The Morning Grind - 03/25/2024

Breadth still healthy

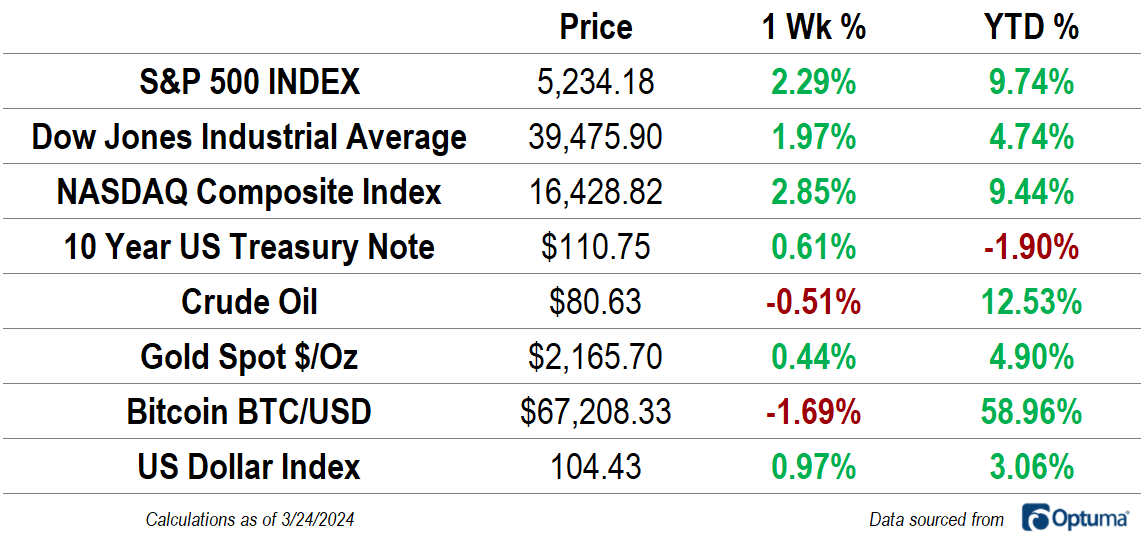

The S&P 500 followed up two consecutive weeks of declines with its best performance of the year, rising 2.3%. For each the S&P 500, Dow Jones Industrial Average, and the NASDAQ Composite, prices closed reached their highest levels of all time. Surprisingly, the strength in stocks coincided with a rally in the US Dollar Index, which had its best weekly close since last November. During the bear market of 2022, a strong Dollar meant week stocks, but more and more, that correlation seems to have died out.

The Federal Reserve surprised no one when it decided to keep interest rates unchanged at last week’s meeting. The tick up in inflation to start the year all but assured a more hawkish stance on monetary policy than the one we had at year-end, when price measures were coming in below expectations. But just because Powell and his peers don’t yet see a reason to lower rates doesn’t mean they see the need to raise them further. Powell simply wants to see more. Here’s what he said at the post-meeting press conference regarding recent high inflation readings:

“I think they haven't really changed the overall story, which is that of inflation moving down gradually on a sometimes-bumpy road toward 2%. I don't think that story has changed. I also don't think that those readings added to anyone's confidence that we're moving closer to that point.”

Market Internals

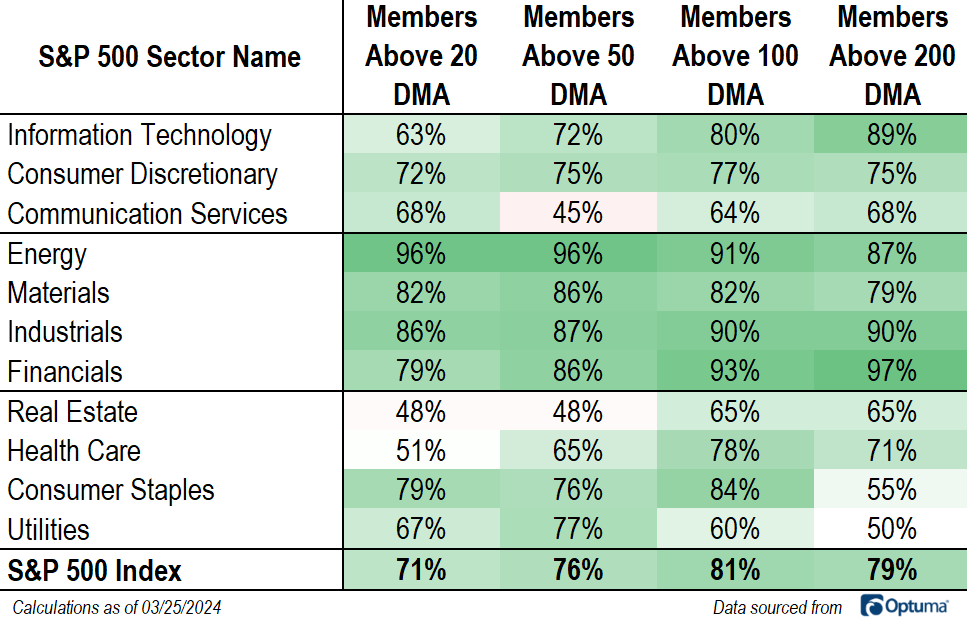

Breadth was a concern for most market watchers throughout 2023, as the rally in growth stocks obscured lackluster performances from value-oriented names during the spring and late-summer months. Index-level declines in August, September, and October had breadth as weak as it had been all year. A surge in prices to end the year laid any lingering concerns about participation to rest, and the strength has continued into 2024. 79% of S&P 500 members are above their 200-day moving average.

Long-term trends are healthiest in the Financials, Industrials, and Information Technology sectors, where more than 89% of constituents have moved above their long-term moving averages. Traditionally considered a risk-off area, the Utilities sector is the most weakly positioned. Just 50% of stocks in that group are in long-term technical uptrends.

More from last week:

Mid-Month Macro Musings

Tomorrow, the Federal Reserve will wrap up its 2-day monetary policy meeting. No one expects them to take any action on interest rates this time around, especially given higher than expected inflation readings to start the year. Rather than what the Fed is

Energy Sector Outlook

Is this finally the time for Energy stocks? We’ve been dealing with stiff resistance at the 2008 and 2014 highs for the better part of the last 2 years, and while the bulls haven’t been able to gain any ground, the bears haven’t been able to capitalize, either.

From the Ground Up

Back in 2005, Joel Greenblatt introduced his ‘Magic Formula for Investing’ with The Little Book That Beats the Market. The book details a methodical approach that helps investors find some of the cheapest, most well-operated companies and buy them each month for a one-year holding period.

Consumer Discretionary: Sector Outlook

In 2023, the Consumer Discretionary sector was among the best places to be. Along with the other two growth-oriented sectors (Information Technology and Communication Services) Discretionary stocks outperformed the benchmark S&P 500. Leadership in 2024 hasn’t been too much different. It’s still Communication Services and Information Technology leading us higher. But the Consumer Discretionary sector has been notably absent from the leaderboard.

What's Ahead

Here's what to watch in the week ahead: