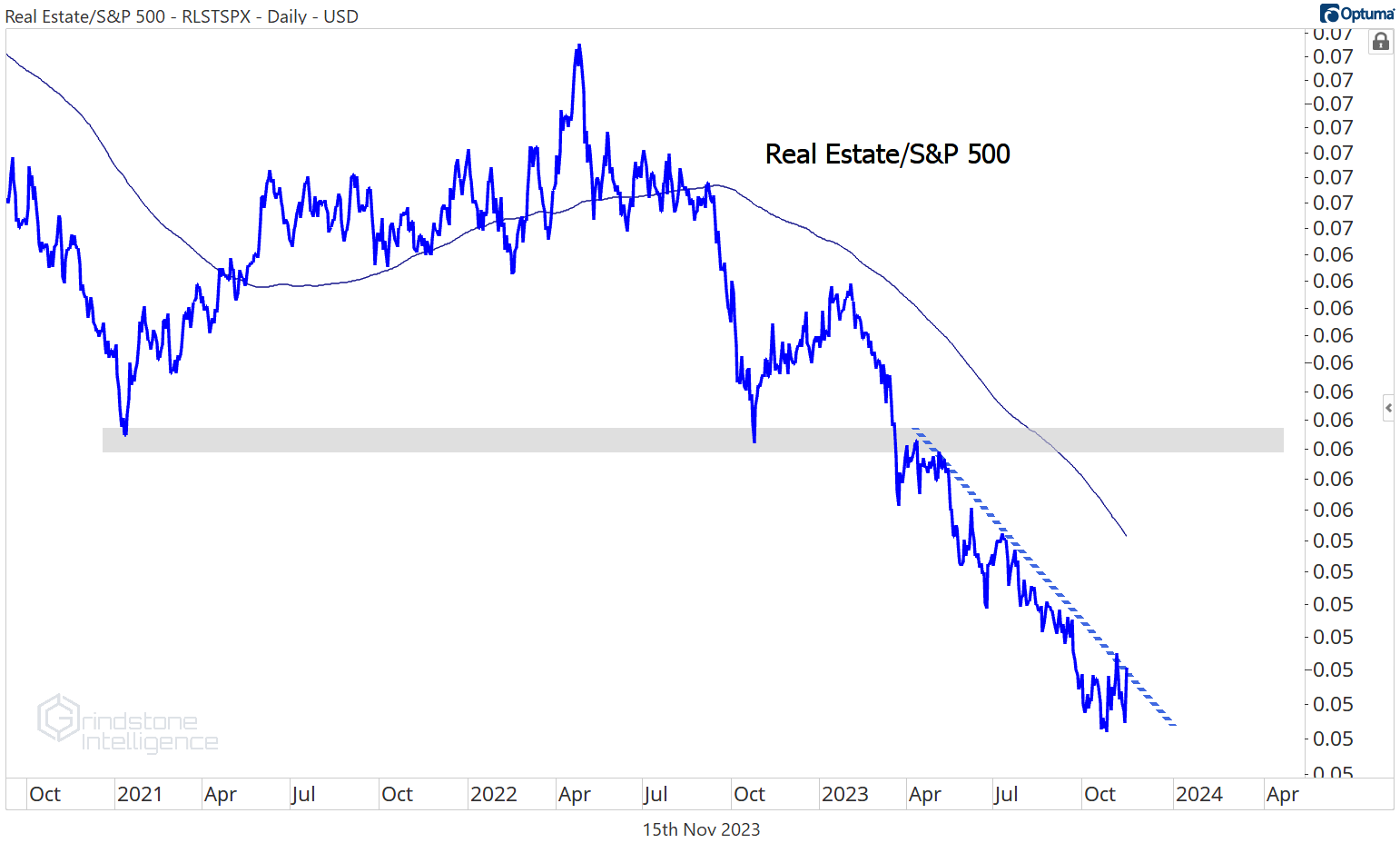

Following last week’s soft economic data and Tuesday’s cooler-than-anticipated inflation report, Treasury rates have already dropped nearly 50 basis points from their peak. And Real Estate stocks have responded accordingly, jumping more than 10% from their October lows. That’s got the sector back above its October 2022 lows and threatening to challenge the 15-month downtrend line.

