The Only 3 Reasons to Buy a Stock

If you’re in the market to make money, there are really only 3 reasons to buy a stock.

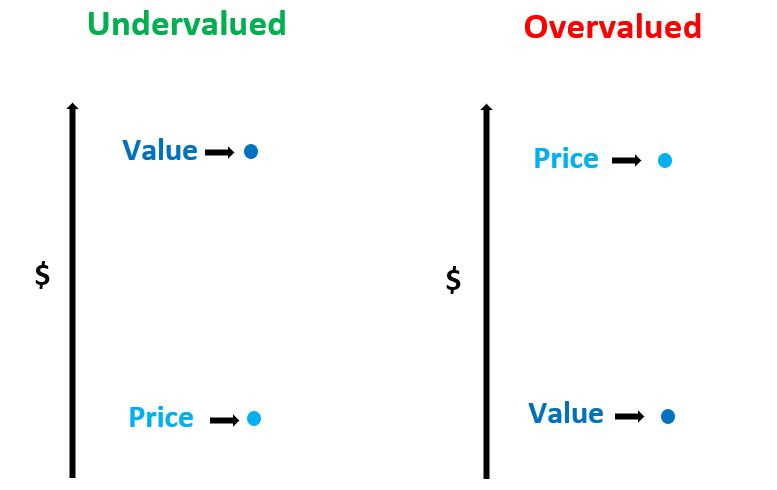

Reason #1: The Stock is Currently Undervalued: “The stock price is currently below the value of the business it represents.”

Defining ‘value’ can be a tricky thing. Intro to Finance 101 at any school in America teaches the value of any asset is equal to the sum of the present value of its future cash flows. Experienced market traders might quip that the value of something is whatever someone else will pay for it.

In the traditional sense of value investing, value is the price at which a company’s stock should trade. To discover value, an analyst tries to consider all available financial information, prospects for both macroeconomic and industry-specific growth, confidence in the management team, and countless other variables, weight each variable accordingly, and arrive at a number that represents the worth of the business in question. If the calculated worth is greater than the price at which a company’s stock price indicates, then the stock is ‘undervalued’. A worth below the indicated price, ‘overvalued’. Not exactly earth-shattering.

Unfortunately, calculating intrinsic value has a few glaring issues in practice.

First, there are countless variables to account for and limited information. Publicly traded companies are required to file detailed financial statements with the SEC, but even those can leave analysts with more questions than answers And analysts don’t just have to worry about business-specific information – external factors like economic growth trends, regulatory dynamics, and interest rates all impact the worth of a company. What’s more, the goal is to calculate what cash flows will be in the future. As if finding a value for all those variables wasn’t hard enough, now the analyst has to predict what each variable’s value will be.

That’s the second problem with valuation: we have limited foresight. For the sake of argument, let’s assume an analyst can reasonably estimate 5 years into the future for a given business. For 5 years ahead, he can put a number to all the variables and calculate cash flows. But anything beyond 5 years – the Horizon of Reasonable Predictability (HRP) – can’t be predicted with any degree of certainty. Still, value is supposed to include ALL of the future cash flows, not just those over the next 5 years. The analyst has to make predictions about something beyond the HRP, knowing full well that he’s just guessing. In the end, the most reasonable thing to do is choose the mid-point of a range of likely outcomes.

So perhaps the biggest problem with valuation is that no one actually knows what the correct value of anything is. Not with certainty, anyway. It’s entirely subjective to the estimates and opinions of the one calculating it. We could ask 1,000 people, all of them extremely qualified, to value the same business, and we’d get 1,000 different answers. At best, an average of those 1,000 answers might represent something close to a company’s true value. But here’s one more dynamic to consider: if you asked them all again a year later, the answers would be different. Valuation is a point-in-time calculation. As time progresses, uncertain things that were previously beyond the HRP become certain, and value changes.

