The Case for Small Caps - 12/14/2023

It's a growth vs. value story

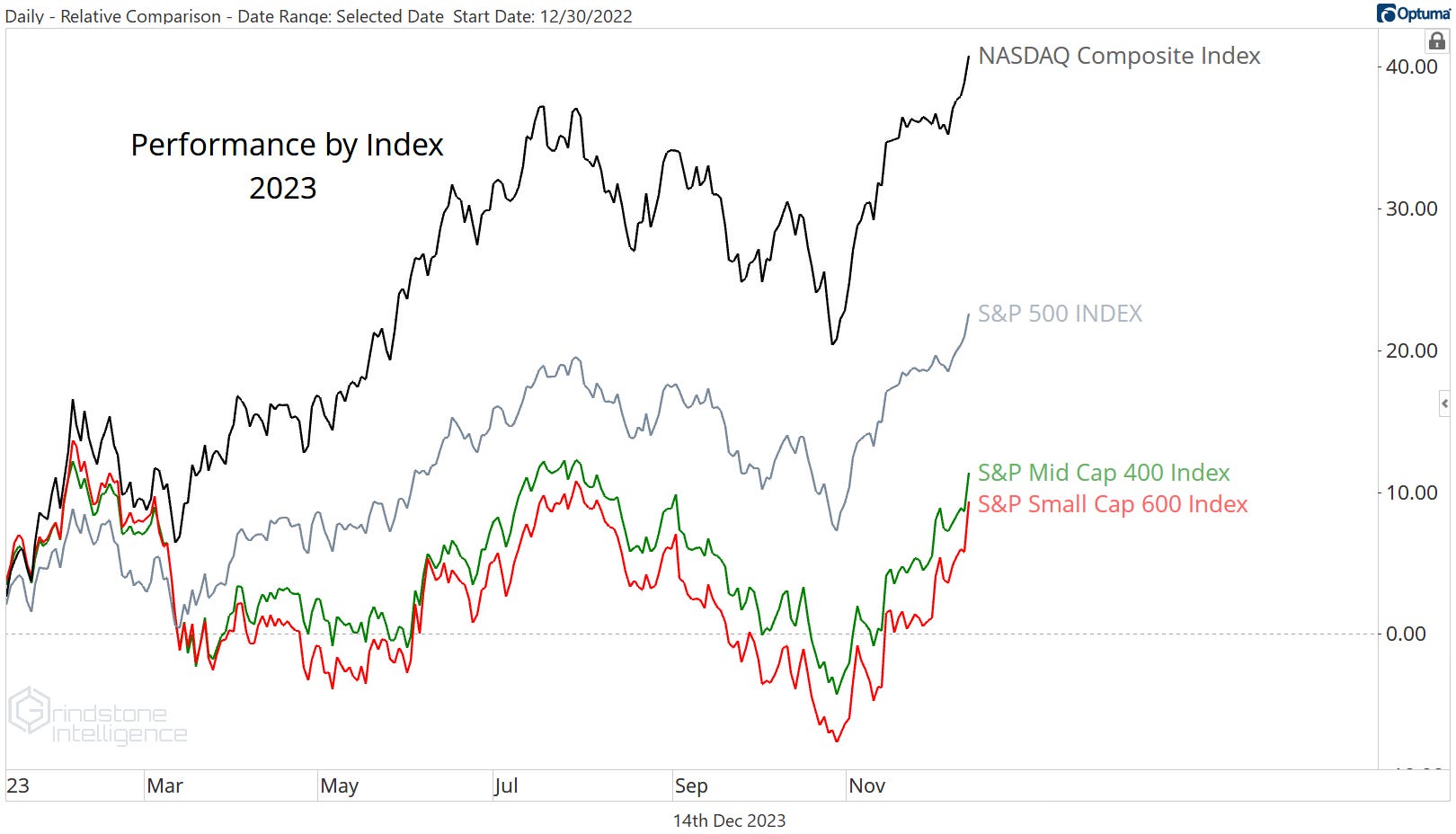

One great recipe for underperforming in 2023 has been to invest in the small caps. Despite an 18% rally from their October lows, the small caps are up less than 10% for the year. The S&P 500 index, meanwhile, has risen nearly 25%, and the NASDAQ Composite is up more than 40%.

It’s an interesting shift from last year. The small caps were the first to bottom in 2022, setting their lows in the early part of the summer, whereas the large cap indexes kept dropping until the fall. But while the large caps have rallied in 2023 and are approaching new all-time highs, the Russell 2000 small caps remain rangebound closer to their lows.

