Top Charts from the Financials Sector - 12/15/2023

Sector outlook and trade ideas

This week, the list of new 52-week highs set new 52-week highs. Whether you’re looking at the NYSE, the NASDAQ, or the S&P 500, the number of stocks breaking out is at its best level since early 2021.

With all these new highs, it seems an eternity ago (rather than just 9 months) that a spate of bank failures was rocking financial markets. In the first half of March, the S&P 500 Financials sector dropped 15%, led by a staggering 50% decline in regional banks. With interest rates still on the rise and unprecedented paper losses sitting on bank balance sheets, it wasn’t hard to believe the failures of SVB, Signature Bank, and Silvergate were just the tip of the iceberg.

Since that mid-March bottom though, any observer might conclude nothing out of the ordinary had happened within the Financials. They’ve tracked the benchmark S&P 500 more closely than any other sector over that period.

And just like the S&P 500, the Financials sector just broke out to new 52-week highs.

Earlier this year, we used the Financials as a risk trigger. As long as the group was holding above the 2020 highs, we said, there was no reason to be outright bearish on the outlook for stocks. A neutral approach was fine. And if the Financials were breaking down? Sure, then we could start talking about renewed weakness in the broader market. But as long as the Financials were holding up, how bad could things really be?

We’re looking at the Financials in a similar way now. As long as the group is above the February 2023 highs, we can’t be anything but bullish on the sector and the market overall.

The next question is how bullish we should be on the group.

At least 90% of the sector’s constituents are above each their 50, 100, and 200-day moving averages. No other sector besides Real Estate can say the same.