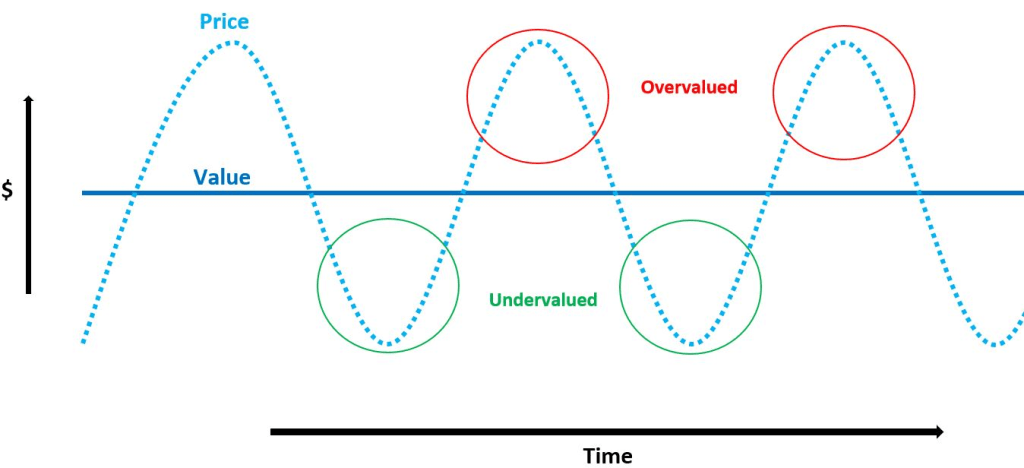

By now I hope it’s clear that even though the precise worth of a business exists, calculating it is virtually impossible. So how is it that legends like Benjamin Graham were able to generate superior investing results through a value investing approach? Because their goal wasn’t to precisely calculate the worth of a business. It was to buy undervalued stocks for the purpose of making money. For that they just needed a general idea of value. When the stock price differed significantly from that general idea, they took advantage by buying or selling, then waited until prices agreed.

On balance, it worked out well for them. Incredibly well. But before you rush off to become the next great investor, there’s a catch: it doesn’t always work. I’m not just saying that valuation is tricky, I’m saying the strategy itself has a flaw. That is, undervalued stocks don’t always go up. So even if you were the greatest analyst in the history of world, if you knew the value of a multi-billion dollar company to the last penny, none of it matters if the stock price doesn’t move towards value. There’s no rule saying it has to. Now, that’s not to say a value-based strategy can’t work. We saw it work for Graham, remember? Over time, stock prices do tend to move towards value. It’s just that over time, value changes!

If value stays constant or rises over time, the job is relatively easy. Buy when the stock is underpriced, sell when it’s overpriced. Retire.

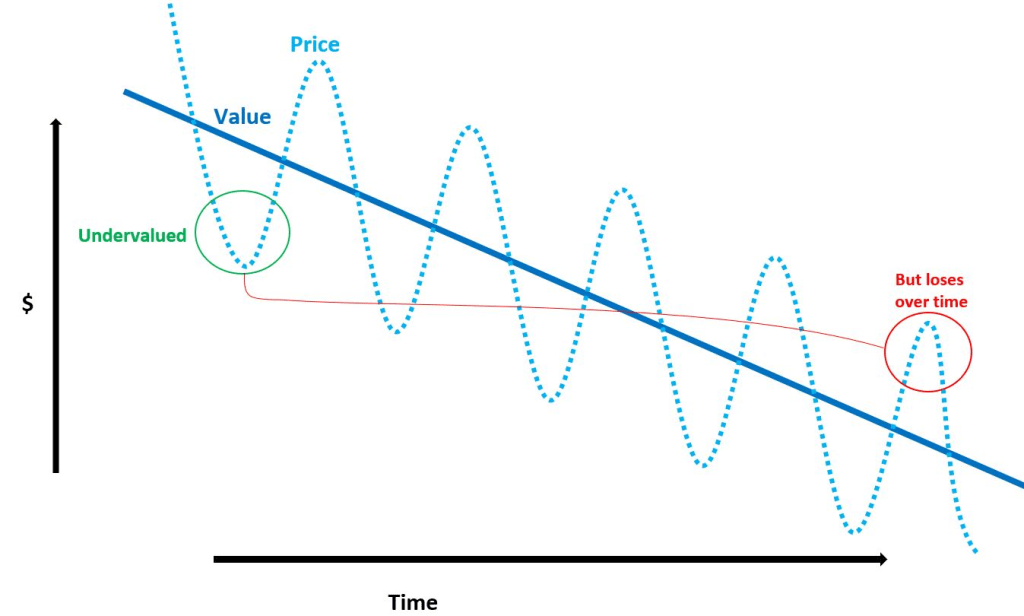

But what if value is trending lower? We can buy when the stock is undervalued, and if prices quickly move towards value, we still profit. But if price takes too long to correct, or if we hold the position for too long, the new value ends up below where we bought it.

