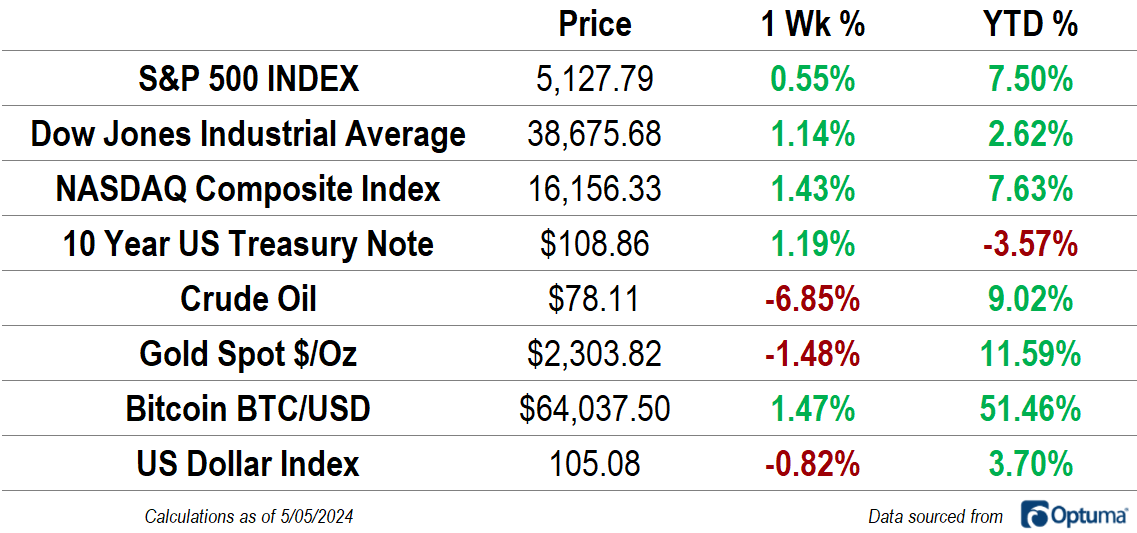

The Morning Grind - 5/6/2024

Longer than previously expected

Rate cuts? Not so fast

Last week, the Federal Reserve kept interest rates unchanged, citing the disappointment of higher-than-expected inflation readings throughout the first quarter. At Fed Chair Jerome Powell’s post-FOMC meeting press conference, his message was clear: interest rates are going to be higher for longer. Here’s a clip from Powell’s opening remarks:

“We've stated that we do not expect that it will be appropriate to reduce the target range for the federal funds rate until we have gained greater confidence that inflation is moving sustainably toward two percent. So far this year, the data have not given us that greater confidence. In particular, and as I noted earlier, readings on inflation have come in above expectations. It is likely that gaining such greater confidence will take longer than previously expected. We are prepared to maintain the current target range for the federal funds rate for as long as appropriate. We're also prepared to respond to an unexpected weakening in the labor market.”

Powell went on to repeat some variation of “longer than previously expected” four more times during the Q&A portion of the press conference.

“We didn't see progress in the first quarter, and I've said it appears then that it's going to take longer for us to reach that point of confidence. So I don't know how long it'll take.”

“We see three inflation readings, and so I think you're at a point there where you should take some signal. We don't like to react to one or two months' data, but this is a full quarter, and I think it's appropriate to take signal now, and we are taking signal. And the signal that we're taking is that it's likely to take longer for us to gain confidence that we are on a sustainable path down to 2 percent inflation.”

“We didn't gain confidence and it's going to take longer to get that confidence”

“We've said that we didn't think it'd be appropriate to cut until we were more confident, that inflation was moving sustainably down to 2 percent. We didn't get - our confidence in that didn't increase in the first quarter and, in fact, what really happened was we came to the view that it will take longer to get that confidence.

We’ve written in the past about the importance of forward guidance in Fed policy making. It’s not what the Fed does, so much as it is what they say. And right now the Fed is saying that rate cuts are off the table until further notice.

No Stag, No Flation?

The message Jerome Powell wanted to send was the one we highlighted above. The clip that everyone seems to be latching onto instead is his answer in response to a question from a reporter at the Financial Times:

Here’s the exchange:

Q: “The Q1 GDP-1 print has led to some to start mentioning the term stagflation with respect to the U.S. economy. Do you or anyone else on the FOMC think this is now a risk?”

A: “I guess I would say I was around for stagflation and it was, you know, 10 percent - 10 percent unemployment. It was high single digits inflation… And very slow growth.

“So right now we have 3% growth, which is, you know, pretty solid growth, I would say, by any measure. And we have inflation running under 3 percent.

“I don't - I don't really understand where that's coming from. And in addition I would say most forecasters, including our forecasting, was that last year's level of growth was very high, 3.4 percent in I guess the fourth quarter, you know, and probably not going to be sustained and would come down. But that would be, that would be our forecast. That wouldn't be stagflation.

“That would still be to a very healthy level of growth. And of course with inflation, you know our - we will return inflation to 2 percent and that won't be - I don't see the stag or the flation actually.”

To Powell’s point, even though progress on inflation has stalled and growth rates have come down to start 2024, things aren’t so bad. Retail sales last month rebounded to a 4% growth rate, and even after Friday’s jobs report showed a notable deceleration in hiring (the 175k jobs added were the lowest since October), the unemployment rate is still as low as anything we saw in the 45-plus years from 1970-2017.

In Case You Missed It: Last Week’s Insights

May Market Outlook

At the outset of every month, we take a top-down look at the US equity markets and ask ourselves: Do we want to own more stocks or fewer? Should we be erring toward buying or selling? That question sets the stage for everything else we're doing. If our big picture view says that stocks are trending higher, we're going to be focusing our attention on favo…

Industrials Sector Deep Dive

The S&P 500 experienced its first monthly decline since last fall in April, and the Industrials sector was no exception. The Industrials have come off their highs, but the decline hasn’t done any significant damage to the longer-term uptrend that’s been in place for the last 18 months. While former leaders like Tech are stuck

Sector Ratings and Model Portfolio Update

We’re living in a different world than we were a year ago. In 2023, it was mega cap growth stocks or nothing. Yes, more than just growth areas of the market were participating in the bull market. But the only way to outperform was to invest in those growth areas.

Energy Sector Outlook

Failed breakout or false start? The S&P 500 Energy sector has been dealing with stiff resistance at the 2008 and 2014 highs for the better part of the last 2 years, and last month, we finally got that long-awaited breakout. Energy stocks hit their highest levels

What’s Ahead

Here are the key data releases to keep an eye in the upcoming week: