Nothing to Fear but Fear Itself - 12/12/2023

It's a risk-on environment

What is it that drives prices?

Is it intrinsic value? The present value of future cash flows, the pace of earnings acceleration, dividend and buyback policies? Is it economic growth, interest rates, or manufacturing activity?

Each of these plays an important role in building an investment outlook, but the truth is, they don’t make prices move. Not directly. The reality is more simple than that. Prices move based on changes in supply and demand. Or put another way, on peoples’ collective decisions to buy or sell securities.

People do their best to incorporate all those important, fundamental components into their buy/sell decisions, but human behavior is a funny thing. We’re susceptible to psychological flaws, and even when we know those flaws exist, we’re not good at correcting them.

Fear and greed are the most important drivers of the market.

And today, greed is the dominant force.

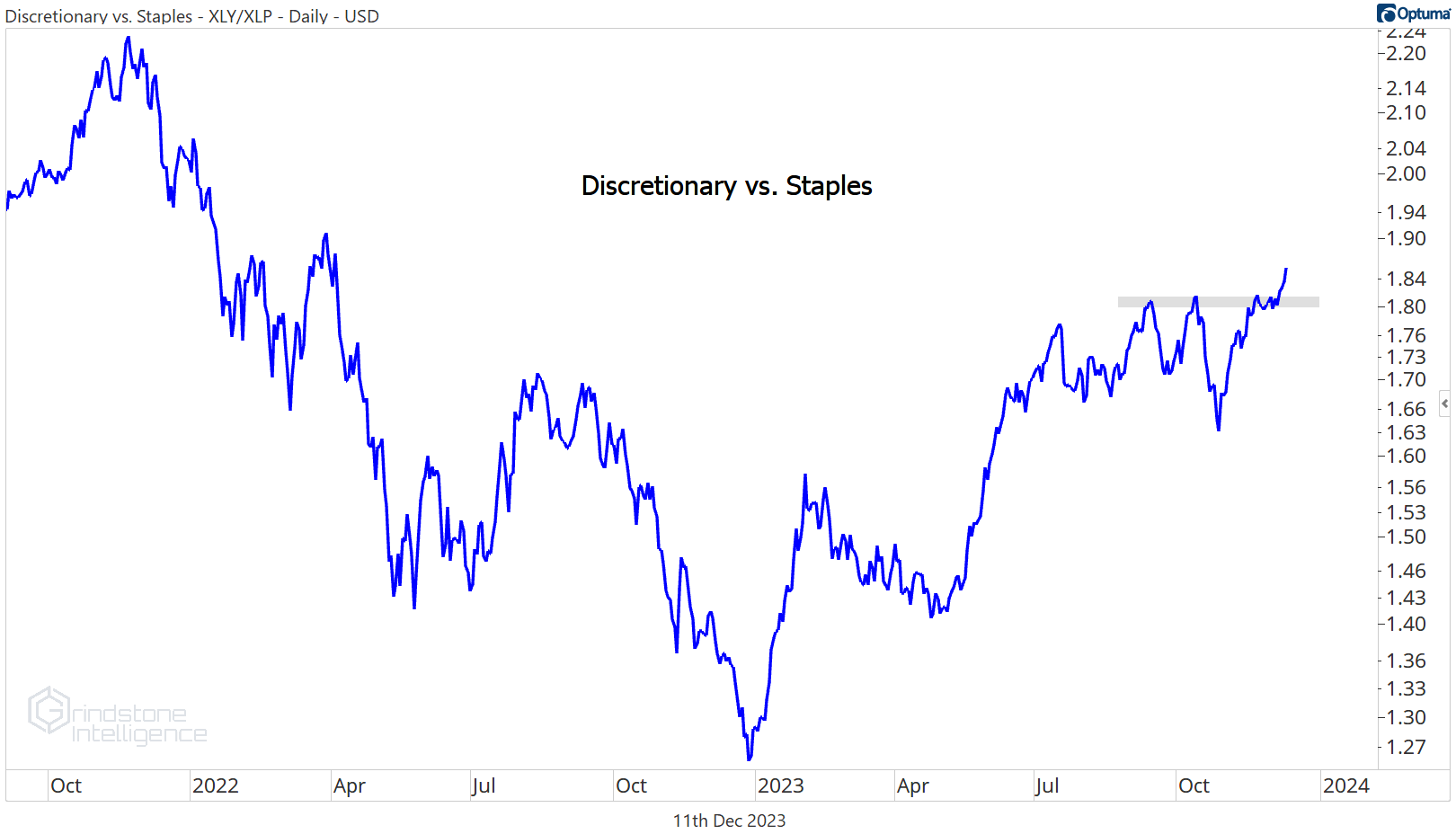

Last week, we published deep dives on two consumer oriented groups of stocks. Consumer Discretionary is one of just 3 sectors outperforming the S&P 500 this year, while the Consumer Staples sector has been one of the worst places to be.