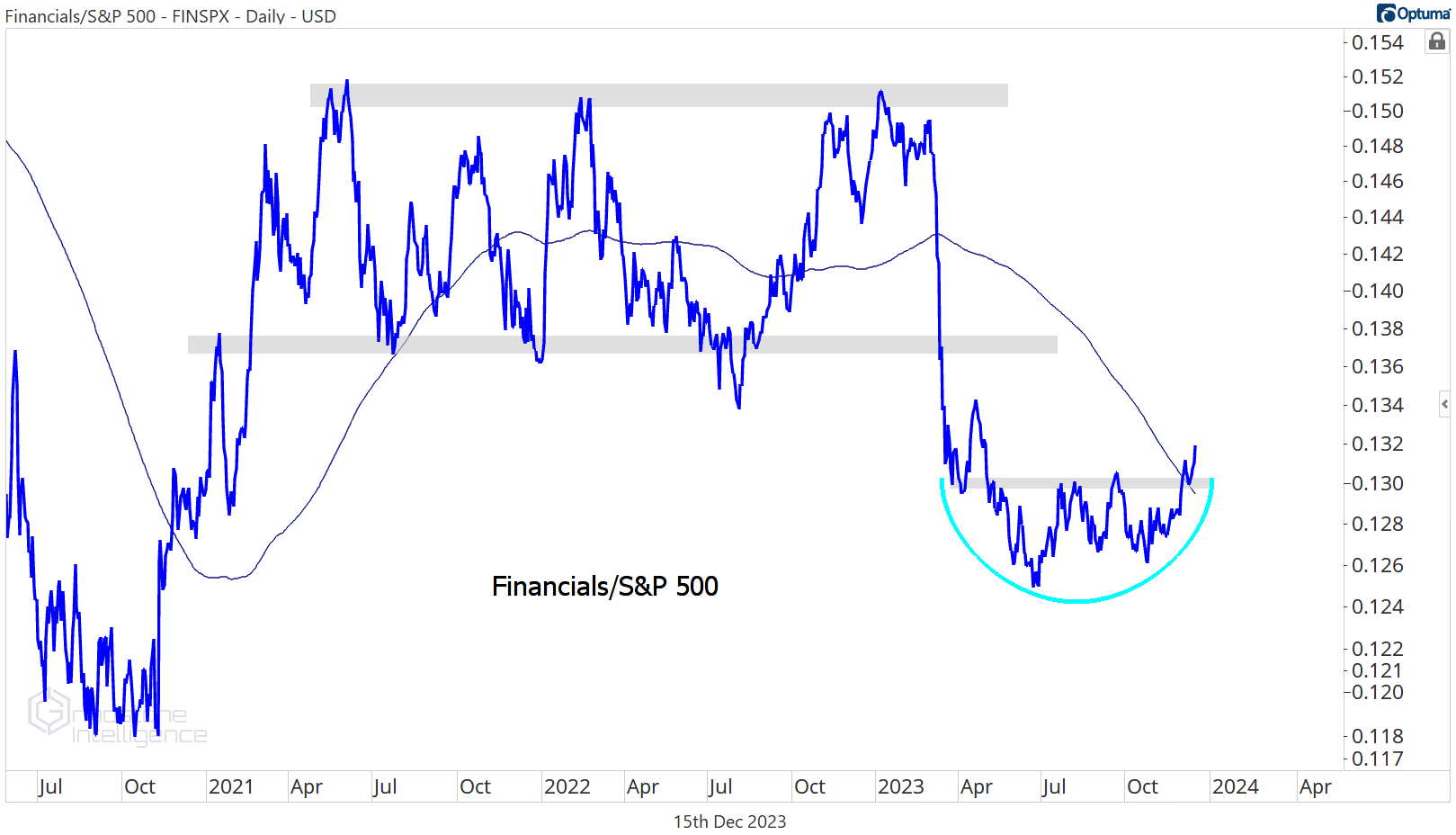

And relative to the rest of the market, the sector has bottomed. The Financials/S&P 500 ratio just broke out to 6-month highs and is above its 200-day moving average for the first time since March.

That outperformance will last as long as value stocks are in favor. The Russell 1000 Growth peaked relative to Value back in November - at the exact same place it did back in 2020 and 2021 - and December is historically one of the worst months for the Growth/Value ratio.

Only Tech features a wider weightings disparity than the Financials when it comes to the two indexes. The Financials are the largest component of Value at more than 20%, but they represent a mere 6.5% of Growth. So as long as the Growth/Value ratio remains stuck below the former highs, it makes sense to favor the Financials.