If we choose not to sell and take the loss at that point, it’s either because we’re hoping the value will trend up in the future, or alternatively, betting the stock price will become overvalued. The former is unpredictable by its very definition (value already includes everything that can be reasonably predicted, and the change in value will be determined by something beyond the HRP), and the latter is the antithesis of a value investing strategy.

So in summary, Reason #1 for owning a stock has a proven track record of success (see Graham et al), but depends upon an accurate estimation of value and a stock price that converges towards that value quickly.

Reason #2: Long-Term Growth “This business will grow over the long-term, and the stock will grow with it.”

Several readers are already confused. Growth of the business? Isn’t that obviously included in the calculation of value, e.g. Reason #1? Well, yes and no. Growth is certainly part of the value framework. But Reason #2 differs in one key aspect: it’s focused on something beyond the Horizon of Reasonable Predictability. In other words, it’s a gamble on the trend in value.

I use the word gamble here for a reason. If it was anything less than a gamble, if the belief in long-term growth could be backed with evidence, then it would no longer be beyond the HRP. To the contrary, a belief backed by evidence is a very reasonable prediction, and thus would be included in value – and value investing was already covered by Reason #1. But Reason #2, making an investment based on unpredictable long-term growth, more closely resembles religious of faith: belief in that which cannot be proven. And that’s part of what makes investing for growth so compelling. Something which can’t be proven also can’t be disproven.

Another appeal of long-term growth investing is that it levels the playing field. The studious analyst has no advantage over the common man, because the difference between worth of the business and stock price is irrelevant. There’s no need to calculate value, because current price does not matter. It sounds blasphemous – after all, countless studies have shown expensive, so-called growth stocks underperform over the long-term. I won’t dispute the findings. But I counter that the problem for those so-called growth stocks was not that their price-to-earnings multiple was too big. No, the problem was that they failed to keep growing.

Let’s talk about a company named Amazon.com and the internet bubble of the late-1990s. If you didn’t experience the exuberance of the dot-com era first-hand, you’ve most likely heard all about it. Investors were so excited about the possibilities of this new technology that they were willing to pay exorbitant premiums for any stock name with a .com at the end. Like all bubbles, it ended poorly. Stock prices collapsed. Amazon.com was one of the highest flyers, rising 7100% less than two years after its May 1997 initial public offering. By December 1999, AMZN had a market capitalization of $36 billion. Meanwhile, their income statement for the year showed only $1.6B in revenue, and a whopping $700M in losses. The following year, they proceeded to lose twice that much.

Any cool-headed analyst could see the stock was overvalued at a price of more than 20 times their annual revenues. And when the bubble popped, the stock dropped a breath-taking 95%. But in the years since, Amazon.com has become a household staple. Since the turn of the century, they’ve grown revenues to more than a quarter trillion dollars – an annual rate of 29%. No one, and I mean no one, could have reasonably predicted that kind of growth. If you’d told someone in 1999 that a seller of used books would one day play such an all-important role in the U.S. economy, they’d have checked you in to the nearest mental hospital.

But what if you believed it? What if you focused only on the unknown growth possibilities, and you bought Amazon at the worst time, when it was most expensive, during one of the largest stock market bubbles in U.S. history? You’d have outperformed every major asset class on earth over the next 20 years – even after an initial collapse of 95%. In fact, with the benefit of hindsight, you should have been willing to pay much more! Ready for some stats? You could have paid double the peak 1999 price and still earned an annual 13.8% through September 2020. If your goal was to achieve historical U.S. equity returns of 10%, you could have paid four times more than Amazon’s peak 1999 price. And if instead you simply wanted to match the S&P 500 Total Return Index over that 20+ year period, you could have paid a 900% premium for AMZN on the day of the peak – or $301 billion dollars for a business with $1.6 billion in annual revenues. If a business grows fast enough for long enough, price doesn’t matter.

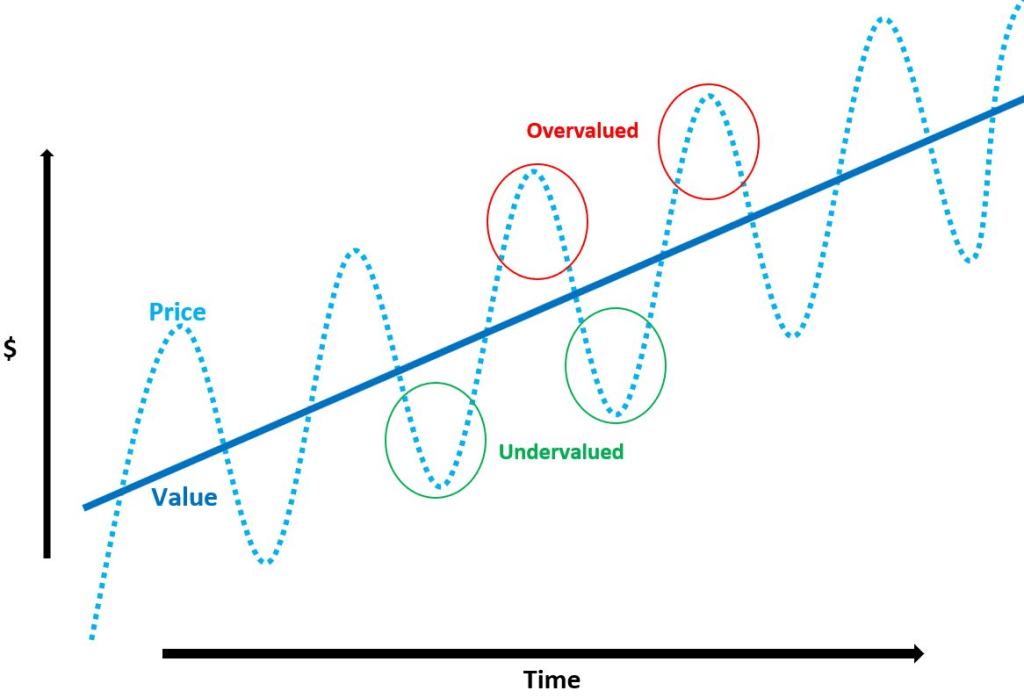

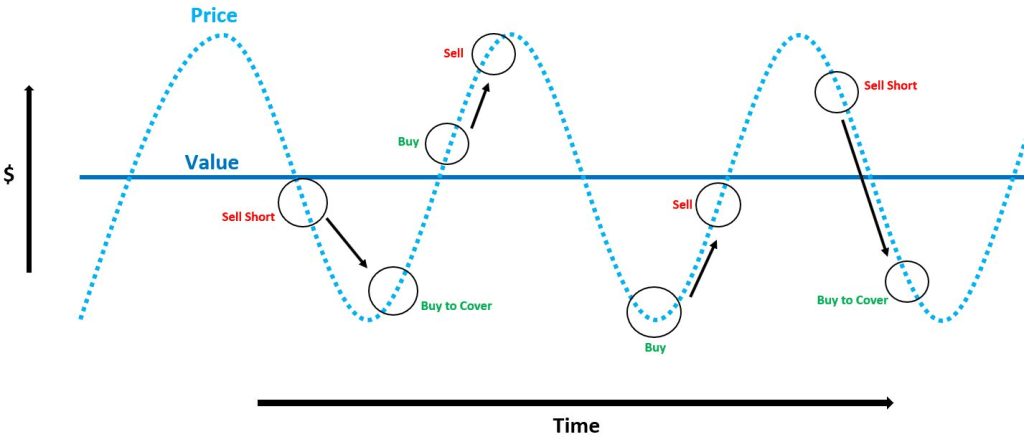

This investment rationale is a bet on the trend in value rather than the level of value, and the current price of the stock plays no role in the investing decision. To illustrate, let’s look at our value vs. price chart again, this time with value on the rise.

To be clear, expensive multiples don’t equate to great growth. The returns for other high-priced technology companies of the late 1990s, like Intel and Cisco, are far less compelling than those for Amazon. Some investors certainly believed those businesses would generate long-term growth at the time, but history has shown otherwise. Contrarily, General Electric could have been bought at low valuations at points during the late-1890s and early-1900s, but, still around 120 years later, clearly grew for longer than anyone could have reasonably expected. It’s not hard to place faith in the wrong deity.

Thus, the biggest problem with choosing a stock based on Reason #2 is that it’s a gamble on the unknown. The only thing separating one stock from another is our confidence level in something we can’t prove. We can’t know in advance whether we’ve chosen Amazon.com or Pets.com, and more often than not, we won’t know for many years, or even decades, if we guessed right.