That’s exactly what we’d expect to see in a bull market.

When the economic outlook is uncertain, investors tend to favor companies that offer stability. Consumer Staples fit that bill. Recession or not, we’re going to keep buying toothpaste and toilet paper. But we can’t say the same thing about a Tesla. Staples, then, offer a great measure of risk appetite: when those types of companies outperform, it’s a sign that investors are fearful.

Instead, Discretionary stocks are breaking out to new 18-month highs vs. the Staples. Risk = on.

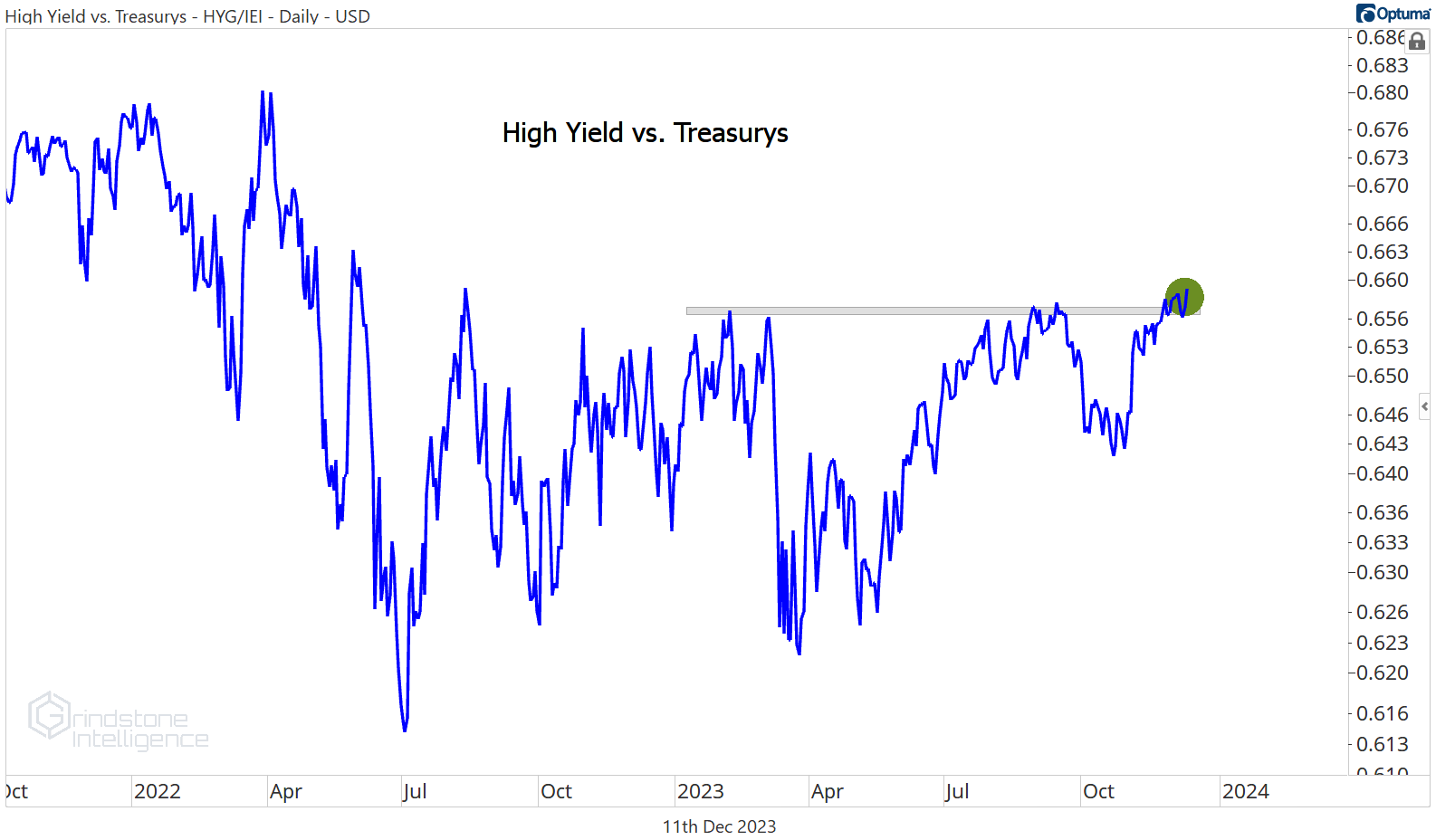

We’re seeing the same dynamics in fixed income. If investors were seeking safe havens within the bond market, we’d expect them to be piling into Treasurys and high quality, investment grade corporates. Instead, high yield bonds are outperforming. Check out the ratio of HYG to IEI, which have similar maturity profiles. The high yield ETF is breaking out.