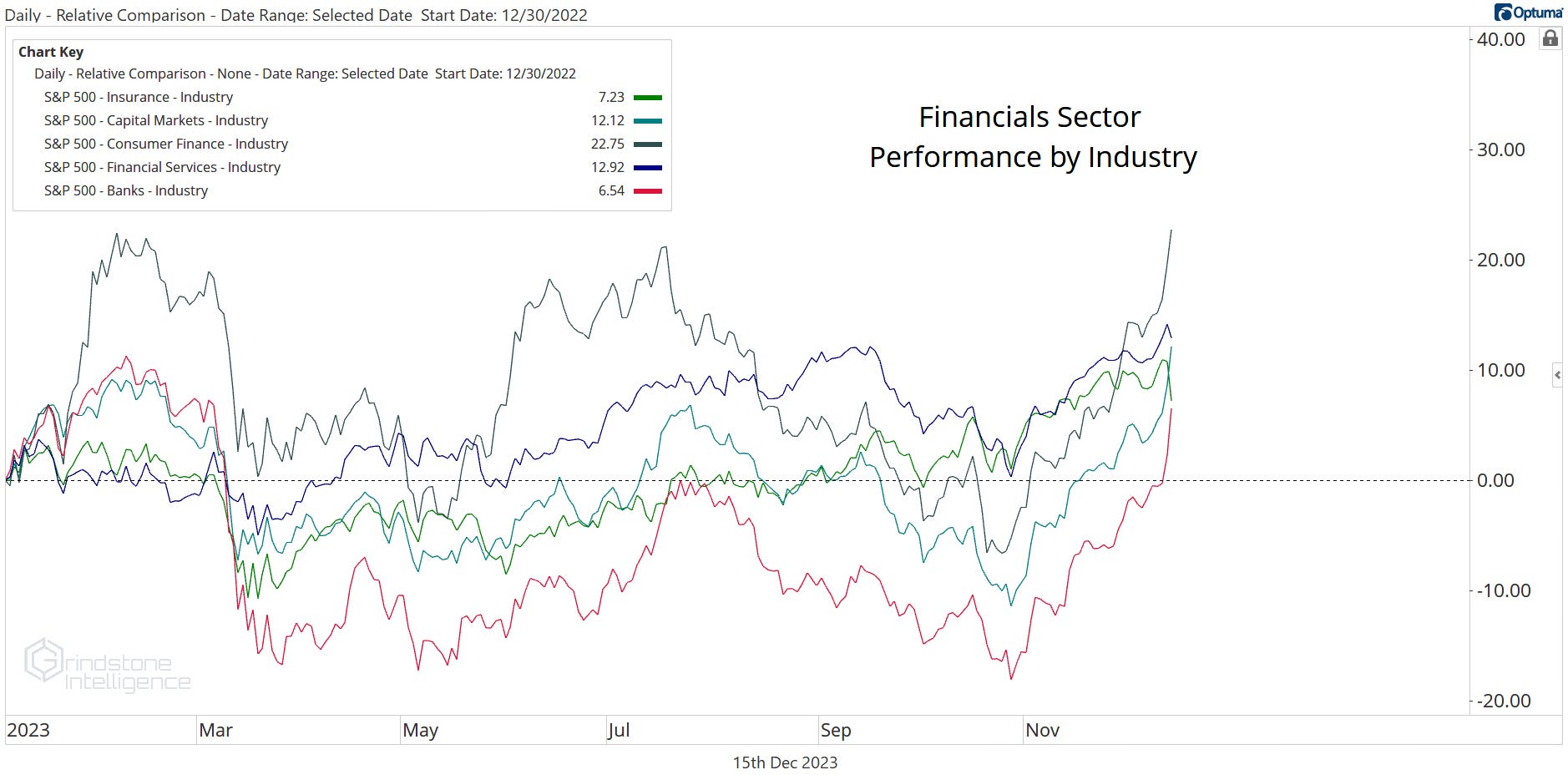

Digging Deeper

The banks are the most interesting industry these days. We’re been waiting patiently (ok, perhaps a bit impatiently) for the regional banks to move above this congestion area near $80. It kept us on the sidelines in July, and protected us from a re-test of the COVID lows over the fall. The wait has ended. The banks are breaking out to six-month highs and there’s no reason to be bearish on them as long as they remain above those summer swing highs.