How the sector responds to that potential area of resistance would go a long way towards answering our question of whether this is just a mean reversion following a bullish momentum divergence and a failed breakdown, or whether this is the start of a major trend reversal. We’d be very impressed if the sector breaks the downtrend line that’s been in place for the group relative to the S&P 500. That alone wouldn’t be enough progress to make us excited about owning a bunch of the sector (we’re still looking at a ratio stuck below the 2021-2022 lows), but it would be an important first step.

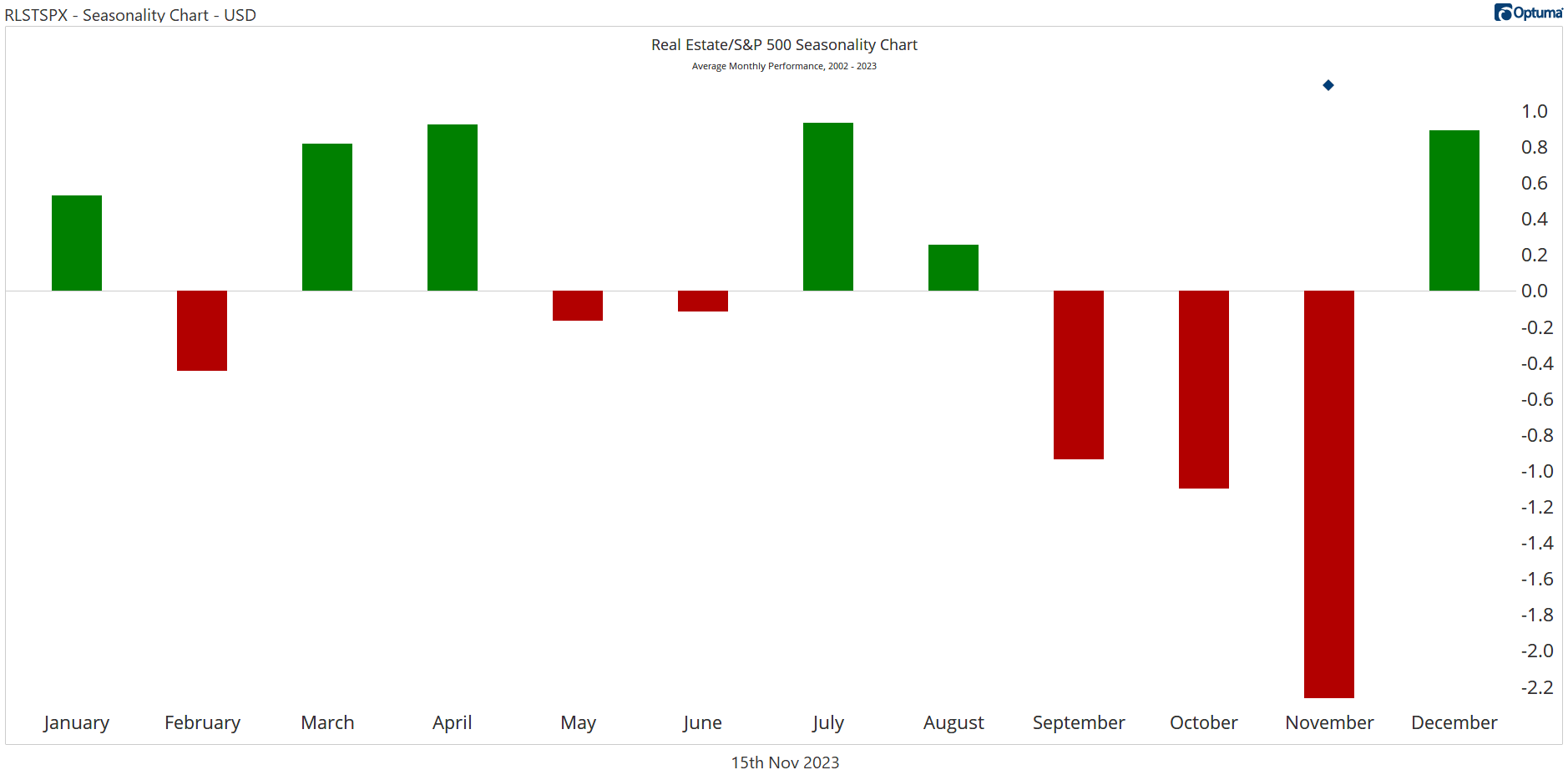

If that first step comes over the next few days, it would be in spite of a huge seasonal headwind. Historically, November has been the absolute worst month to own Real Estate.

It’s my belief that seasonality often gives the best information in hindsight - when prices don’t follow seasonal patterns, that’s when it’s time to really pay attention. If Real Estate continues outperforming during its worst month, what do you think it’s capable of in December, a historically bullish month? It’ll be really hard to ignore.