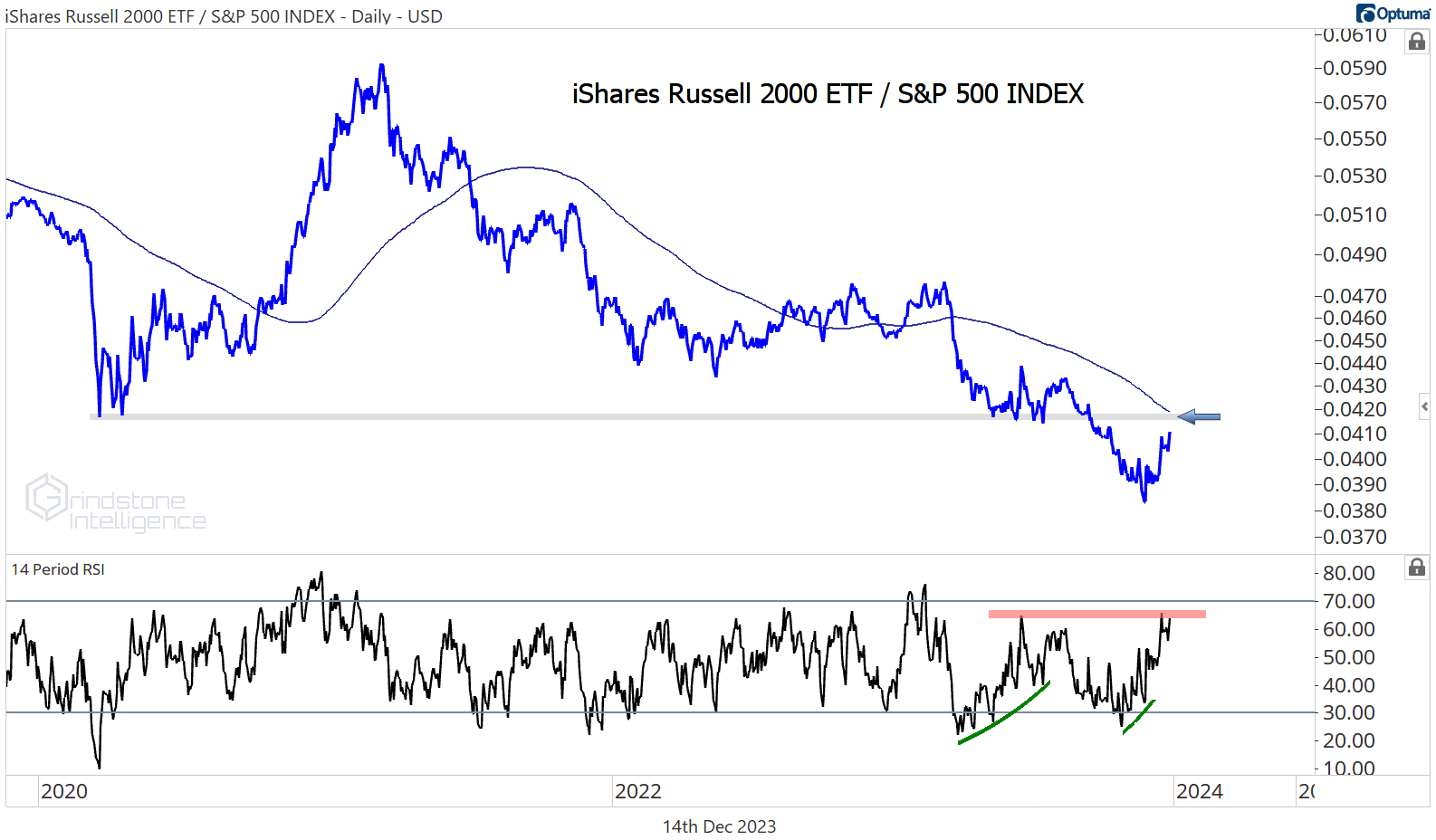

The lack of participation drove small caps to new lows relative to the S&P 500. A bullish momentum divergence for the ratio at the 2020 lows set the stage for a potential reversal, but bulls weren’t able to take advantage. Now we’ve got another momentum divergence shaping up, but we haven’t yet seen confirmation. As long as the small cap to large cap ratio is stuck below those 2020 lows and momentum is stuck in a bearish range, the higher likelihood here is that large caps will continue to lead.