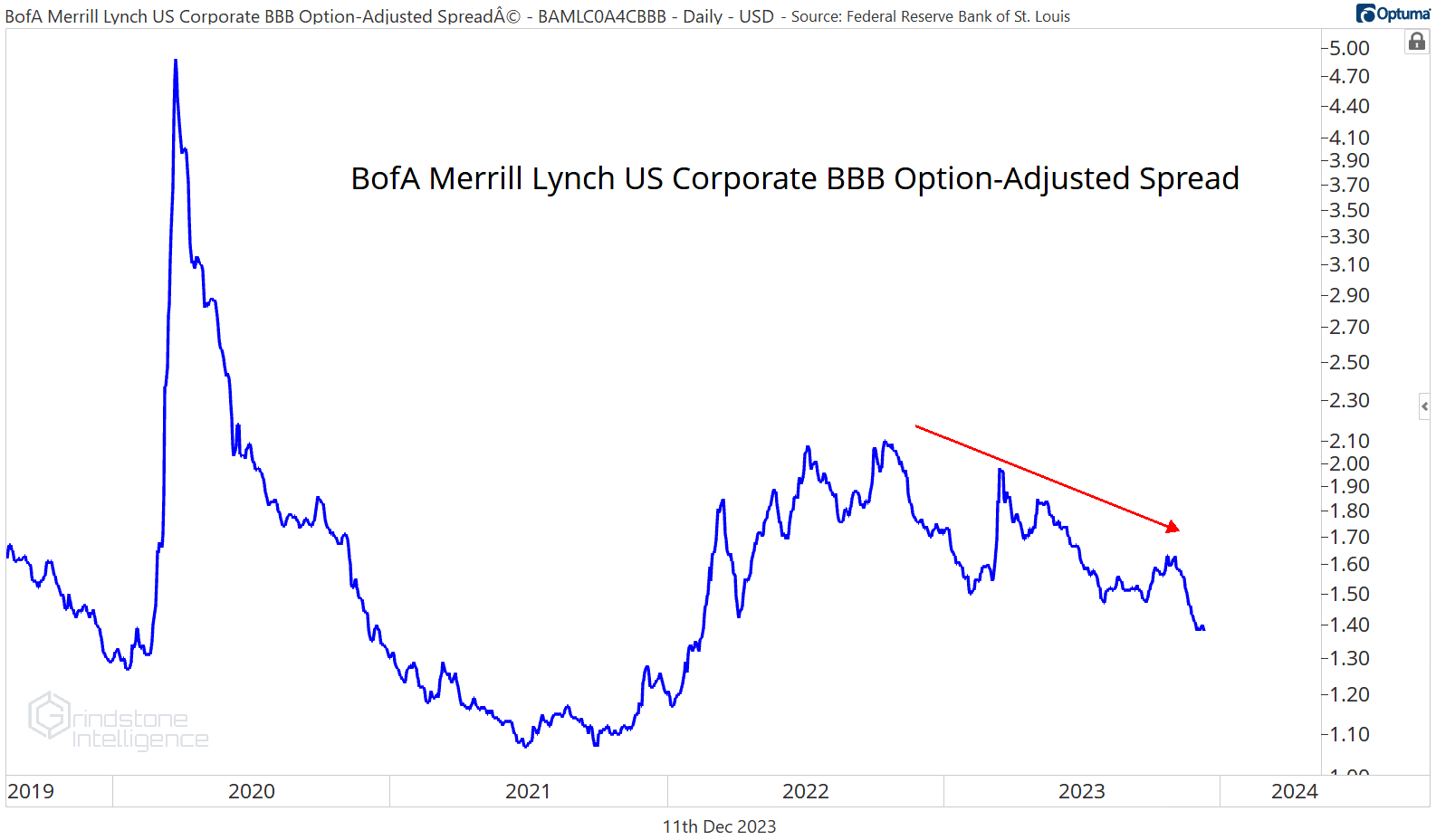

Here’s another way to look at it. Corporate credit spreads (the difference between interest rates on corporate bond issues and Treasurys) just fell to their lowest level in nearly 2 years. If investors were fearful of mass defaults, don’t you think the default risk premium would be rising?