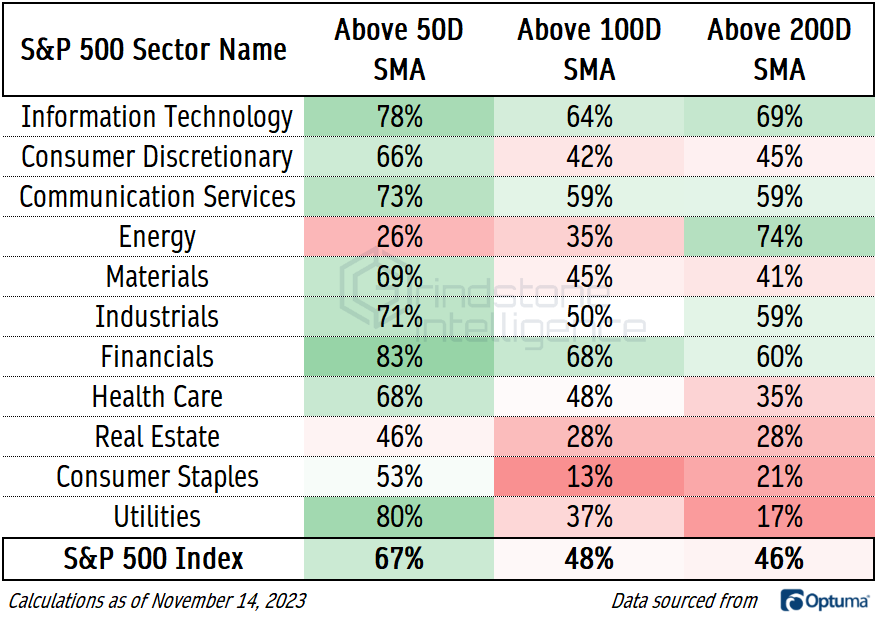

We’re still skeptical that it can close out the month, given the weak breadth that permeates the group. Less than one-third of stocks in the sector are above their 100 and 200-day moving averages, a share that is significantly below the index average.

And fewer Real Estate stocks have set a new 52-week high than in any other sector, with 84% still stuck in a long-term, lower-lows regime. Perhaps it’s not fair to expect a bunch of new 52-week highs within a sector that just came out of a big failed breakdown, but shorter-term trends aren’t much better. Just 19% of the sector has so far managed to set a new 3-month high.

It’ll take more progress from interest rates and improvement beneath the surface before we’ll have much confidence in Real Estate as more than a short-term leader.

Keep reading with a 7-day free trial

Subscribe to Grindstone Intelligence to keep reading this post and get 7 days of free access to the full post archives.