Reason #3: The Catalyst – “I believe this stock is going higher”

The catalyst investing rationale is seemingly the most straightforward. It’s certainly the most simple to explain. The catalyst buyer is completely unconcerned with value of the business, long-term growth, or current price. He’s only concerned with which direction price will go over the relatively short-term.

Let’s use the price vs. value graphic once more to illustrate. The catalyst-focused investor doesn’t rely on the relationship between the two. At times the strategy may appear to align with a value approach, while at other times it seems to run directly counter.

The concept is simple, but the practice is less so. There is a limitless number of inputs to stock price changes. Catalysts, though, are often things that affect human behavior. And human behavior is what directs stock prices on a day to day basis.

It would not be possible to give a detailed explanation of the many areas of catalyst investing. It includes all forms of technical analysis – a wide ranging discipline that focuses on historical price trends and patterns – but also extends to various algorithmic trading strategies, and even headline chasing, among other things.

Making investment decisions guided by Reason #3 is often referred to as ‘trading’. The approach has a mixed reputation in the professional investing community, given a lack of research backing the usefulness of many approaches. It’s certain than many investors, professional or not, have gone bust trying to master the intricate art. But make no mistake, some of the most successful investors of all time have been ‘traders’.

What’s the point?

So now you’ve read about all three reasons to buy a stock. If you’re unfamiliar with the world of investing, these topics may have been new to you. If you’re an experienced investor, perhaps I just told you a bunch of things you already knew, and you feel like you’ve wasted you time. Maybe you did. But I think the process of slowly walking through your investment process and defining your strategy can help you make decisions that are logically consistent.

For instance, if you’re strictly a value investor, as defined earlier, do you consider yourself a short, long, or intermediate-term investor? I think many would define themselves as long-term, but we’ve seen that a longer holding period presents risks to value investing. In reality, the strategy is based on reversion to the mean, which more closely aligns with short and intermediate-term time-frames. So what do you do if price reverts to your estimate of value the day after you buy it? The logical thing to do is sell immediately – your undervalued thesis no longer applies – but the discomfort of incurring a short-term taxable gain or worse, looking like a ‘trader’ instead of a reputable value investor, can cloud a logical decision.

Or for the investor who focuses solely on long-term growth potential. Are you waiting for the next dip to buy? You may get a lower price, but if your belief is in long-term growth, current price matters very little. Your focus is years and decades ahead. If you believe value is rising over time, the last thing you want to do is spend time on the sideline. Waiting for a dip that may or may not come is contradictory to your own thesis.

What about the catalyst trader? Do you find yourself becoming emotional about gains or losses? The strategy is designed to take advantage of other investors’ emotional decisions. Allowing your own emotions to take over eliminates your advantage. Do you continue to hold your position after your original thesis proves wrong, hoping that you’ll get out even? A logical trader should want capital available for the next catalyst, not stuck in a position with nothing but hope for a thesis.

Among the worst things an investor can do is change their strategy to justify a losing position. Often the changed approach is not a conscious effort. It comes about by not having a clear understanding of your own approach. For the value investor who watched the value of the business decline before prices rose to his initial estimate, believing that value will reverse course. For the growth believer who turned out to be wrong, pointing out that the stock is underpriced. And for the catalyst investor, reading up on financial statements after a stock is purchased.

Of course, that doesn’t mean your strategy must be restricted to only one of the three above. They aren’t mutually exclusive. Some guy named Warren Buffett once said, “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.” Buffett is called value investor, but he doesn’t focus on value alone. He targets good companies – those that will grow for a long time – and tries to buy them at good prices. He combines Reasons 1 and 2, while ignoring 3. Alternatively, many investors use catalyst investing to complement their focus on value. Successfully timing the market mitigates the term risk associated with a value-only approach. But those strategies are defined before a stock is bought, not after.

Catching the bottom of an undervalued stock, with an underlying business that will grow for a long time is the holy trinity of investing. That doesn’t mean you need the whole triumvirate to be successful, though. You just need a mastery one of the three. What’s most important is understanding who you are as an investor and defining your process. Doing that will help you avoid the fatal flaw of allowing emotions to change your strategy.

The post The Only 3 Reasons to Buy a Stock first appeared on Grindstone Intelligence.