And moving outside the US, check out how Emerging Market bonds are doing. They’ve set a series of higher highs and higher lows vs. US debt. That’s not something you’d expect to see if investors believed we were on the verge of a global recession.

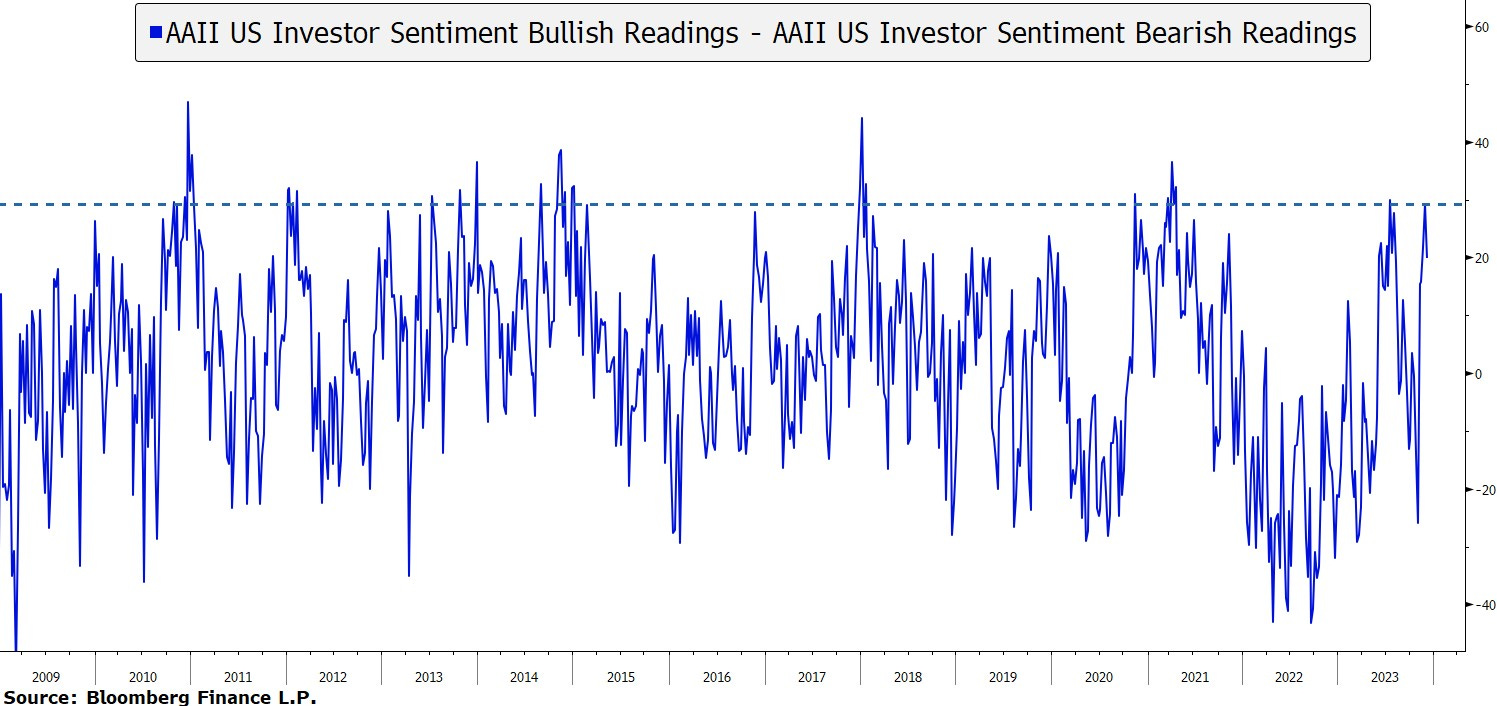

It’s clear what investors are doing. And they’re saying it to, too. Just two weeks ago, the number of bearish survey responses to the AAII US Investor Sentiment Survey dropped to the lowest level since 2017. And the rate at which bulls outnumber the bears is in rarified territory. Greed is the dominant force in today’s market.

There are plenty of risks to the market - there always are. “Bull markets climb a wall of worry,” they say.

Just remember, it’s not the risks themselves that matter, but how investors respond to those risks.

We’ve nothing to fear but fear itself.