Rates are on the Rise

With stocks under pressure to start the year, bonds haven’t gotten the bid you might expect to see during a market selloff. In fact, we’ve seen the opposite: rates are on the rise.

Shorter-term issues are leading the way. Since setting a low in the summer of 2020, U.S. 5 year Treasury yields have trended steadily higher and have now completely erased the QE-driven decline following the onset of the COVID-induced recession. On Friday, they (barely) closed at their highest level since the middle of 2019.

Ten year Treasuries peaked in the spring of 2021 following their own rally off the pandemic lows. But after 8 months of consolidation, they’re breaking out to new 52-week highs.

The move at the long end of the curve has been less pronounced. Just two-months ago, 30 year Treasury yields were breaking down from a consolidation range, and it looked like the 40-year bull market in bonds was about to resume. But that move turned out to be a head fake – 30s are now breaking to the upside. Still, long-term rates are well below pre-pandemic levels and their 2021 highs.

The result of relatively muted moves on longer-dated maturities is a yield curve that’s flattened considerably. Since the end of March, 2021, the spread between 30 and 5 year Treasuries has contracted by more than 100 basis points.

Of course, the world looks quite a bit different than it did last March. Back then, the Federal Reserve was still confident that inflation would be transitory, and their median expectation was for core PCE to fall to 2.2% by year-end. Instead, the reading for December came in at 4.9%. The surprising persistence of price pressures has forced those same Fed members to plan for a rate hike as soon as next month, when less than a year ago the median expectation was for rates to remain at zero until at least 2024.

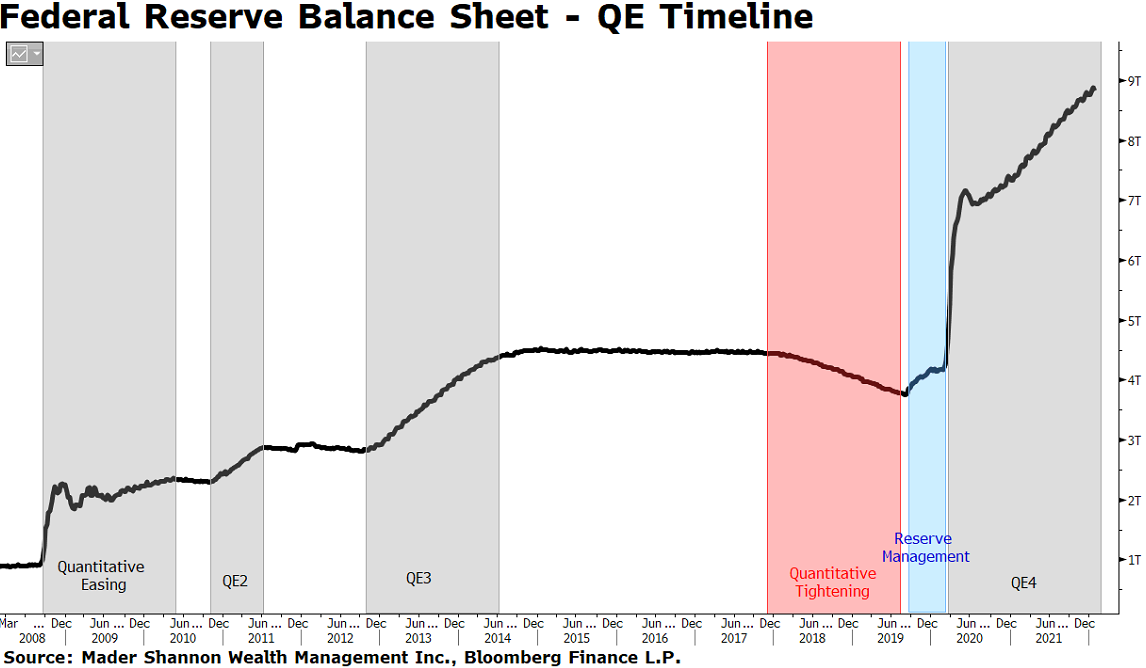

With the increasing likelihood of higher overnight rates from the Fed, it’s unsurprising that shorter-term yields have risen, but why have long-term yields failed to participate? Perhaps it’s because the Fed, despite its increasingly hawkish tone, is still buying $20 billion of Treasury securities this month, and $10 billion in mortgage-backed securities, as part of its ongoing quantitative easing plan.

QE4 is set to expire in March. We’ll see then whether Fed purchases have been artificially holding down long-term yields.

It’s not just Fed members who’ve been forced to change their tone. Christine Lagarde, head of the European Central bank, took eurozone 2021 rate-hike expectations from “No” to “Maybe” in her post-meeting press conference last week. German 10 year rates responded by jumping 25 basis points and rising above zero for the first time in nearly 3 years.

Italian government bonds, which are decidedly more at-risk of default than their German counterparts, saw yields spike even more, nearly 50 bps for the week. That’s the biggest weekly jump since the March 2020 meltdown.

That normalization in credit spreads between European government issues has been mirrored in the U.S. corporate market. Last week, high yield spreads reached the highest levels we’ve seen in a year. Yet even now, credit costs are cheaper than at almost any time in 2019, before the pandemic hit.

Bear markets tend to coincide with recessions, and recessions tend to be the result of credit crunches. Judged on current credit spreads, this equity selloff seems to be a run-of-the-mill correction within a longer-term bull market. But if this decline is instead a pre-cursor to economic weakness, expect high yield bonds to come under more pressure than they’ve gotten so far.

Nothing in this post or on this site is intended as a recommendation or an offer to buy or sell securities. Posts on Means to a Trend are meant for informational and entertainment purposes only. I or my affiliates may hold positions in securities mentioned in posts. Please see my Disclosure page for more information.

The post Rates are on the Rise first appeared on Grindstone Intelligence.