Leaders

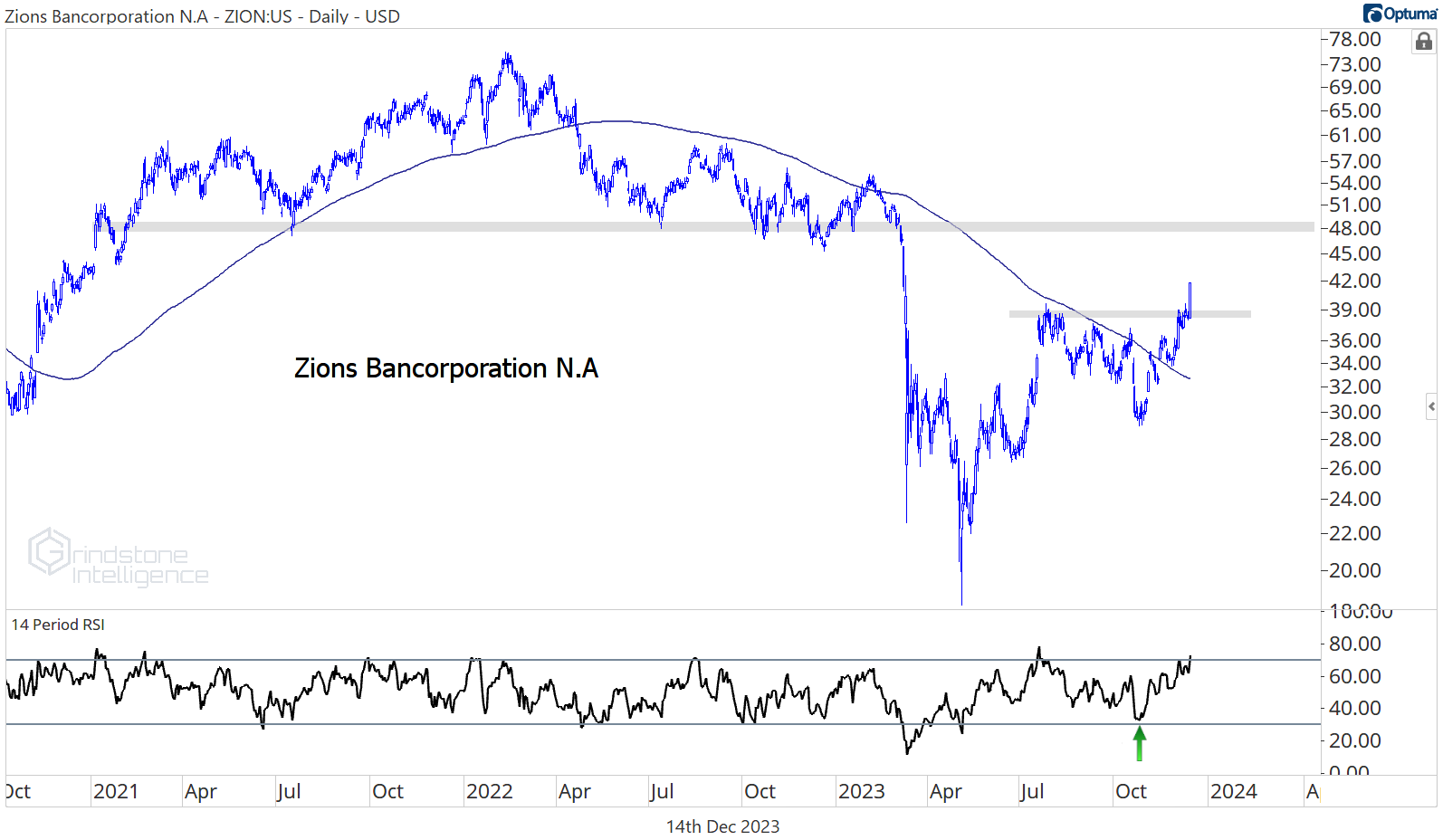

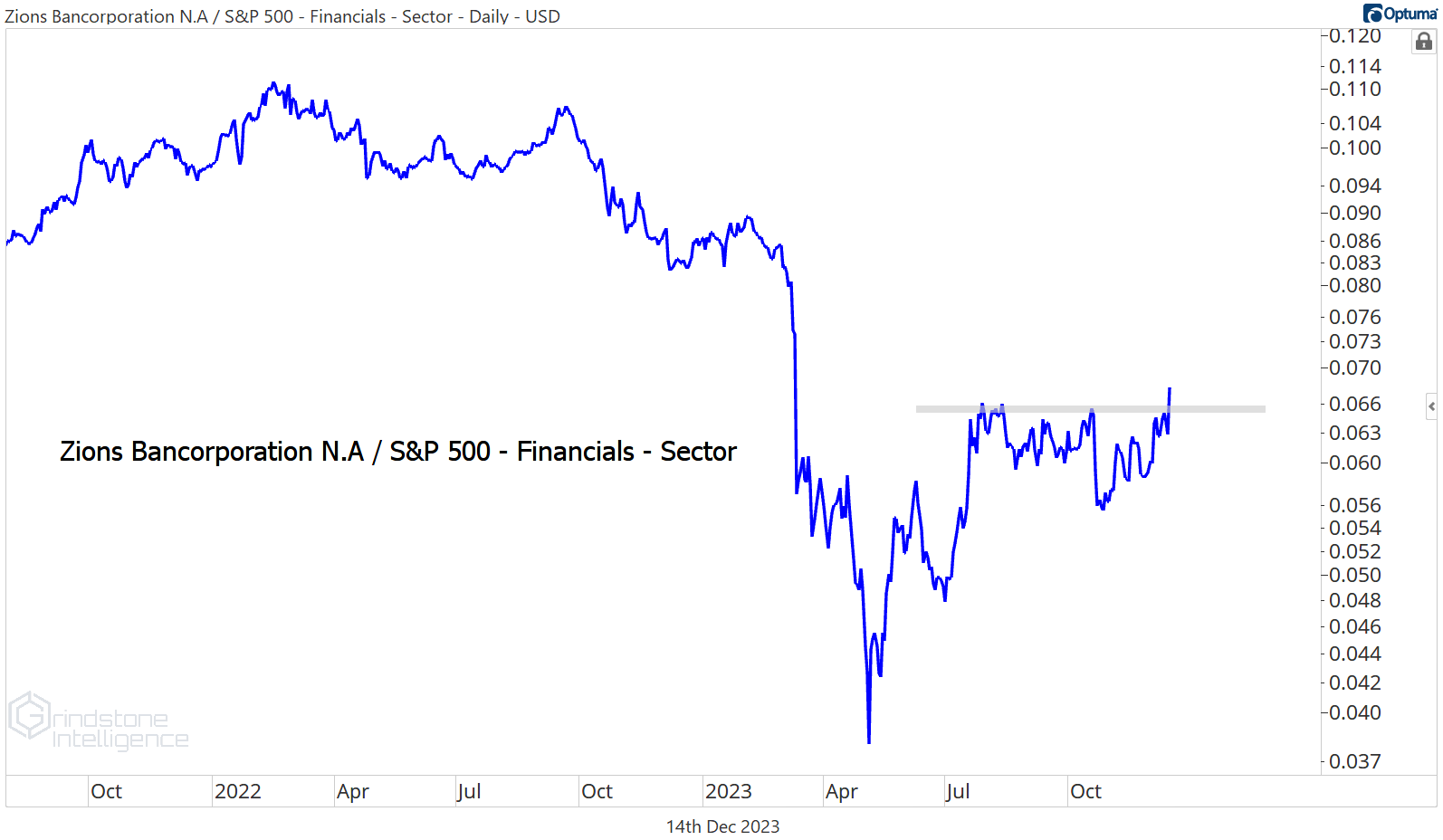

Zion Bancorp is the cleanest setup within the regional banks. It managed to stay out of oversold territory this October, and unlike the sub-industry as a whole, ZION never approached the spring lows.

That relative strength is readily apparent - ZION just broke out of a 5-month base vs. the rest of the sector.

We want to buy any pullbacks in ZION toward $39 with a target back at the spring breakdown level near $47.

Capital One is among the sector’s biggest winners for the year after a 23% rally over the last 4 weeks. It just broke out to new 52-week highs. Once again, we don’t particularly want to chase here, but we definitely want to be taking advantage of any pullbacks toward the $120 breakout level. Our target is the 61.8% retracement from the bear market decline, which is near $142.

Losers

Arch Capital is a prime example of why we should set targets and stick to them. When the stock was ripping into the end of October, it was hard not to think they’d keep going up forever. But we set targets for a reason. Here’s what we said last month:

“Arch Capital Group reached our target of the 261.8% retracement from the 2020 selloff, and now we want to step aside and see how the sector’s second-best YTD performer responds.”

They responded by being the worst stock in the sector over the last 4 weeks. This is one to leave alone until further notice.

Other Notable Charts

We continue to like Fiserv after it successfully broke out of this multi-year base. FI was one of the best uptrends you could find in the decade leading up to COVID, and now it’s had some time to digest all those gains. The first attempt to get going this summer resulted in a failed move, but after the false start, FI’s second attempt is bearing fruit. We want to be long above $123 with a near-term target above $150.

Other payments-related stocks are also breaking out. For Visa we want to be long above $250 with a target of $290, which is the 161.8% Fibonacci retracement from the 2021 decline. Check out momentum getting the most overbought that it has in 2 years, too. That’s not something you see in a downtrend.

Blackrock just broke out of a monster base. We want to buy any pullbacks toward $780 with a target back at the former highs near $970.

