Sector Ratings and Model Portfolio Update - 1/4/2024

The Grindstone Intelligence Sector Ratings are based on our top-down technical approach. We assess the relative strength and trends within each sector and gauge risk appetite in the broader market to determine which sectors we think are best positioned to lead going forward. The ratings below reflect our views over the coming month.

The US Equity Model Portfolio is a hypothetical allocation designed to align with our Sector Ratings. The positions are chosen with investment horizons ranging from one to several months. The Model chooses only funds that track sectors, industries, or categories of stocks - no individual stocks or cash positions are used. Changes to the model will be communicated via email to subscribers and posted on our site.

A leadership change is at hand.

We’ve been sharing the chart below quite a bit over the last few weeks, and for good reason. Growth stocks were all the rage in 2023, and with mega-cap growth driving the boat, it was a tough year for stock-pickers to outperform. With the growth/value ratio finding resistance at a familiar level - the same place it peaked back in 2020 and 2021 - the stage is set for a regime change.

How long this new regime lasts is anyone’s guess, but for now, it’s clear that we need to be leaning away from growth until further notice.

Where should we be focusing our efforts instead? How about Health Care? Relative to the S&P 500, Health Care was setting multi-year lows on December 18th. Since then, it’s been the best sector in the index.

That bottom in the Health Care/S&P 500 ratio occurred at the exact same place it did back in 2021, and momentum put in a massive bullish divergence to boot. This could just be a mean reversion or it could be the start of a new, long-term uptrend. In any case, we don’t want to be betting against Health Care stocks.

The same goes for the Consumer Staples. We’re looking at a failed breakdown vs. the rest of the market, with momentum failing to reach oversold territory on the last move lower. At the very least, we should expect the Staples to track with the market over the next month or two. The more likely outcome is a reversion towards the 200-day moving average.

We’re still skeptical of the Energy sector, despite increased geopolitical turmoil that’s sparked significant (though often short-lived) rallies in oil prices over the past few weeks. Unless the Energy/SPX ratio is convincingly back above the summer-2023 lows, we prefer to bet on further underperformance from Energy stocks.

By definition, the Real Estate sector has completed its mean reversion relative to the rest of the market. The Real Estate/SPX ratio rallied back to the 200-day average (the mean) and now it’s stalled out, with momentum falling sharply over the past few weeks. The higher likelihood now is a resumption of the downtrend that’s been in place since early 2022, so we’re maintaining our Underweight rating on the sector.

Here’s a complete look at our current ratings:

As a result of the changes to our sector ratings, we’re making the following changes to our Model Portfolio.

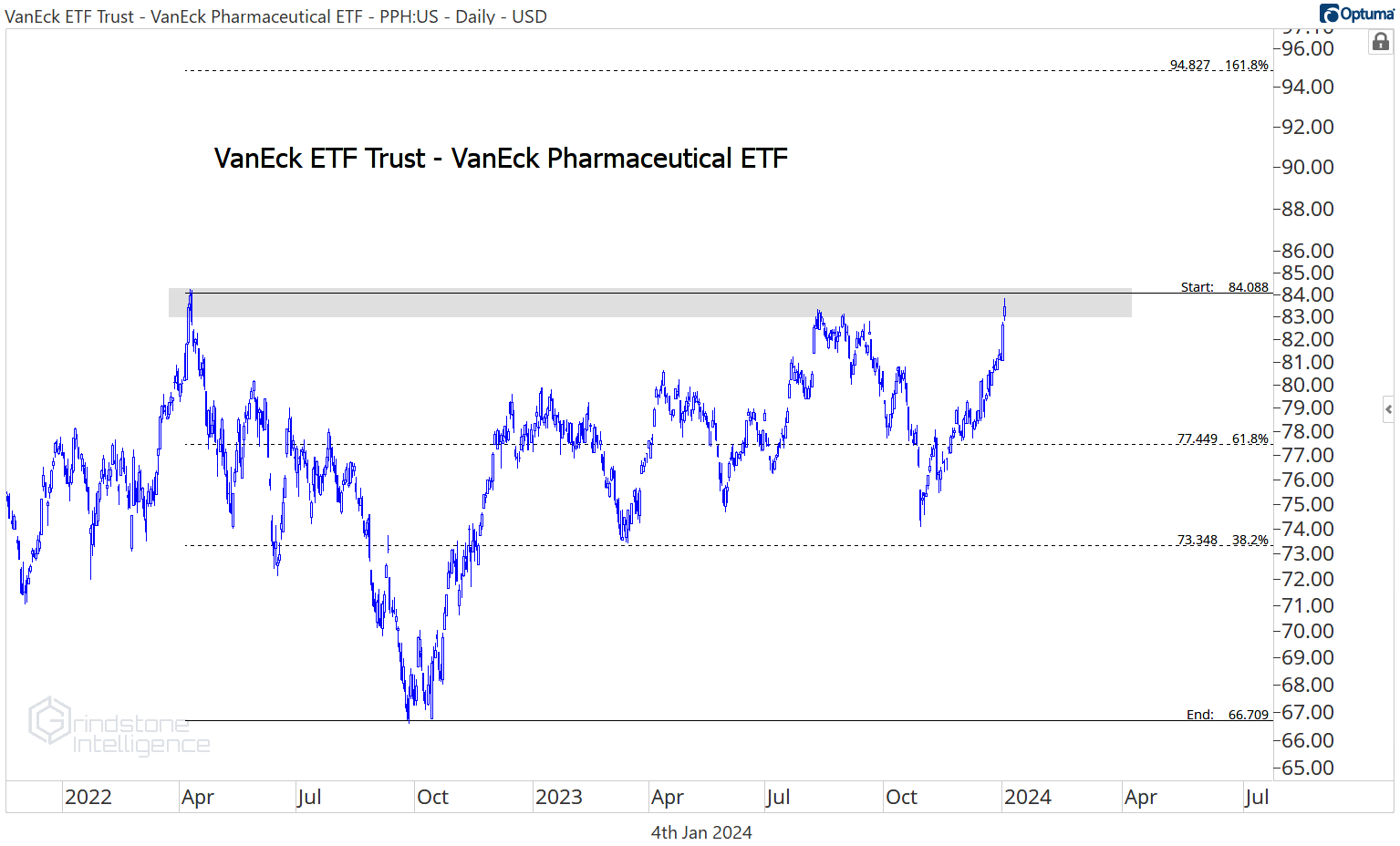

We’re adding the Vaneck Pharmaceutical ETF to reflect our Health Care sector upgrade. PPH just set new 52-week highs and is on the verge of a multi-year breakout. If the sector is going to outperform over the next few months, there’s a good chance PPH leads the way. We’re targeting $95.

We’re also boosting our position in IAK, the iShares Insurance Fund. Insurance was one of the best non-growth places to be in 2023, and we think that relative strength is set to continue this year. Especially if the Financials are a leading sector. The target on IAK is $130.

That’s all for today. Until next time.

hello Austin can u check my suscription ? there is problem i wrote to you but u don t see it i think

regards