The Truth About Long-Term Stock Market Returns

Since the inception of the S&P 500 in 1928, stocks have delivered an outstanding annualized return of 10%. You read that right. Ten percent per year. To everyone with a 90-year time horizon that invested all their money in a zero-fee, tax-free, and non-existent index fund, then rode out the turmoil of the Great Depression, WWII, the Dot Com crash, and the 2008 Financial Crisis, reinvesting dividends and never selling along the way: Congratulations. You crushed it.

For the rest of us (that is, everyone), it’s time to face reality. As investors, many of us have been conditioned to believe that 10% per year is not only possible, but a near-certain outcome if we just stick to the plan. It’s a comforting thought. The truth can be harder to swallow: 10% per year is not quite the same as 10% every year. Moreover, you don’t have 90 years to leave your assets untouched, and you probably won’t sit by and watch your retirement account get cut in half without taking action. In short, just playing the game doesn’t mean we’re entitled to double-digit returns over our investment horizon.

Much like the last 10 years, the long-term history of the S&P 500 price index (below) has been marked by periods of uptrends and consolidations. Over the long term, market participants benefited from extended periods of outstanding growth, but sometimes invested for years without meaningful asset appreciation.

True, dividends would add to the return during the stagnant periods shown above, and it’s not entirely fair to exclude them. Then again, it’s not entirely fair to exclude inflation either. Inflation doesn’t get much attention anymore, especially when talking about investment returns – for that we can thank the Fed and 25 years of core CPI readings below 3%. But since we’re analyzing 100 years of historical data, not just the last 25, we can’t afford to ignore it. So what happens if we included both dividends and inflation? We still see extended periods of time where stocks provide no meaningful appreciation in purchasing power.

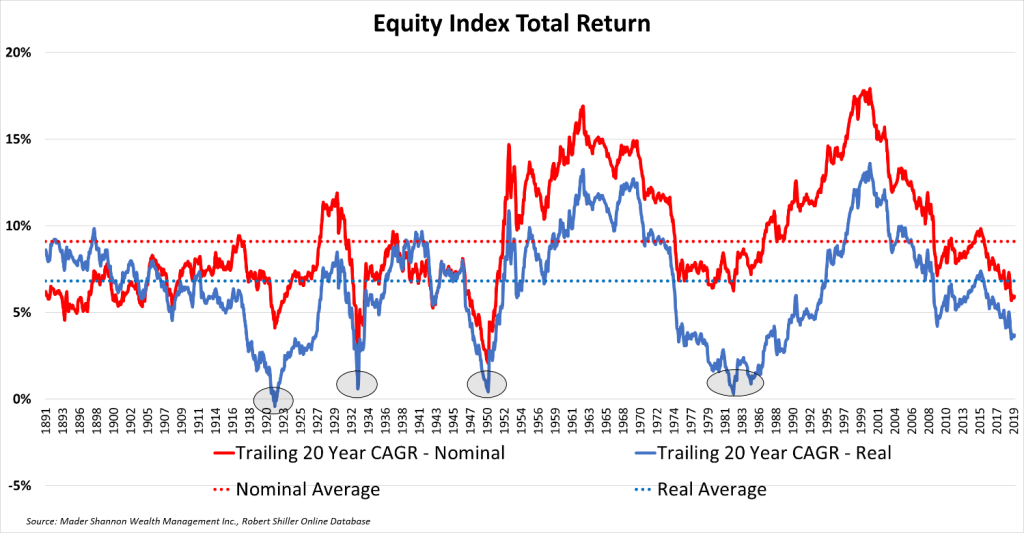

Each data point in the chart below represents the annualized real total return for the S&P 500 over the preceding 20 years. (The underlying equity and inflation data go all the way back to 1871, courtesy of Robert Shiller’s online database.)

No less than 4 times in the past century, equities provided less than 1% in real return per year for a 20-year period. For plenty of savers, 20 years is longer than their investing life! And though the annualized real return over the entire dataset is a respectable 6.9%, the 3.9% average achieved over the most recent 20-year period should remind us just how volatile returns can be. Mr. Market doesn’t care about our retirement plans. He doesn’t owe us anything.

To be sure, stocks are still one of the best long-term wealth generators, but investment returns are cyclical. They can come in bunches or not at all. Going all in, crossing your fingers, and hoping for the best might make you rich – but hope isn’t much of an investment strategy.

Nothing in this post or on this site is intended as a recommendation or an offer to buy or sell securities. Posts are meant for informational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in posts. Please see my Disclosure page for more information.

The post The Truth About Long-Term Stock Market Returns first appeared on Grindstone Intelligence.