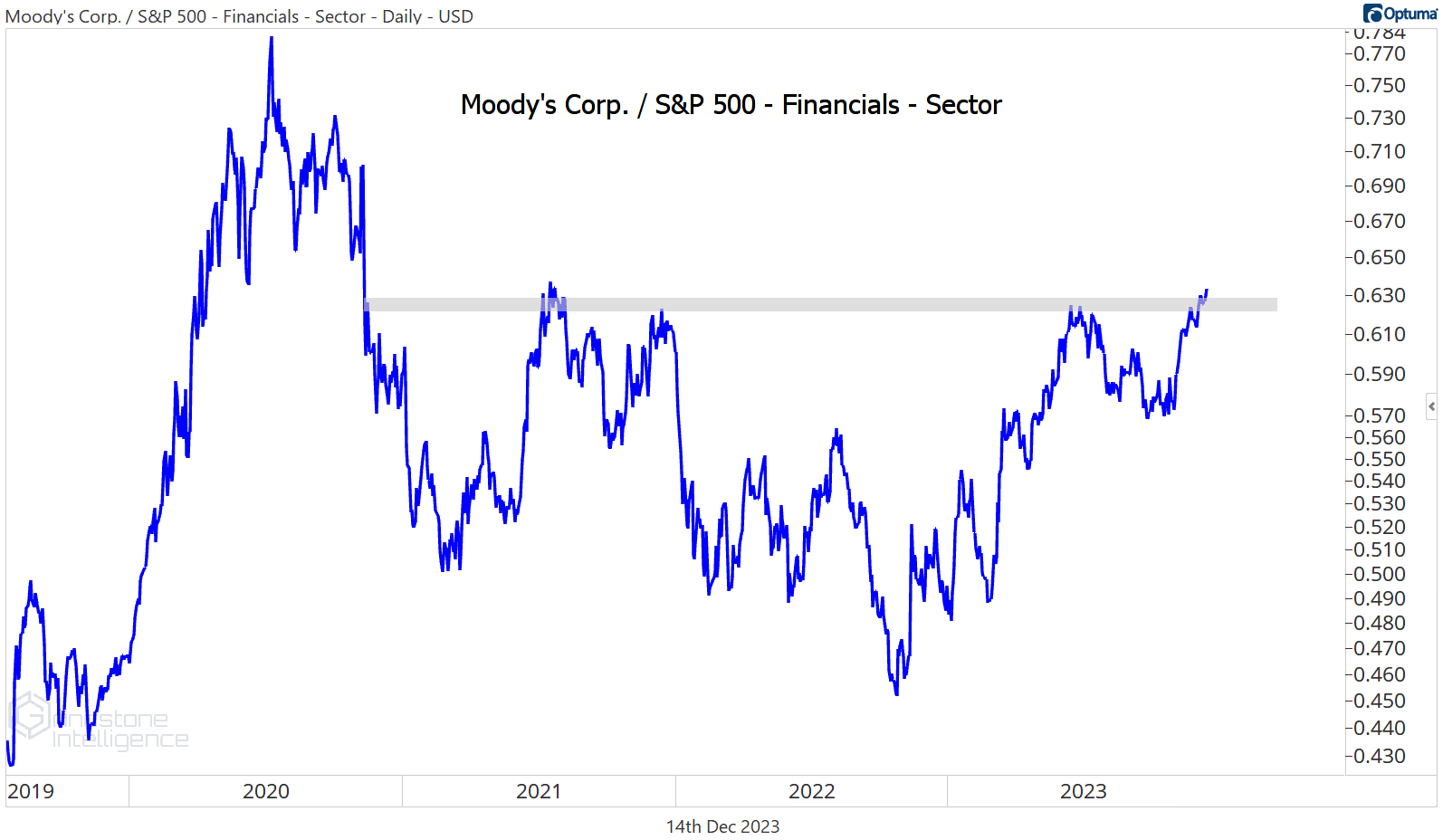

Moody’s is nearing potential resistance at the 2021 highs, which means this isn’t a place to be initiating new long positions.

We do love the relative strength we’re seeing in MCO relative to the rest of the Financials, though. Here they are trying to break out of a multi-year relative base.

We want to own MCO above $410 - and only above $410 - with a target above $500.

That’s all for today. Until next time.