The Weekly Grind: October 9, 2023

Week in Review

The S&P 500 rose in the first week of October after 4 consecutive weeks of decline. Another streak also ended last week, when the US Dollar index failed to close higher. The Dollar’s run ended just short of the record set back in 2014. Interest rates, meanwhile, continued to rise, with 30-year Treasury yields briefly surpassing 5%. Crude oil dropped sharply. It’s 9% selloff was the worst since the failure of SVB back in March.

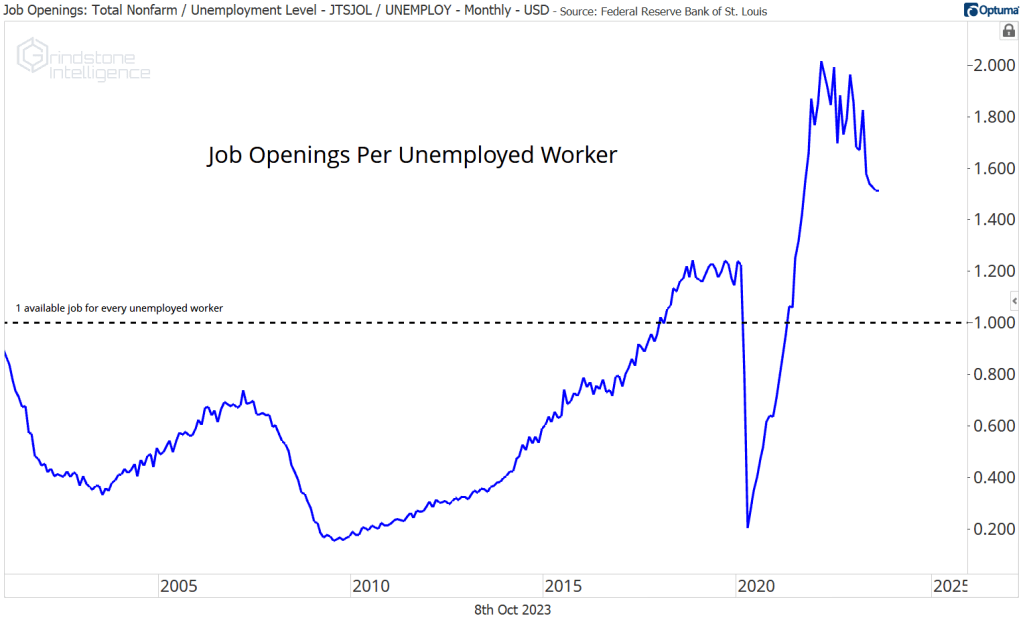

All year, economists have been waiting for the ‘inevitable’ recession that comes with a massive Federal Reserve tightening cycle. Jerome Powell & Co. have raised short-term interest rates by more than 5% since last spring, the fastest pace of hikes since Paul Volcker’s efforts to break the back of inflation in the 1980s. But instead of recession, the US economy keeps on chugging along. The US added 336,000 jobs in September, the best payrolls print since January. That keeps the number of job openings per unemployed worker at roughly 1.5 – far higher than anything the country experienced prior to 2020.

Market Internals

Breadth was a concern for most market watchers throughout March, April, and May, as the rally in growth stocks obscured lackluster performances from value-oriented names during the spring. In June and July, trends began to broaden, but the dog days of summer took their toll. After index-level declines in August and September, breadth is weaker than it’s been all year.

Long-term trends remain healthiest in the Information Technology and Energy sectors, where more than half of constituents are still above their long-term moving averages. Traditionally considered risk-off areas, the Utilities and Consumer Staples sectors are the most weakly positioned. Fewer than 10% of stocks in those groups are in technical uptrends – no matter which timeframe you choose.

What’s Ahead

Here’s what to watch in the week ahead:

The post The Weekly Grind: October 9, 2023 first appeared on Grindstone Intelligence.