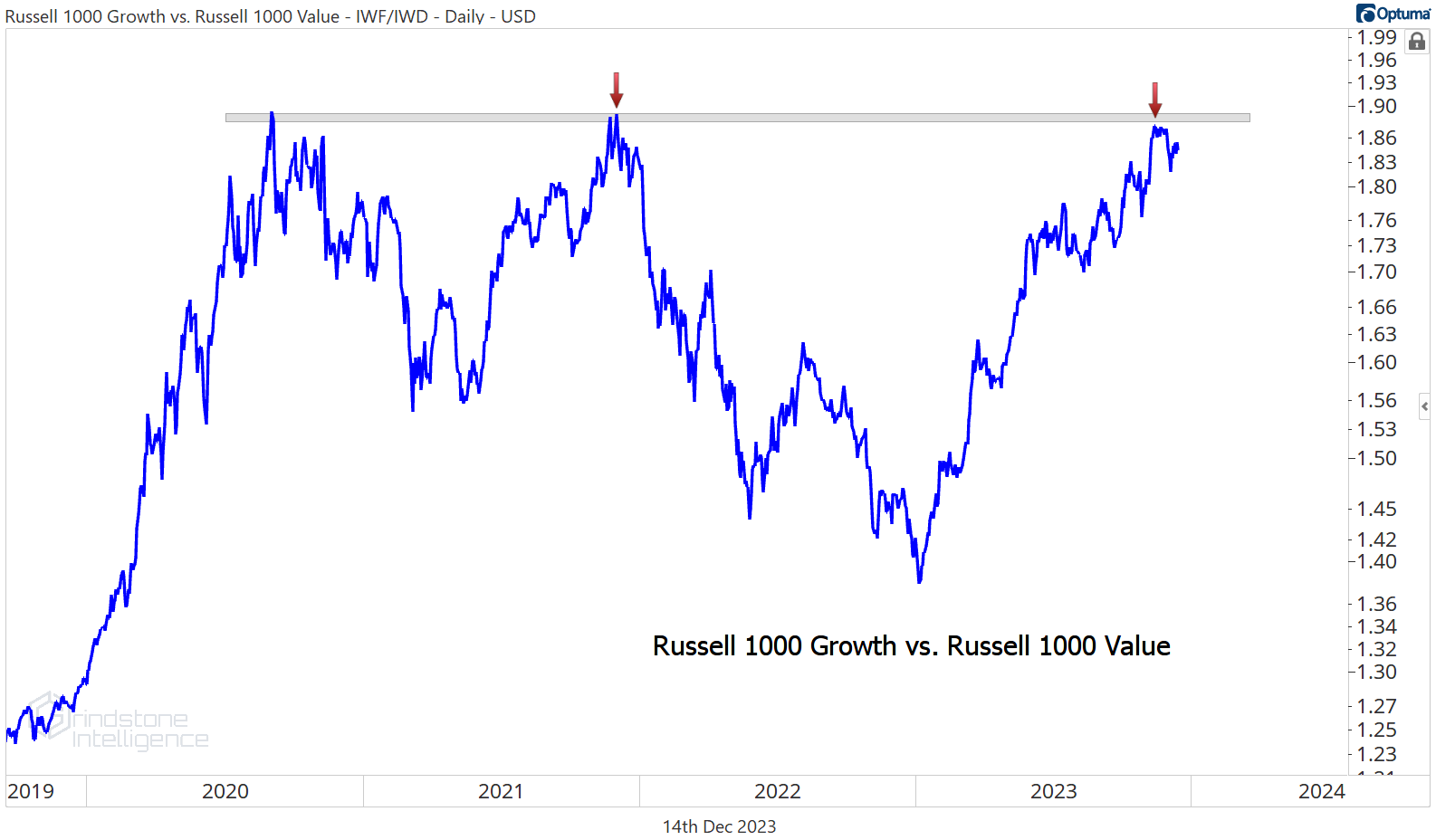

The Russell 2000’s underperformance this year isn’t really a ‘small cap vs. large cap’ thing. It’s really a story about growth vs. value. Since January, Growth stocks have outperformed Value by 35%, fully erasing the move in 2022.

And check out the differences in sector exposure between the large caps and the small caps. Tech and Communications (growth-oriented sectors) are both massive underweights in the small cap index, while underperforming areas like Financials, Real Estate, and Energy (value-oriented sectors) are large overweights.

Don’t get me wrong, large cap Tech is definitely outperforming small cap Tech. The small cap sector broke down to new relative lows vs. the big boys.

