What’s Behind the Underperformance of the Average Stock?

How’s the stock market doing this year?

The answer, even more than usual, depends on how you define ‘the stock market’. Is it the Dow? The S&P 500? Perhaps the NYSE Composite?

If the market means the NASDAQ, things look pretty great – that index is up nearly 30% for the year. Dig a little deeper, and the picture isn’t quite so rosy. The Dow Jones Industrial Average and NYSE Composite are barely in positive territory. The small caps are actually down for the year. This is a market defined by the haves and the have-nots.

That bifurcation is made clear by the difference between the performance of the widely-used S&P 500 Index, which is up 13% this year, and the performance of the equally weighted S&P 500, which is flat.

For those unfamiliar with index construction, here’s a quick primer. There are generally 3 ways to weight the members of an index: by market capitalization, by price, or equally. A market cap-weighted index like the S&P 500 weights its members by their size. For example, Apple, a company worth nearly $3 trillion, is about 30x more important than Goldman Sachs, a company worth about $100 billion. A price-weighted index, like the Dow Jones Industrial Average, weights its components based on their share price. Using that method, Goldman Sachs (~$300 per share) is more important than Apple (~$180 per share). An equally weighted index is constructed exactly as it sounds: each component carries the same level of importance.

Comparing the equally-weighted S&P 500 to the normal, market cap-weighted one tells us a story about how the ‘average’ stock is doing. 2022 was the year of the ‘average’ stock. 2023 is not.

So what’s behind this year’s underperformance? In large part, it’s because the mega caps are driving the S&P 500’s gain.

That’s not a secret. Just hop on Twitter and you can find a cacophony of investors complaining about the narrow leadership – and rightfully so. The so-called Magnificent 7 (Apple, Microsoft, NVIDIA, Alphabet, Meta, Amazon, and Tesla) together account for nearly all of the S&P 500’s year-to-date rally.

But it’s not just a market cap story.

It’s also a story about sector rotation. We took the ratio chart from above and overlaid it with the ratio of Value stocks to Growth stocks. If we didn’t have the labels, would you be able to tell the difference?

Check out the differences in sector exposure between the normal S&P 500 and its equally weighted counterpart. Growth sectors like Information Technology and Communication Services are of significantly less importance in the EW version. Utilities and Real Estate, which account for less than 5% of the benchmark index, together comprise over 12% of the EW index – roughly the same weight as Tech.

That’s important because Utilities and Real Estate have been some of the absolute worst places to be this year. Check out how awful they’ve been – especially over the last few months. And the equally weighted index is way overweight!

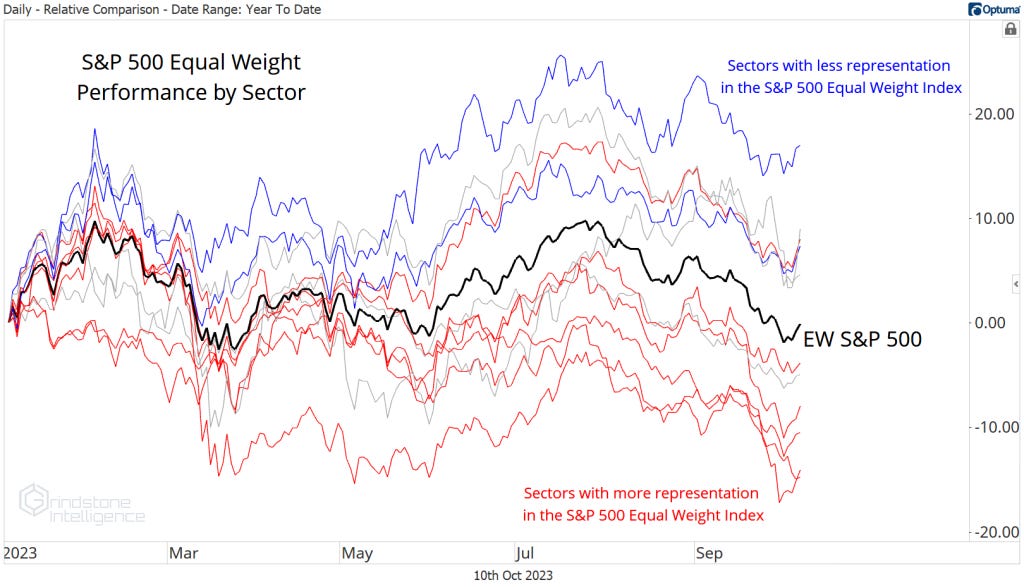

In fact, the equal weight S&P 500 is systematically underweight the best performing sectors and overweight the worst. Check it out:

In red are the sectors to which the EW index has materially more exposure than the cap weighted SPX. In blue are sectors that are underweighted. Nearly every overweight is lagging, and the underweights are leading. Note that these performances are for the equally weighted sectors, too, so we’ve removed the outsized impacts from the Magnificent 7.

It seems clear that things aren’t quite as bad as the equally weighted index makes them look. Market strength hasn’t been limited to just a handful of stocks. The equally weighted Tech (+17% this year), Energy (9%), Industrials (8%), Communications (7%), Discretionary (5%) sectors are all turning in respectable performances.

But things aren’t quite as good as the 13% gain implied by the SPX, either. Those mega caps do make a difference, and it’s particularly clear at the sector level.

Take Information Technology. Tech is the top performing equally weighted sector, with a healthy 17% gain for the year. But the cap weighted sector is up nearly 40%. And in Communication Services, the cap weighted surge of 45% far outpaces the (still respectable) 7% gain in the equally weighted sector.

The market cap impact shows up in the Financials, too, where the 4% year-to-date decline masks an even worse situation below the surface.

Small cap Financials are off a staggering 15% for the year.

If you’ve seen the underperformance of the Russell 2000 small cap index this year, that’s probably not surprising. What might surprise you, though, is that small cap underperformance isn’t a consistent theme. In 5 of the 11 sectors, small caps are outperforming large caps. The explanation for the Russell 2000’s underperformance can again be partially explained by sector exposure. Tech is a massive underweight in the small cap index, while underperforming areas like Financials and Real Estate are both large overweights.

So how’s the market doing this year? It depends.

Things aren’t quite as good as it might look on the surface. But they’re also not quite as bad as some might have you believe.

The post What’s Behind the Underperformance of the Average Stock? first appeared on Grindstone Intelligence.