Will Home Prices Ever Come Back Down?

The National Association of Realtors’ Housing Affordability Index is cratering.

You’ve more than likely seen this chart before, but even if you haven’t, there’s a good chance you’re feeling the effects anyway. Whether you’re a first time buyer, upgrading to accommodate a larger family, relocating for work, or just looking for a change in scenery, it’s rarely been more expensive for Americans to buy a home.

The problems aren’t hard to identify. The first is the most obvious: home price increases have accelerated.

From 2013-2019, the Case-Shiller National Home Price Index rose at a steady rate of 5-6% per year. In 2021 and 2022, though, those gains surged to 20% per year. And even though home prices have stabilized over the last year, they’re still 20% above what would have been expected if home values had continued at their prior pace.

So what was behind the surge in prices? The same thing that always drives price changes: a mismatch between supply and demand.

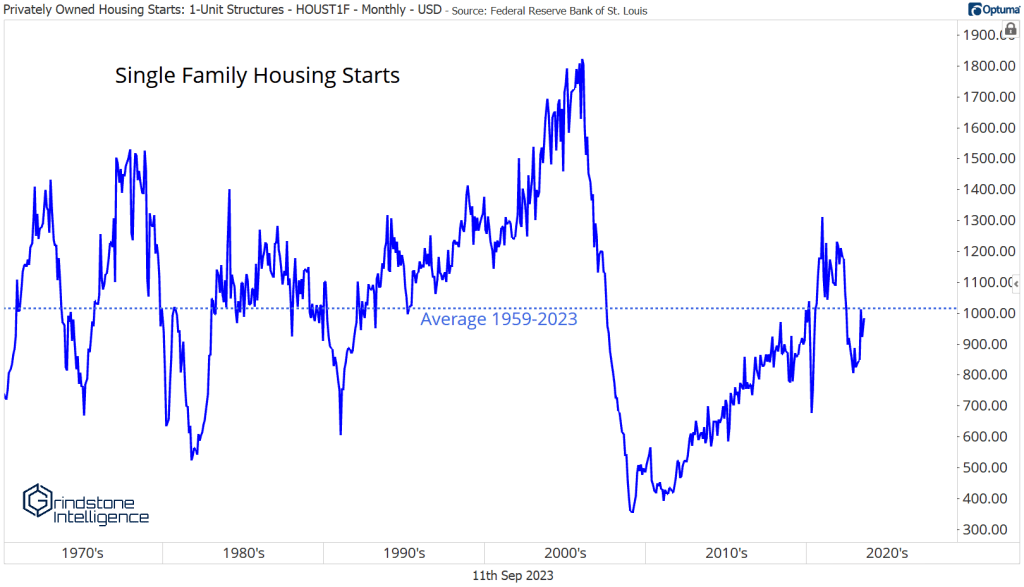

After the housing bust of the mid-2000s, the industry changed on a lot of levels. Obviously, the availability of credit dried up. Banks started requiring people to actually have jobs and income to qualify for a mortgage. But homebuilding dynamics changed, too.

Builders and their suppliers were brought to the brink of destruction. Many of them went belly up.

Just like US oil producers following the energy collapse of 2014, the builders that survived were forced to change the way they operated – they bought fewer lots, built fewer spec homes, and tightly controlled their inventory levels. As a result, the US single-family housing starts have been below average for most of the last 15 years.

The supply/demand mismatch was exacerbated by COVID.

Millennials have notoriously postponed marriage and children until later in life compared to previous generations. But in the late 2010s, household formation picked up in the nation’s most populous adult demographic cohort, evidenced by growth in owner-occupier households outpacing that of renter households. The coronavirus and the work-from-home movement that accompanied it were like gasoline on a fire.

Demand surged.

At the same time, supply chain and labor disruptions cut off the supply of new homes. Cycle times – the time it takes to complete a home after breaking ground – extended by 6 months during 2021 and 2022, because builders couldn’t get the necessary materials, equipment, or appliances to finish and deliver homes.

What did the publicly traded builders do? They intentionally slowed the pace of sales. They stopped making homes available for sale until they were at or near completion, as opposed to when the lot was available. They stopped giving incentives altogether. They stopped taking new orders.

With supply crimped, home prices skyrocketed.

Build times have started to improve in recent months, though, according to industry executives. That’s a good sign for homebuyers, if it means builders can complete and deliver new homes.

Unfortunately, new home supplies are just one piece of the puzzle.