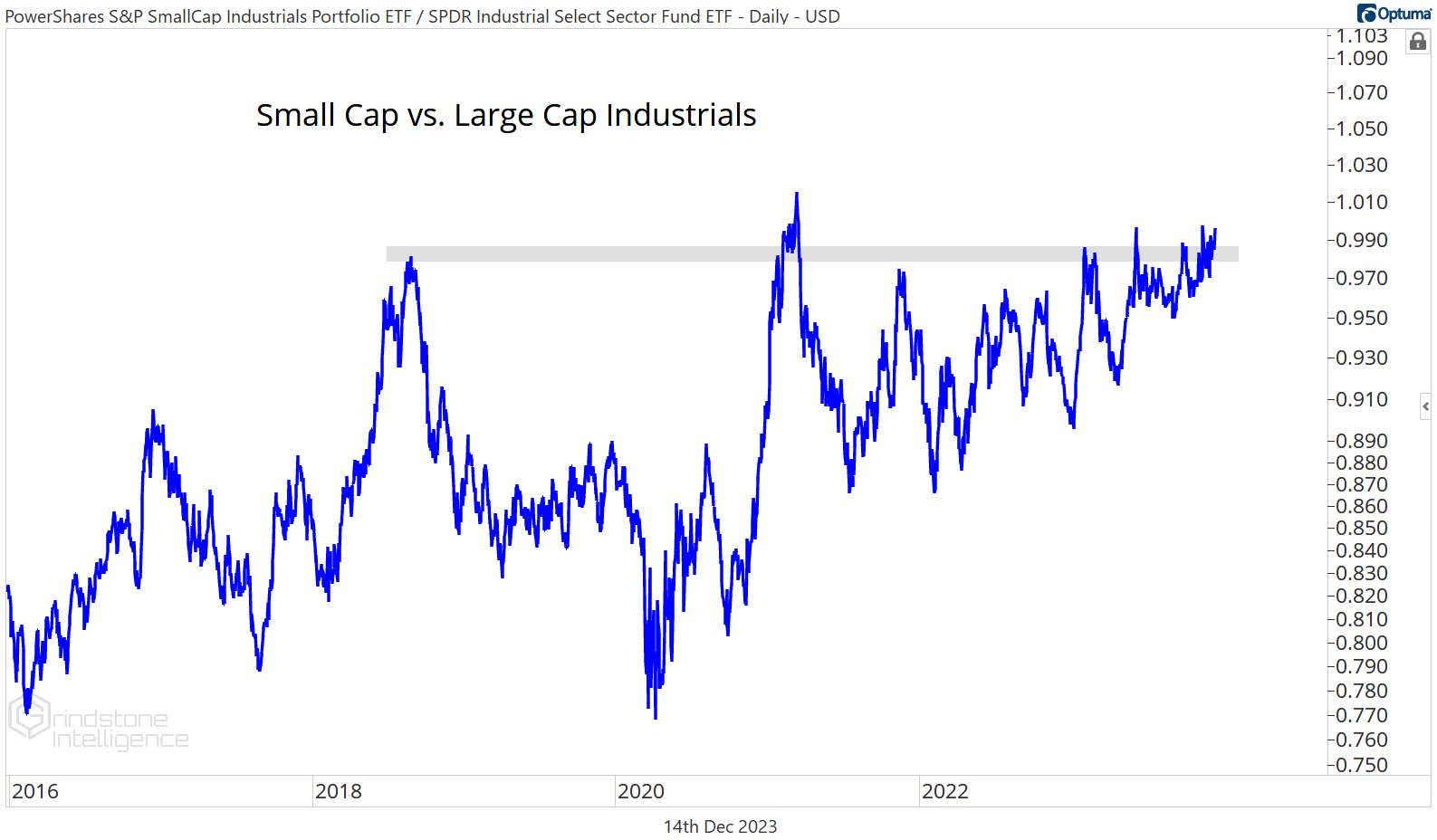

But if the theme was ‘all small caps are lagging’, small cap industrials probably wouldn’t be breaking out of a 5-year base relative to the large cap sector.

Here’s that small cap group on their own breaking out to new all-time highs. You can’t say that about too many large cap sectors. We think they’ll keep going all the way to $120.

