The Weekly Wrap: September 19, 2022

Week in Review

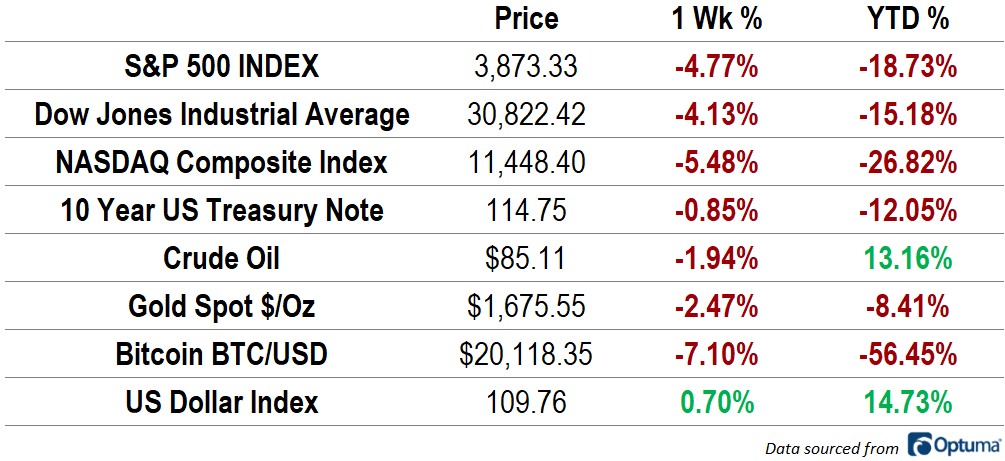

It was a tough week for investors, as equity indexes fell more than 4% to their lowest levels in 2 months. The S&P 500 fell 4.7%, and the Nasdaq dropped 5.5%. Bonds provided no safe haven for investors, with the 10-year Treasury yield rising near 3.5% and bond prices falling 0.9%. Oil prices declined 1.8%. Gold dropped briefly to its lowest point in 2 years before settling 2.7% lower. The US Dollar index continues to be a major headwind for asset prices, rising 0.6% for its highest weekly closing print since 2002. Bitcoin remained volatile, erasing early-week gains before dropping 7.7%.

Tuesday’s CPI report for August came in hotter than street expectations, triggering a renewed downturn in risk assets. Though inflation decelerated on a year-over-year basis, most of the decline was related to lower energy prices. Core inflation – which strips out volatile food and energy components – rose to 6.3% Y/Y. Housing costs moved up 0.7% from July, and Medical Care Services rose 0.8%. Those are the fastest M/M rates for each category, which together comprise more than half of the Core CPI reading. The worse-than-expected report could set the stage for a 1% rate hike by the Fed next week, but the base expectation is still for 75bps.

Earnings Expectations and Valuation

This year’s market selloff has not been matched by a decline in earnings expectations. That drove the S&P 500’s forward price-to-earnings ratio from a historically elevated level of 23x to less than 16x, which more closely aligns with the average over the last 30 years.

Earnings growth for large cap US stocks is expected to end the year at 9%, backed by double-digit revenue growth and stable profit margins. In 2023, the consensus expectation is for 8% earnings growth. That’s still near the long-term average, but a notable deceleration from prior years. That estimate relies on meaningful margin expansion.

What’s Ahead

All eyes are on the Federal Reserve this week as they prepare to hike rates for the fifth consecutive meeting. Futures markets are pricing in another 0.75% hike. The early part of the week will be dominated by housing data, with the NAHB Housing Market Index released on Monday, Housing Starts on Tuesday, and Existing Home Sales on Wednesday morning before the FOMC decision. The Bank of Japan and Bank of England both hold meetings before markets open on Thursday morning, and we’ll close the week with September flash PMIs from S&P Global

The post The Weekly Wrap: September 19, 2022 first appeared on Grindstone Intelligence.