Materials: Mining, Metals, and Mixed Signals

Materials joined the list of sectors setting new highs last week, after spending the last six months stuck below peak levels set in May.

The breakout was led by Chemicals, an industry which makes up 69% of the sector. Chem consolidated healthily above the 161.8% extension from the 2018-2020 decline, with the area near $800 acting as a base throughout the summer. The next extension is up near $1080, and the May highs should act as near-term support on any pullback.

Construction Materials looks similar, having broken out above the the first extension from the COVID selloff after several months of consolidation.

The Metals & Mining industry is still well off peak levels from earlier this year, but has joined in the recent rally and is nearing an incremental high.

The Miners tend to trade closely with the commodities they produce, and this particular industry is heavily influenced by the prices of copper, steel, and gold. Copper and steel prices surged throughout much of 2020 and 2021, but have stabilized in recent months.

As they’ve consolidated, precious metals have started to strengthen. Relative to Base Metals, Precious Metals surged back above the 2018 lows that were broken in late summer.

False breakdowns like these can set the stage for major trend reversals. So are precious metals poised to lead going forward?

Perhaps. Gold just put together its best 2-week stretch in over a year, and has been setting higher lows since the spring.

Longer term, the yellow metal has struggled to digest the former highs set in 2011 and 2012. If prices manage to resolve higher from here, a decade-long base could help drive a substantial move higher.

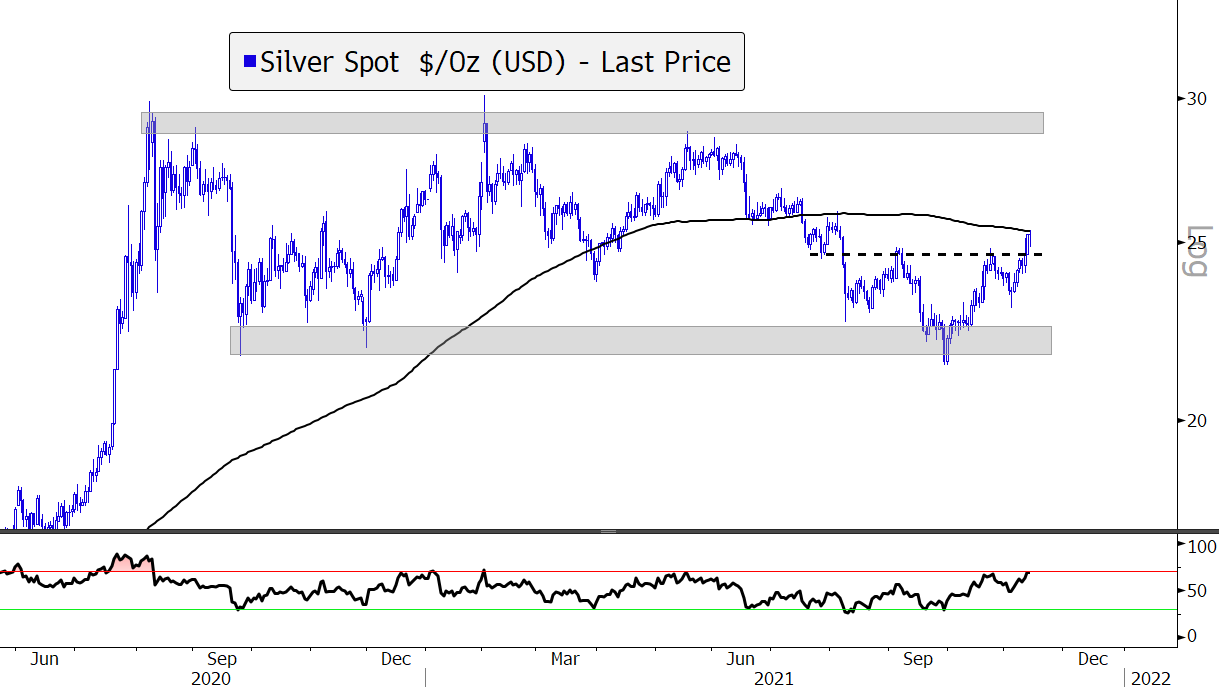

Silver has been messy for the last year, too, but has rallied since a failed breakdown at the end of September. I try not to put too much faith in traditional chart ‘patterns’, yet the reverse head-and-shoulders pattern that set up over the last quarter couldn’t get much cleaner.

If Gold and Silver both gain momentum, Precious Metals could do more than just outperform their Base counterparts. They could outperform equities. Relative to the S&P 500, Precious Metals broke their 2018 lows earlier this year and are solidly in a downtrend. Yet momentum failed to get oversold on the most recent selloff. Should the current rally continue, a momentum divergence could quickly snowball into a false breakdown and a ratio back above its 200-day moving average.

To be sure, Precious Metals are still in a well-defined downtrend vs. equites. But if a reversal ever comes, it has to start somewhere.

The biggest headwind to outperformance by metals could be from currencies. Commodity prices and relative strength in Materials tend to be negatively correlated with changes in the U.S. Dollar, but, oddly enough, recent strength in metals has coincided with a breakout in the U.S. Dollar Index:

So will the Dollar’s strength put an end to leadership from the Materials space? Will the currency reverse lower? Or can the two buck their historical relationship and rally together?

Nothing in this post or on this site is intended as a recommendation or an offer to buy or sell securities. Posts on Means to a Trend are meant for informational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in posts. Please see my Disclosure page for more information.

The post Materials: Mining, Metals, and Mixed Signals first appeared on Grindstone Intelligence.