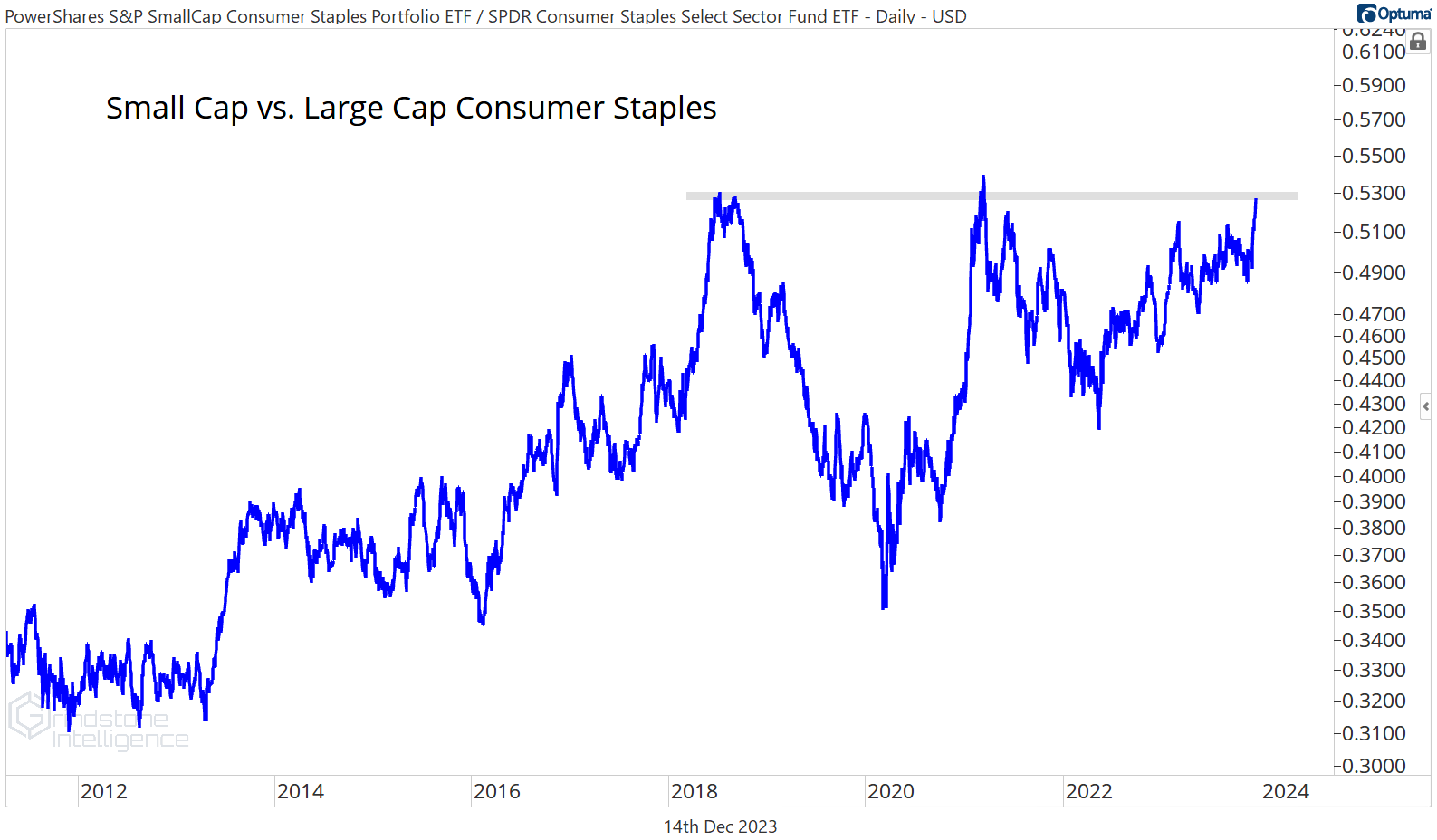

In the same vein, check out the small cap Consumer Staples. They’re threatening to break out of a big base vs. the large cap sector, too. That surely doesn’t fit with ‘all small caps are bad.’

So if we want to see the small cap indexes start outperforming, what we really need to watch are the value sectors. We already know how much strength lies beneath the surface in the Industrials. But what about the Financials?

They’ve been a big laggard in 2023, thanks in large part to declines during the March banking scare. But now, the small cap sector is breaking out to 9-month highs. That completes the trend reversal that began with a failed breakdown in October.

And with another 35% before the small cap Financials challenge their all-time highs, there’s plenty of room for further gains. Should value fall back into favor in 2024, we’ll be giving this area a lot more attention.

That’s all for today. Until next time.