Undoing the 2017 TCJA: What a Corporate Tax Hike Could Mean for Stocks

On December 21, 2017, the Tax Cuts and Jobs Act was signed into law. Though the 185-page bill contained a multitude of changes to federal collection laws, the most important for publicly traded companies was a reduction in the corporate tax rate from 35% to 21%. The cut was a direct benefit to the bottom line of most businesses and helped drive earnings to a year of outsized growth in 2018. For the S&P 500, EPS jumped 21% that year, roughly 3x the long-term average.

The TCJA was a popular debate topic during the ensuing 2018 and 2020 election cycles, and the current administration ran on a platform that included moderating the corporate tax cut. Their initial target: 28%. With majority control in both houses of Congress, the effort to enact the increase is likely to succeed, though the timeline for passage is unclear. The impact of the 2017 act may offer clues as to how a new tax bill would affect stocks.

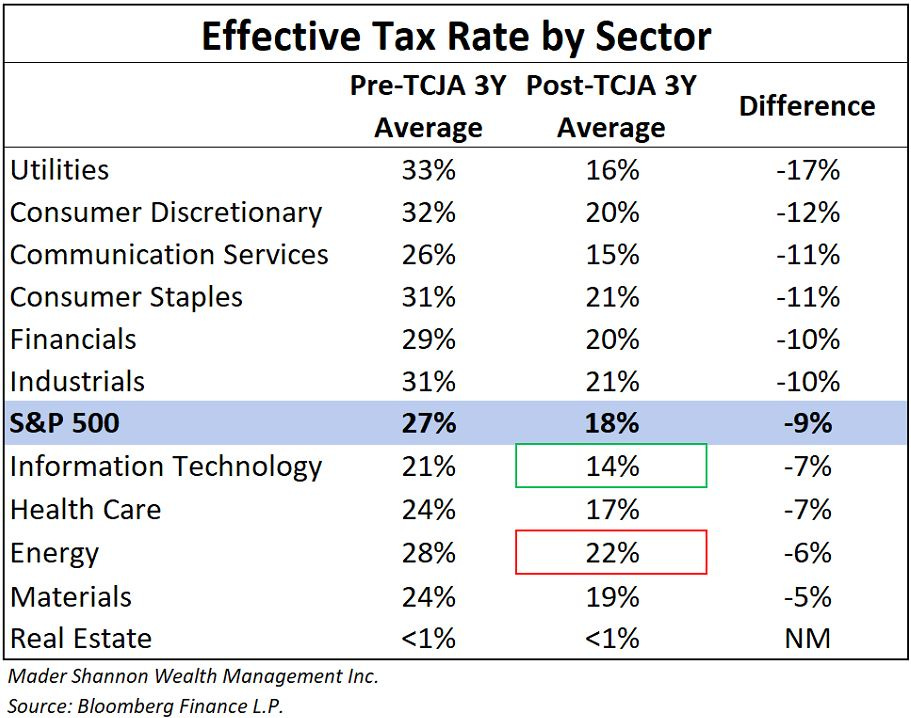

In the years before the TCJA, the effective tax rate for the S&P 500 index was roughly 27%, eight points below the headline rate thanks to a complex array of deductions and loopholes, but still among the highest in the advanced world. The tax cut aggressively lowered the headline rate by 14%, but also eliminated some loopholes – from 2018 to 2020, the aggregate effective rate was only 9% lower than before. As is usually the case, some sectors benefited more than others.

The Utilities sector, which formerly paid the highest rate, saw by far the largest payment reduction. Meanwhile, sectors like Information Technology, Health Care, and Materials, which paid among the lowest rates, saw smaller reductions. Notably, Tech managed to maintain its leading tax rate position (excluding Real Estate, whose constituents are taxed in a different manner), while Energy has paid the highest effective rate in recent years.

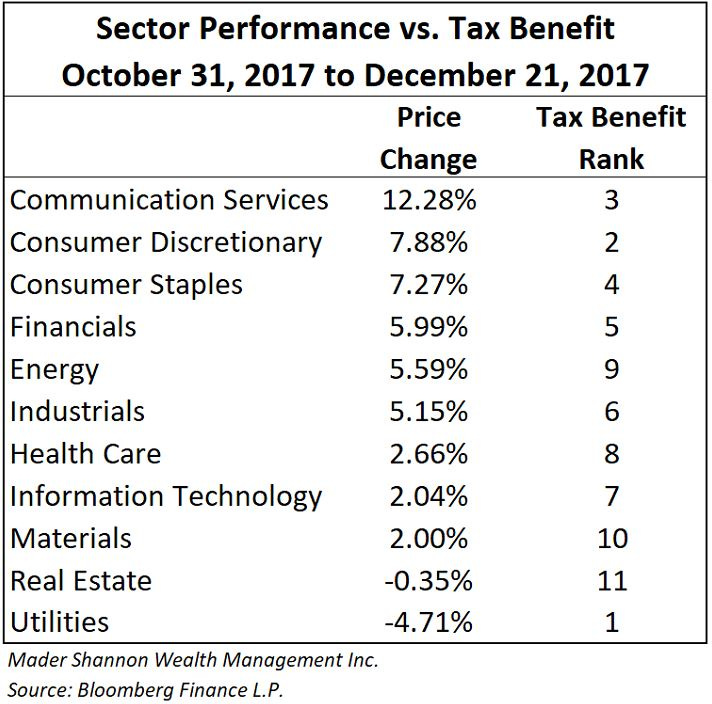

In large part, stock prices responded to the cut in logical fashion. The first text of the TCJA bill was released by House of Representatives members on November 2, 2017. It took only a month and half for the text to be finalized by both houses of Congress and signed by the President – a breakneck pace in the federal legislature. Because the Act was so significant and the timeline so short, much of the change in stock prices over that time can be attributed to the bill. The table below is sorted by sector performance between the two key dates. The third column notes the relative reduction in effective rate we observed in the table above.

The Utilities sector stands out. Though it received the largest tax rate reduction, it turned in the worst performance. Investing can be hard, sometimes. Putting aside that clear outlier, the correlation between performance and rate reduction is pretty remarkable. The sectors benefitting the most from the TCJA meaningfully outperformed those benefitting the least. Sometimes, investing can be easy.

Should a corporate tax hike be implemented, it seems reasonable to assume that sectors and companies which saw the most benefit in 2017 would face the most harm now. Of course, it’s never quite that simple. We are talking about politics in modern America, after all. A potential tax bill will undoubtedly be riddled with provisions that benefit some groups and hinder others. We’ll know more of those details soon enough. In any case, it’s important to keep the hike in context: even if the target of 28% is achieved, the effective rate paid by businesses will still be lower than it was prior to 2017.

Nothing in this post or on this site is intended as a recommendation or an offer to buy or sell securities. Posts on Means to a Trend are meant for informational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in posts. Please see my Disclosure page for more information.

The post Undoing the 2017 TCJA: What a Corporate Tax Hike Could Mean for Stocks first appeared on Grindstone Intelligence.