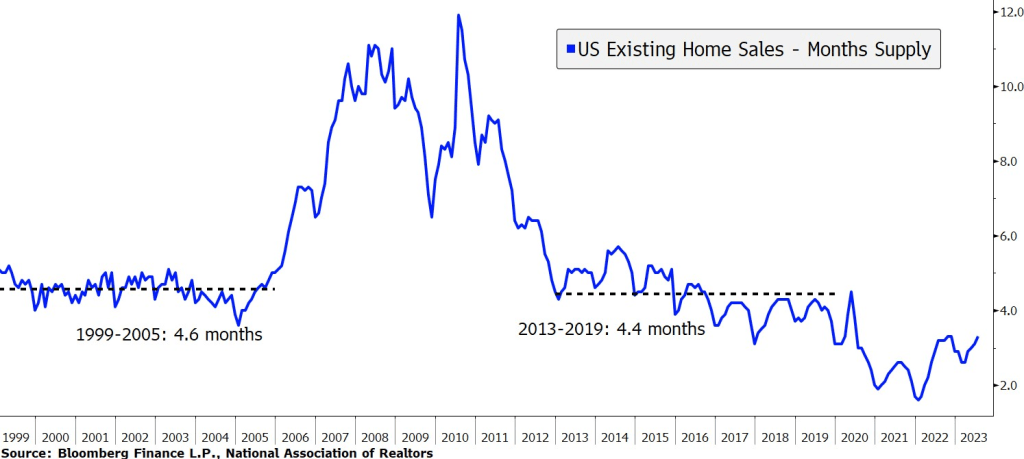

The vast majority of home sales in the US are for existing homes, and existing home inventories are still well below average. There are 3.5 months supply of existing homes today. That’s better than the sub-2 reading at the height of the crisis, but still below the 4.5 months that was associated with ‘healthy’ housing markets from 1995-2005 and 2013-2019.

What’s worse, the recent uptick in months supply is a result of slowing sales, not rising inventory levels. The number of existing homes in inventory is still at multi-decade lows.

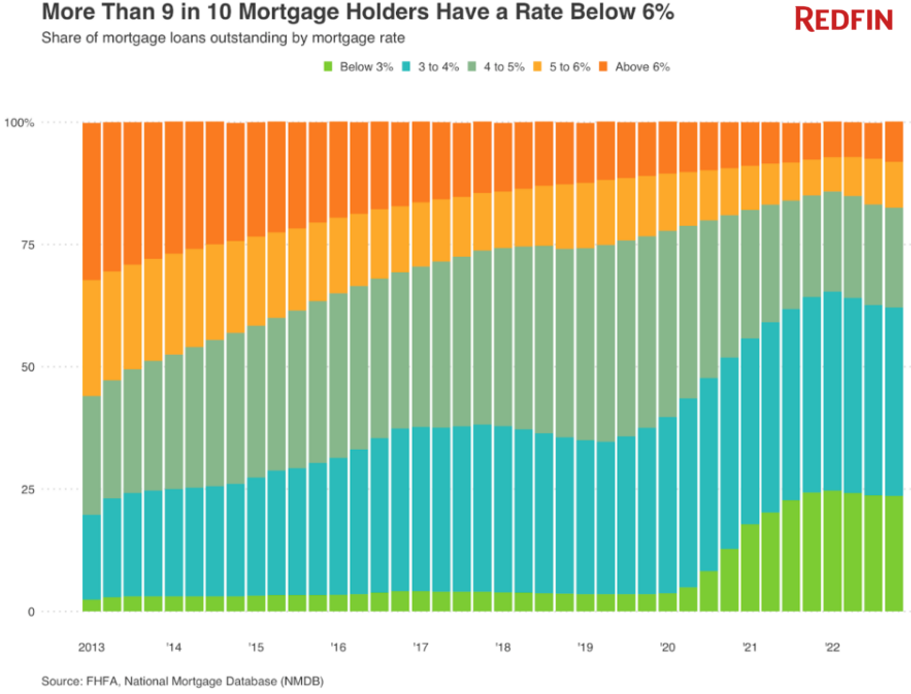

Why aren’t people selling homes like they used to? Because most of them would have to be a bit crazy to leave.

Since the Federal Reserve embarked on its fight against inflation last year, the average 30-year mortgage rate has climbed from less than 3% to more than 7%. That’s made it prohibitively expensive both for first time buyers and anyone looking to move.

On a similarly priced home, the higher interest rate equates to a whopping 60% increase in the monthly mortgage payment (and don’t forget home prices have gone up since then, too).

According to Redfin, more than half of mortgage holders have locked in rates of less than 4%. Nine in 10 have rates below 6%. That makes moving a rather unaffordable prospect.

That means lower mortgage rates could solve both the affordability and the existing home supply problem. Or would it? Shifts in mortgage rates historically have had only a muted impact on home prices. The chart below takes the monthly mortgage payment implied by current home prices and mortgage rates, then applies that same payment at different interest rates to find a ‘rate-adjusted home price’.

For example, if you took the mortgage payment on a new home today and applied it towards a loan with a 2% rate, you could afford at $786,000 home.

But home prices don’t respond like that to changes in interest rates. If they did, the thin blue lines would progress smoothly higher, while the thick line would jump around with interest rate changes. The opposite has been true.

So will home prices ever come back down? The short answer is, probably not. At least not by enough to alter the affordability landscape. Our crystal ball is murky as ever, so we can’t rule out the possibility, but history is not on the side of significant declines in home prices.

New home prices have rarely dropped more than 5% from their peak over the the last 60 years, with a maximum decline of 13% during the Great Financial Crisis.

The record for existing home prices is a bit more palatable – the Case-Shiller Home Price Index fell 25% during the GFC. But even that pales in comparison to the aforementioned 60% rise in monthly mortgage costs from rising rates. It could be years before housing affordability returns to where it was a few years ago – if it ever does.

On the bright side (if there is one?), rental rates could be set to fall as the supply of rental units surges. The number of structures 5-units or more under construction is at record highs:

*Editor’s note: In the original version of this post, we incorrectly stated that the Housing Affordability Index was at all-time lows. The index was actually lower in the early 1980s, when mortgage rates were much higher than they are now.

The post Will Home Prices Ever Come Back Down? first appeared on Grindstone Intelligence.