The Weekly Wrap: December 12, 2022

Week in Review

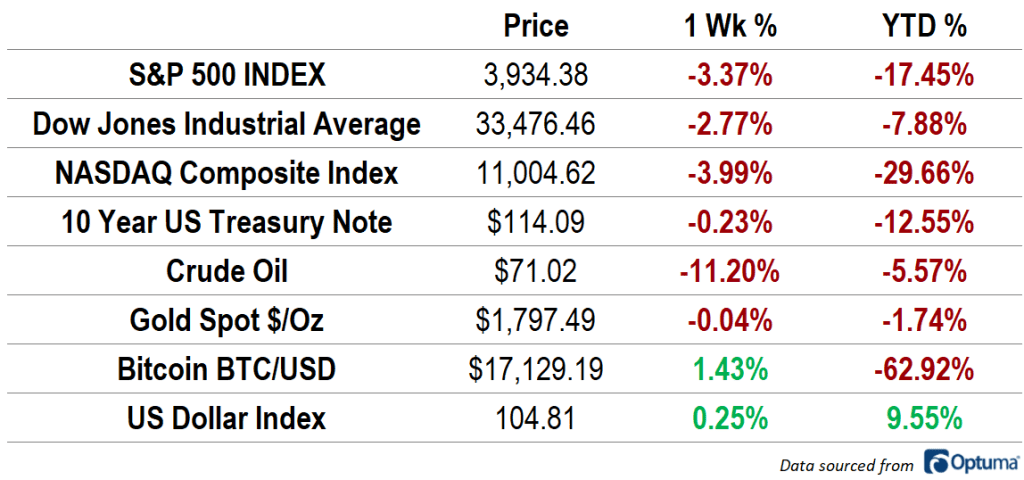

Asset prices were back under pressure last week as the Nasdaq Composite led stocks lower, dropping 4%. The S&P 500 Index fell 3.4% to close 17.5% lower for the year, and the Dow Jones Industrial Average slipped 2.8%. It’s still the best performing of the major US indexes in 2022, down less than 8%. Crude oil saw a significant weekly decline, dropping 11.2% as the US Dollar and interest rates both rose. The Dollar is nearly 10% higher on the year. Gold was mostly unchanged, ending the week near $1800. Bitcoin prices managed to rise more than 1%, but the cryptocurrency is still down more than 60% for the year.

Crude oil fell to its lowest levels of the year as markets continue to weigh slowing global activity against the threat of further supply disruptions. Most economists forecast a US recession occurring sometime in the next twelve months, with the consensus expectation being a mild contraction beginning in 2H 2023. The outlook for Europe is worse, as they’re already reeling from the impacts of war in the eastern portion of the continent. Despite the slowdown, OPEC refrained from further production cuts at their most recent meeting, given potential shortages stemming from the European Union decision to cap prices on Russian oil exports.

Earnings Expectations and Valuation

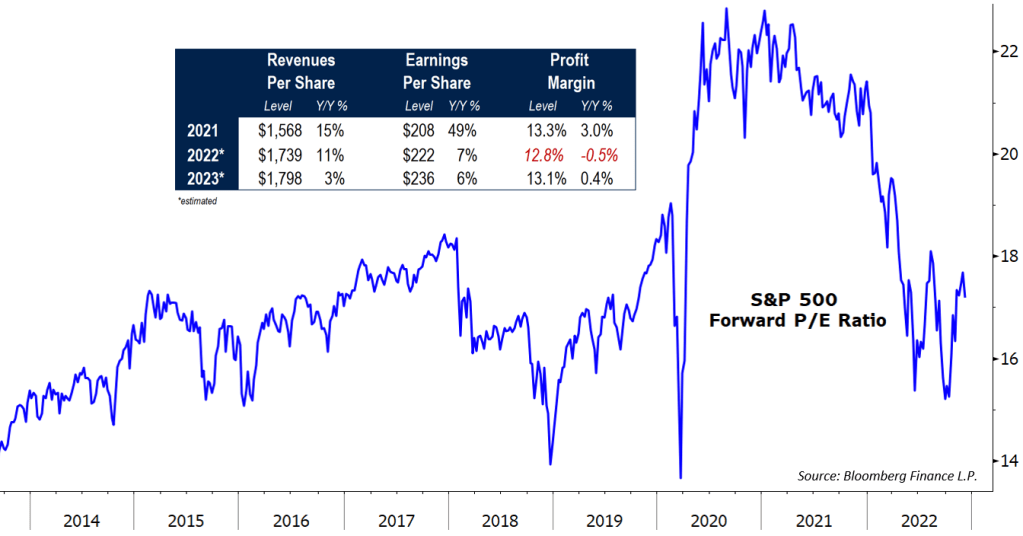

This year’s market selloff has not been matched by a proportionate decline in earnings expectations. That’s driven the S&P 500’s forward price-to-earnings ratio from a historically elevated level of 23x to 17x, which more closely aligns with the average over the last 30 years.

Earnings growth for large cap US stocks is expected to end the year at 7%, thanks to double-digit revenue growth. That’s near the long-term average, but a notable deceleration from prior years. In 2023, the consensus expectation is for 6% earnings growth, but that estimate relies on a reversal of the margin pressures seen in 2022.

What’s Ahead

The Federal Reserve will decide whether and by how much to raise short-term interest rates on Wednesday, as they continue on their quest to curb inflation. They’ll get one last piece of critical data on Tuesday morning, when the Bureau of Labor Statistics publishes Consumer Prices for November. It would take a material surprise in the CPI report to shift markets away from their expectations for a 0.5% rate hike. NFIB Small Business Optimism is slated for Tuesday morning, and last month’s retail sales are reported on Thursday. On Friday, S&P Global releases preliminary results for their December Purchasing Managers Index survey.

The post The Weekly Wrap: December 12, 2022 first appeared on Grindstone Intelligence.